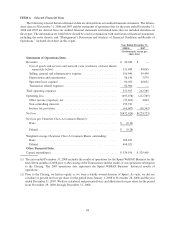

Clearwire 2008 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2008 Clearwire annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

Th

e use o

f

t

h

e reme

di

a

l

met

h

o

df

or a

ll

o

f

t

h

eO

ld

C

l

earw

i

re assets,

b

ut

f

or on

l

y a port

i

on o

f

t

h

e

f

ormer Spr

i

nt

assets, means that Clearwire will bear the entire tax burden with respect to the built-in

g

ain on the Old Clearwire

assets, and will have shifted to it a portion of the tax burden with respect to the built-in gain on the former Sprin

t

assets. Accor

di

ng

l

y, C

l

earw

i

re

i

s

lik

e

l

yto

b

ea

ll

ocate

d

as

h

are o

f

t

h

e taxa

bl

e

i

ncome o

f

C

l

earw

i

re Commun

i

cat

i

ons

t

hat exceeds its proportionate economic interest in Clearwire Communications, and Clearwire ma

y

incur a material

li

a

bili

ty

f

or taxes. However, su

bj

ect to t

h

eex

i

st

i

ng an

d

poss

ibl

e

f

uture

li

m

i

tat

i

ons on t

h

e use o

f

C

l

earw

i

re’s net

operat

i

ng

l

osses, w

hi

c

h

we re

f

er to as NOLs, un

d

er Sect

i

on 382 an

d

Sect

i

on 384 o

f

t

h

eCo

d

e, C

l

earw

i

re’s NOLs ar

e

g

enera

lly

expecte

d

to

b

eava

il

a

bl

etoo

ff

set, to t

h

e extent o

f

t

h

ese NOLs,

i

tems o

fi

ncome an

dg

a

i

na

ll

ocate

d

t

o

Clearwire by Clearwire Communications. See “Risk Factors — The ability of Clearwire to use its net operating

losses to offset its income and gain is subject to limitation.” Clearwire Communications is required to mak

e

di

str

ib

ut

i

ons to C

l

earw

i

re

i

n amounts necessar

y

to pa

y

a

ll

taxes reasona

bly d

eterm

i

ne

dby

C

l

earw

i

re to

b

epa

y

a

bl

e

w

ith respect to its distributive share of the taxable income of Clearwire Communications, after takin

g

into account

t

he net operating loss deductions and other tax benefits reasonably expected to be available to Clearwire. See th

e

s

ect

i

ons t

i

t

l

e

d

“R

i

s

k

Factors — Man

d

ator

y

tax

di

str

ib

ut

i

ons ma

yd

epr

i

ve C

l

earw

i

re Commun

i

cat

i

ons o

ff

un

d

st

h

a

t

are re

q

uired in its business” and “Certain Relationshi

p

s and Related Transactions, and Director Inde

p

endence

”

b

eg

i

nn

i

ng on pages 43 an

d

122, respect

i

ve

l

y, o

f

t

hi

s report

.

Sa

l

es o

f

certain

f

ormer C

l

earwire assets

by

C

l

earwire Communications ma

y

trigger taxa

bl

e gain t

o

C

learwire.

If

C

l

earw

i

re Commun

i

cat

i

ons se

ll

s

i

n a taxa

bl

e transact

i

on an O

ld

C

l

earw

i

re asset t

h

at

h

a

db

u

il

t-

i

nga

i

natt

h

e

ti

me o

fi

ts contr

ib

ut

i

on to C

l

earw

i

re Commun

i

cat

i

ons, t

h

en, un

d

er Sect

i

on 704(c) o

f

t

h

eCo

d

e, t

h

e tax

g

a

i

nont

he

s

ale of the asset generally will be allocated first to Clearwire in an amount up to the remaining (unamortized

