Berkshire Hathaway 2005 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2005 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

60

Management’s Discussion (Continued)

Insurance — Underwriting (Continued)

Berkshire Hathaway Reinsurance Group (Continued)

Retroactive policies normally provide very large, but limited, indemnification of unpaid losses and loss adjustment

expenses with respect to past loss events, which are generally expected to be paid over long periods of time. The underwriting

losses from retroactive reinsurance are primarily attributed to the amortization of deferred charges established on retroactive

reinsurance contracts written in previous years. The deferred charges, which represent the difference between the policy

premium and the estimated ultimate claim reserves, are amortized over the expected claim payment period using the interest

method. The amortization charges are recorded as losses incurred and, therefore, produce underwriting losses. The level of

amortization in a given period is based upon estimates of the timing and amount of future loss payments. While contract terms

vary, losses under retroactive contracts are generally subject to a very large aggregate dollar limit occasionally exceeding

$1 billion under a single contract. The expected amount and timing of future loss payments is reviewed periodically. To the

extent there are changes in these estimates, deferred charge balances are adjusted on a retrospective basis via a cumulative

adjustment.

Underwriting losses in 2005 from retroactive contracts are net of a pre-tax gain of approximately $46 million related to

the final settlement of remaining unpaid losses under a certain retroactive reinsurance agreement. In addition, estimates of

unpaid losses were reviewed during the fourth quarter of 2005 which resulted in a net reduction of $75 million in loss reserves.

Also, rates of deferred charge amortization on certain contracts were decreased due to slower than expected loss payments.

During 2004 the estimated timing of future loss payments with respect to one large contract was accelerated which produced an

incremental pre-tax amortization charge of approximately $100 million.

Loss payments for all retroactive contracts, including the aforementioned settlement totaled approximately $969

million in 2005 compared to $860 million in 2004. Unamortized deferred charges at December 31, 2005 totaled approximately

$2.13 billion compared to $2.45 billion at year-end 2004. Management believes that these charges are reasonable with respect to

the large amounts of float related to these policies, which totaled about $6.9 billion at December 31, 2005. Income generated

from the investment of float is reflected in net investment income and investment gains.

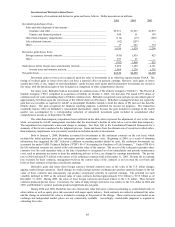

Premiums earned in 2005 from other multi-line reinsurance increased approximately $226 million over 2004. In 2005,

increased premiums were earned from new workers’ compensation and ongoing aviation programs and were partially offset by

declines in quota-share contracts. Premiums earned in 2004 from traditional multi-line reinsurance decreased $510 million

compared to 2003. The comparative decrease was primarily due to declines in quota-share participations (including Lloyd’ s) and

the termination of a major quota-share contract in mid-2003.

Pre-tax underwriting results from other multi-line reinsurance in 2005 included estimated losses of approximately $100

million from Hurricanes Katrina, Rita and Wilma. Pre-tax underwriting results in 2004 included losses of approximately $175

million arising from the third quarter hurricanes affecting the U.S. and Caribbean. However, catastrophe losses in 2004 were

more than offset by increased underwriting gains in aviation coverages and approximately $160 million in gains from the

commutations of several reinsurance contracts. Underwriting gains in 2003 reflected low amounts of property and aviation

losses. There were no significant commutations in 2003.

The pre-tax maximum probable loss from a single event at December 31, 2005 is estimated to be $6 billion resulting

from potential risk of loss from a major earthquake in California.

Berkshire Hathaway Primary Group

Berkshire’ s primary insurance group consists of a wide variety of smaller insurance businesses that principally write

liability coverages for commercial accounts. These businesses include: National Indemnity Company’ s primary group operation

(“NICO Primary Group”), a writer of motor vehicle and general liability coverages; U.S. Investment Corporation (“USIC”),

whose subsidiaries underwrite specialty insurance coverages; a group of companies referred to internally as “Homestate”

operations, providers of standard multi-line insurance; Central States Indemnity Company (“CSI”), a provider of credit and

disability insurance to individuals nationwide through financial institutions; and Med Pro which was acquired as of June 30,

2005. See Note 3 to the Consolidated Financial Statements for additional information concerning this acquisition.

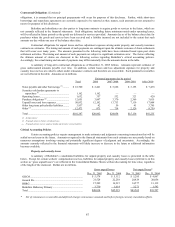

Collectively, Berkshire’ s other primary insurance businesses produced earned premiums of $1,498 million in 2005,

$1,211 million in 2004, and $1,034 million in 2003. Premiums earned in 2005 by Med Pro accounted for most of the increase in

total premiums earned by the group compared with 2004. The increase in premiums earned in 2004 compared to 2003 was

largely attributed to increased volume of USIC and the NICO Primary Group. Net underwriting gains of Berkshire’ s other

primary insurance businesses totaled $235 million in 2005, $161 million in 2004, and $74 million in 2003. The underwriting

gain in 2005 reflected a decrease in loss reserve estimates for pre-2005 loss events in auto and general liability business,

improved results of Homestate, USIC and CSI operations, partially offset by losses incurred from increases in medical

malpractice reserves.