Berkshire Hathaway 2005 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2005 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

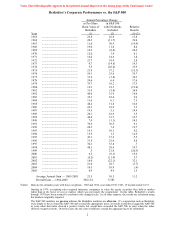

In 2004 our float cost us less than nothing, and I told you that we had a chance – absent a mega-

catastrophe – of no-cost float in 2005. But we had the mega-cat, and as a specialist in that coverage,

Berkshire suffered hurricane losses of $3.4 billion. Nevertheless, our float was costless in 2005 because of

the superb results we had in our other insurance activities, particularly at GEICO.

* * * * * * * * * * * *

Auto policies in force grew by 12.1% at GEICO, a gain increasing its market share of U.S. private

passenger auto business from about 5.6% to about 6.1%. Auto insurance is a big business: Each share-

point equates to $1.6 billion in sales.

While our brand strength is not quantifiable, I believe it also grew significantly. When Berkshire

acquired control of GEICO in 1996, its annual advertising expenditures were $31 million. Last year we

were up to $502 million. And I can’ t wait to spend more.

Our advertising works because we have a great story to tell: More people can save money by

insuring with us than is the case with any other national carrier offering policies to all comers. (Some

specialized auto insurers do particularly well for applicants fitting into their niches; also, because our

national competitors use rating systems that differ from ours, they will sometimes beat our price.) Last

year, we achieved by far the highest conversion rate – the percentage of internet and phone quotes turned

into sales – in our history. This is powerful evidence that our prices are more attractive relative to the

competition than ever before. Test us by going to GEICO.com or by calling 800-847-7536. Be sure to

indicate you are a shareholder because that fact will often qualify you for a discount.

I told you last year about GEICO’ s entry into New Jersey in August, 2004. Drivers in that state

love us. Our retention rate there for new policyholders is running higher than in any other state, and by

sometime in 2007, GEICO is likely to become the third largest auto insurer in New Jersey. There, as

elsewhere, our low costs allow low prices that lead to steady gains in profitable business.

That simple formula immediately impressed me 55 years ago when I first discovered GEICO.

Indeed, at age 21, I wrote an article about the company – it’ s reproduced on page 24 – when its market

value was $7 million. As you can see, I called GEICO “The Security I Like Best.” And that’ s what I still

call it.

* * * * * * * * * * * *

We have major reinsurance operations at General Re and National Indemnity. The former is run

by Joe Brandon and Tad Montross, the latter by Ajit Jain. Both units performed well in 2005 considering

the extraordinary hurricane losses that battered the industry.

It’ s an open question whether atmospheric, oceanic or other causal factors have dramatically

changed the frequency or intensity of hurricanes. Recent experience is worrisome. We know, for instance,

that in the 100 years before 2004, about 59 hurricanes of Category 3 strength, or greater, hit the

Southeastern and Gulf Coast states, and that only three of these were Category 5s. We further know that in

2004 there were three Category 3 storms that hammered those areas and that these were followed by four

more in 2005, one of them, Katrina, the most destructive hurricane in industry history. Moreover, there

were three Category 5s near the coast last year that fortunately weakened before landfall.

Was this onslaught of more frequent and more intense storms merely an anomaly? Or was it

caused by changes in climate, water temperature or other variables we don’ t fully understand? And could

these factors be developing in a manner that will soon produce disasters dwarfing Katrina?

Joe, Ajit and I don’ t know the answer to these all-important questions. What we do know is that

our ignorance means we must follow the course prescribed by Pascal in his famous wager about the

existence of God. As you may recall, he concluded that since he didn’ t know the answer, his personal

gain/loss ratio dictated an affirmative conclusion.

7