Avon 2003 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2003 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85

|

|

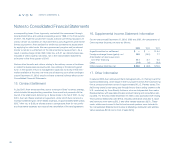

relief for alleged violations of the California Business and Professions Code,

breach of contract, unjust enrichment and “money had and received.” The

Company filed a demurrer to the complaint, asserting that it failed to state a

cause of action. In December 2003, the court sustained the Company’s demur-

rer based on the initial plaintiff’s failure to allege actual damages, but gave the

plaintiff time to amend her complaint and produce a plaintiff who had actually

suffered damages. On January 23, 2004, plaintiff Blakemore and three other

plaintiffs served an amended class action complaint on behalf of Avon Sales

Representatives who “received products from Avon they did not order, there-

after returned the unordered products to Avon, and did not receive credit for

those returned products.” The amended complaint seeks unspecified com-

pensatory and punitive damages, restitution and injunctive relief for alleged

fraudulent concealment, breach of contract, unjust enrichment and violation of

the California Business and Professions Code. The Company believes that

this action is a dispute over purported customer service issues and is an

inappropriate subject for consideration as a class action. While it is not pos-

sible to predict the outcome of litigation, management believes that there are

meritorious defenses to the claims asserted and that this action should not

have a material adverse effect on the Consolidated Financial Statements. This

action is being vigorously contested.

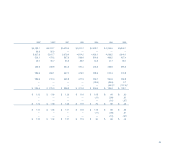

On December 20, 2002, a Brazilian subsidiary of the Company received a series

of excise and income tax assessments from the Brazilian tax authorities assert-

ing that the establishment in 1995 of separate manufacturing and distribution

companies in that country was done without a valid business purpose. The

assessments assert tax deficiencies during portions of the years 1997 and 1998

of approximately $71.0 at the exchange rate on the date of this filing, plus penal-

ties and accruing interest totaling approximately $121.0 at the exchange rate on

the date of this filing. On July 1, 2003, the Brazilian subsidiary of the Company

was informed that the first-level appellate body had rejected the basis for

income tax assessments representing approximately 78% of the total assess-

ment, or $150.0 (including interest), but that rejection is subject to mandatory

second-level appellate review. The balance of the assessment relating to

excise taxes (approximately $42.0) was not affected. On December 26, 2003

an additional assessment was received in respect of excise taxes for the bal-

ance of 1998, totaling approximately $76.0 at the exchange rate on the date of

this filing and asserting a different theory of liability based on purported market

sales data. In the event that the assessments are upheld or reinstated in the ear-

lier stages of review, it may be necessary for the Company to provide security to

pursue further appeals, which, depending on the circumstances, may result in a

charge to income. It is not possible to make a reasonable estimate of the amount

or range of expense that could result from an unfavorable outcome in respect

of these or any additional assessments that may be issued for subsequent

periods. The structure adopted in 1995 is comparable to that used by many

companies in Brazil, and the Company believes that it is appropriate, both

operationally and legally, and that the assessments are unfounded. This

matter is being vigorously contested and in the opinion of the Company’s out-

side counsel the likelihood that the assessments ultimately will be upheld

is remote. Management believes that the likelihood that the assessments

will have a material impact on the Consolidated Financial Statements is

also remote.

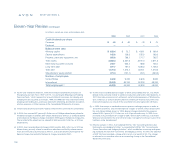

Polish subsidiaries of the Company have been responding to Protocols of

Inspection served by the Polish tax authorities in respect of 1999 and 2000 tax

audits. The Protocols asserted tax deficiencies, penalties and accruing interest

totaling approximately $30.0 at the exchange rate on the date of this filing:

$16.5 primarily relating to the documentation of certain sales, and $13.5 related

to excise taxes. On July 29, 2003, the Company accepted a final assessment of

approximately $.6 in respect of the excise tax matter, and on December 29,

2003, the Company accepted a final assessment of approximately $.5 in

respect of the documentation of sales matter.

In 1998, the Argentine tax authorities denied certain past excise tax credits

taken by Avon’s subsidiary in Argentina and assessed this subsidiary for the

95