)

p

ortion of the built-in gain on the Old Clearwire asset. Under the Operating Agreement, unless Clearwir

e

Commun

i

cat

i

ons

h

as a

b

ona

fid

e non-tax

b

us

i

ness nee

d

(as

d

e

fi

ne

di

nt

h

e Operat

i

n

g

A

g

reement), C

l

earw

i

re

Communications will not enter into a taxable sale of Old Clearwire assets that are intan

g

ible propert

y

and tha

t

w

ould cause Clearwire to be allocated under Section 704(c) more than

$

10 million of built-in gains during any

36

-month period. For this purpose, Clearwire Communications will have a bona fide non-tax business need with

r

es

p

ect to the sale of Old Clearwire assets, if (1) the taxable sale of the Old Clearwire assets will serve a bona fide

b

usiness need of Clearwire Communications’ wireless broadband business and (2) neither the taxable sale nor th

e

r

e

i

nvestment or ot

h

er use o

f

t

h

e procee

d

s

i

ss

i

gn

ifi

cant

l

y mot

i

vate

db

yt

h

e

d

es

i

re to o

b

ta

i

n

i

ncrease

di

ncome tax

b

enefits for the members or to impose income tax costs on Clearwire. Accordin

g

l

y

, Clearwire ma

y

reco

g

nize built-

i

n

g

ain on the sale of Old Clearwire assets (1) in an amount up to $10 million, in an

y

36-month period, and (2) in

greater amounts,

if

t

h

e stan

d

ar

d

o

fb

ona

fid

e non-tax

b

us

i

ness nee

di

s sat

i

s

fi

e

d

.I

f

C

l

earw

i

re Commun

i

cat

i

ons se

ll

s

O

ld Clearwire assets with unamortized built-in

g

ain, then Clearwire is likel

y

to be allocated a share of the taxable

i

ncome of Clearwire Communications that exceeds its

p

ro

p

ortionate economic interest in Clearwire Communi

-

c

at

i

ons, an

d

may

i

ncur a mater

i

a

lli

a

bili

ty

f

or taxes. However, su

bj

ect to t

h

eex

i

st

i

ng an

d

poss

ibl

e

f

uture

li

m

i

tat

i

ons

on t

h

e use o

f

C

l

earw

i

re’s NOLs un

d

er Sect

i

on 382 an

d

Sect

i

on 384 o

f

t

h

eCo

d

e, C

l

earw

i

re’s NOLs are

g

enera

lly

e

xpected to be available to offset, to the extent of these NOLs, items of income and gain allocated to Clearwire by

Clearwire Communications. See the section titled “Risk Factors — The ability of Clearwire to use its net operating

l

osses to o

ff

set

i

ts

i

ncome an

dg

a

i

n

i

ssu

bj

ect to

li

m

i

tat

i

on”

b

e

gi

nn

i

n

g

on pa

g

e44o

f

t

hi

s report. C

l

earw

i

r

e

Communications is required to make distributions to Clearwire in amounts necessar

y

to pa

y

all taxes reasonabl

y

determined b

y

Clearwire to be pa

y

able with respect to its distributive share of the taxable income of Clearwire

Commun

i

cat

i

ons, a

f

ter ta

ki

ng

i

nto account t

h

e net operat

i

ng

l

oss

d

e

d

uct

i

ons an

d

ot

h

er tax

b

ene

fi

ts reasona

bl

y

e

xpected to be available to Clearwire. See the sections titled “Risk Factors — Mandator

y

tax distributions ma

y

de

p

rive Clearwire Communications of funds that are re

q

uired in its business” and “Certain Relationshi

p

san

d

Re

l

ate

d

Transact

i

ons, an

d

D

i

rector In

d

epen

d

ence”

b

eg

i

nn

i

ng on pages 43 an

d

122, respect

i

ve

l

y, o

f

t

hi

s report

.

Sprint and the Investors may shift to Clearwire the tax burden of additional built-in gain through a hold

-

ing company exchange.

Un

d

er t

h

e Operat

i

n

g

A

g

reement, Spr

i

nt or an Investor ma

y

e

ff

ect an exc

h

an

g

eo

f

C

l

earw

i

re Commun

i

cat

i

ons

C

l

ass B Common Interests an

d

C

l

earw

i

re C

l

ass B Common Stoc

kf

or C

l

earw

i

re C

l

ass A Common Stoc

kby

t

ransferrin

g

to Clearwire a holdin

g

compan

y

that owns the Clearwire Communications Class B Common Interest

s

42