Berkshire Hathaway 2005 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2005 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82

|

|

73

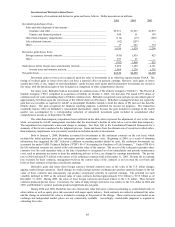

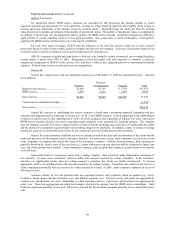

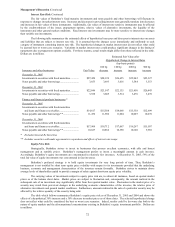

Equity Price Risk (Continued)

Estimated Hypothetical

Fair Value after Percentage

Hypothetical Hypothetical Increase (Decrease) in

Fair Value Price Change Change in Prices Shareholders’ Equity

As of December 31, 2005....................... $46,721 30% increase $60,737 9.9

30% decrease 32,705 (9.9)

As of December 31, 2004....................... $37,717 30% increase $49,032 8.5

30% decrease 26,402 (8.5)

Berkshire is also subject to equity price risk with respect to certain long duration equity index put contracts.

Berkshire’ s maximum exposure with respect to such contracts is approximately $14 billion at December 31, 2005. These

contracts generally expire 15 to 20 years from inception. Outstanding contracts at December 31, 2005, have been written on four

major equity indexes including three foreign. Berkshire’ s potential exposure with respect to these contracts is directly correlated

to the movement of the underlying stock index between contract inception date and expiration. Thus, if the overall value at

December 31, 2005 of the underlying indices decline 30%, Berkshire would incur a pre-tax loss of approximately $900 million.

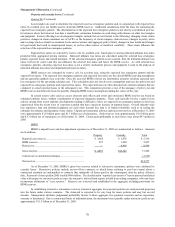

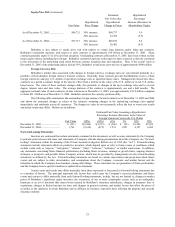

Foreign Currency Risk

Berkshire’ s market risks associated with changes in foreign currency exchange rates are concentrated primarily in a

portfolio of short duration foreign currency forward contracts. Generally, these contracts provide that Berkshire receive certain

foreign currencies and pay U.S. dollars at specified exchange rates at specified future dates. Management entered into these

contracts as a partial economic hedge of the adverse effect from a decline in the value of the U.S. dollar on its net U.S. dollar-

based assets. The value of these contracts changes daily due primarily to changes in the spot exchange rates and to a lesser

degree, interest rates and time value. The average duration of the contracts is approximately one and a half months. The

aggregate notional value of such contracts, in nine currencies at December 31, 2005, was approximately $13.8 billion compared

to about $21.4 billion as of December 31, 2004. Berkshire monitors the currency positions daily.

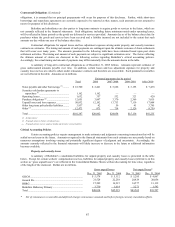

The following table summarizes the outstanding foreign currency forward contracts as of December 31, 2005 and 2004

and shows the estimated changes in values of the contracts assuming changes in the underlying exchange rates applied

immediately and uniformly across all currencies. The changes in value do not necessarily reflect the best or worst case results

and actual results may differ. Dollars are in millions.

Estimated Fair Value Assuming a Hypothetical

Percentage Increase (Decrease) in the Value of

Foreign Currencies Versus the U.S. Dollar

Fair Value (20%) (10%) (1%) 1% 10% 20%

December 31, 2005............................. $ (231) $(2,684) $(1,515) $ (366) $ (95) $1,206 $2,855

December 31, 2004............................. 1,761 (2,614) (475) 1,533 1,991 4,127 6,669

Forward-Looking Statements

Investors are cautioned that certain statements contained in this document, as well as some statements by the Company

in periodic press releases and some oral statements of Company officials during presentations about the Company, are “forward-

looking” statements within the meaning of the Private Securities Litigation Reform Act of 1995 (the “Act”). Forward-looking

statements include statements which are predictive in nature, which depend upon or refer to future events or conditions, which

include words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “estimates,” or similar expressions. In addition,

any statements concerning future financial performance (including future revenues, earnings or growth rates), ongoing business

strategies or prospects, and possible future Company actions, which may be provided by management are also forward-looking

statements as defined by the Act. Forward-looking statements are based on current expectations and projections about future

events and are subject to risks, uncertainties, and assumptions about the Company, economic and market factors and the

industries in which the Company does business, among other things. These statements are not guaranties of future performance

and the Company has no specific intention to update these statements.

Actual events and results may differ materially from those expressed or forecasted in forward-looking statements due

to a number of factors. The principal important risk factors that could cause the Company’ s actual performance and future

events and actions to differ materially from such forward-looking statements, include, but are not limited to, changes in market

prices of Berkshire’ s significant equity investees, the occurrence of one or more catastrophic events, such as an earthquake,

hurricane or an act of terrorism that causes losses insured by Berkshire’ s insurance subsidiaries, changes in insurance laws or

regulations, changes in Federal income tax laws, and changes in general economic and market factors that affect the prices of

securities or the industries in which Berkshire and its affiliates do business, especially those affecting the property and casualty

insurance industry.