Berkshire Hathaway 2005 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2005 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82

|

|

71

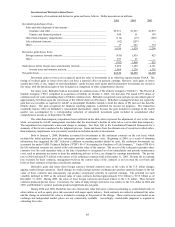

Property and casualty losses (Continued)

BHRG (Continued)

BHRG’ s liabilities for environmental, asbestos, and latent injury losses and loss adjustment expenses are presently

believed to be concentrated within retroactive reinsurance contracts. Reserves for such losses were approximately $4.0 billion at

December 31, 2005 and $4.2 billion at December 31, 2004. Claims paid in 2005 attributable to such losses were approximately

$273 million. BHRG, as a reinsurer, does not regularly receive reliable information regarding numbers of asbestos,

environmental and latent injury claims from ceding companies on a consistent basis, particularly with respect to multi-line treaty

or aggregate excess of loss policies.

BHRG’ s other property and casualty loss reserves derive from catastrophe, individual risk and multi-line reinsurance

policies. Reserve amounts are based upon loss estimates reported by ceding companies and IBNR reserves, which are primarily

a function of reported losses from ceding companies and anticipated loss ratios established on an individual contract basis

supplemented by management’ s judgment of the impact on each contract of major catastrophe events as they become known.

Anticipated loss ratios are based upon management’ s judgment considering the type of business covered, analysis of each ceding

company’ s loss history and evaluation of that portion of the underlying contracts underwritten by each ceding company, which

are in turn ceded to BHRG. A range of reserve amounts as a result of changes in underlying assumptions is not prepared.

Other Critical Accounting Policies

Berkshire records as assets deferred charges with respect to liabilities assumed under retroactive reinsurance contracts.

At the inception of these contracts, the deferred charges represent the difference between the consideration received and the

estimated ultimate liability for unpaid losses. Deferred charges are amortized using the interest method over an estimate of the

ultimate claim payment period and are reflected in earnings as a component of losses and loss expenses. The deferred charge

balances are adjusted periodically to reflect new projections of the amount and timing of loss payments. Adjustments to these

assumptions are applied retrospectively from the inception of the contract. Unamortized deferred charges totaled $2.4 billion at

December 31, 2005. Significant changes in the amount and payment timing of estimated unpaid losses may have a significant

effect on unamortized deferred charges and the amount of periodic amortization.

Berkshire’ s Consolidated Balance Sheet as of December 31, 2005 includes goodwill of acquired businesses of

approximately $23.6 billion. A significant amount of judgment is required in performing goodwill impairment tests. Such tests

include periodically determining or reviewing the estimated fair value of Berkshire’ s reporting units. There are several methods

of estimating a reporting unit’ s fair value, including market quotations, asset and liability fair values and other valuation

techniques, such as discounted projected future net earnings and multiples of earnings. If the carrying amount of a reporting

unit, including goodwill, exceeds the estimated fair value, then individual assets, including identifiable intangible assets, and

liabilities of the reporting unit are estimated at fair value. The excess of the estimated fair value of the reporting unit over the

estimated fair value of net assets would establish the implied value of goodwill. The excess of the recorded amount of goodwill

over the implied value is then charged to earnings as an impairment loss.

Berkshire’ s consolidated financial position reflects very significant amounts of invested assets. A substantial portion

of these assets are carried at fair values based upon current market quotations and, when not available, based upon fair value

pricing models. Certain of Berkshire’ s fixed maturity securities are not actively traded in the financial markets. Further,

Berkshire’ s finance businesses maintain significant balances of finance receivables, which are carried at amortized cost.

Considerable judgment is required in determining the assumptions used in certain pricing models, including interest rate, loan

prepayment speed, credit risk and liquidity risk assumptions. Significant changes in these assumptions can have a significant

effect on carrying values.

Information concerning recently issued accounting pronouncements which are not yet effective is included in Note 1(r)

to the Consolidated Financial Statements. As indicated in Note 1(r) to the Consolidated Financial Statements, Berkshire does not

expect any of the recently issued accounting pronouncements to have a material effect on its financial statements.

Market Risk Disclosures

Berkshire’ s Consolidated Balance Sheets include a substantial amount of assets and liabilities whose fair values are

subject to market risks. Berkshire’ s significant market risks are primarily associated with interest rates, equity prices and foreign

currency exchange rates. The following sections address the significant market risks associated with Berkshire’ s business

activities.

Interest Rate Risk

Berkshire’ s management prefers to invest in equity securities or to acquire entire businesses based upon the principles

discussed in the following section on equity price risk. When unable to do so, management may alternatively invest in bonds,

loans or other interest rate sensitive instruments. Berkshire’ s strategy is to acquire securities that are attractively priced in

relation to the perceived credit risk. Management recognizes and accepts that losses may occur. Berkshire has historically

utilized a modest level of corporate borrowings and debt. Further, Berkshire strives to maintain the highest credit ratings so that

the cost of debt is minimized. Berkshire utilizes derivative products, such as interest rate swaps, to manage interest rate risks on

a limited basis.