Avon 2003 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2003 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

|

|

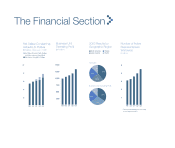

Management’s Discussion and Analysis of Financial Condition and Results of Operations

management’s discussion

Avon’s calculations of pension, postretirement and postemployment costs

are dependent on assumptions, including discount rates, expected return on

plan assets, interest cost, health care cost trend rates, benefits earned, mor-

tality rates, the number of associate retirements, the number of associates

electing to take lump-sum payments and other factors. Actual results that

differ from assumptions are accumulated and amortized over future periods

and, therefore, generally affect recognized expense and the recorded obliga-

tion in future periods. While management believes that the assumptions used

are reasonable, differences in actual experience or changes in assumptions

may materially affect Avon’s pension, postretirement and postemployment

obligations and future expense.

The expected return on plan assets for all pension plans approximated $75.0

for the year ended December 31, 2003, and was calculated based upon the

average expected long-term rate of return on plan assets. For the year ended

December 31, 2003, the assumed rate of return on assets globally was 8.3%,

which represents the weighted-average rate of return on all plan assets includ-

ing the U.S. and non-U.S. plans. In determining the long-term rate of return,

the Company considers the nature of the plans’ investments, an expectation

for the plans’ investment strategies and historical rates of return.

The majority of the Company’s pension plan assets relate to the U.S. pension

plan. The assumed rate of return for 2003 for the U.S. plan was 8.8%. Historical

rates of return for the U.S. plan for the most recent 10-year and 20-year periods

were 7.8% and 10.5%, respectively. In the U.S. plan, the Company’s asset allo-

cation policy has favored U.S. equity securities, which have returned 10% and

12%, respectively, over the 10-year and 20-year periods.

In addition, the current rate of return assumption for the U.S. plan was based

on an asset allocation of approximately 35% in corporate and government

bonds (which are expected to earn approximately 5% to 7% in the long term)

and 65% in equity securities (which are expected to earn approximately 9%

to 10% in the long term). Similar assessments were performed in determining

rates of return on non-U.S. pension plan assets, to arrive at the Company’s

current weighted-average rate of return of 8.3%.

During 2002, the assets associated with the Company’s benefit plans experi-

enced negative investment returns, most significantly in the U.S. plan where

the market value of plan assets declined approximately 13%. As a result,

Avon made cash contributions to its U.S. qualified pension plan of $60.0 in

2003 and $120.0 in 2002 versus $25.0 in 2001. However, in 2003, the market

value of plan assets in the U.S. increased approximately 20%. The Company

continues to believe that 8.3% for all plans is a reasonable long-term rate of

return and will continue to evaluate the expected rate of return, at least annu-

ally, and adjust as necessary.

The discount rate used for determining future pension obligations for each

individual plan is based on a review of long-term bonds that receive a high

rating given by a recognized rating agency. The weighted average discount

rate for U.S. and non-U.S. plans determined on this basis has decreased to

6.0% at December 31, 2003, from 6.3% at December 31, 2002.

Future effects of pension plans on the operating results of the Company will

depend on economic conditions, employee demographics, mortality rates, the

number of associates electing to take lump-sum payments, investment per-

formance and funding decisions. However, given current assumptions (including

those noted above), 2004 pension expense related to the U.S. plan is expected

to increase in the range of $10.0 to $15.0. The Company does not anticipate

that this incremental expense will affect its ability to meet its financial targets.

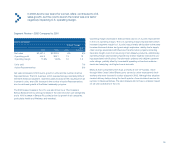

A 50 basis point change (in either direction) on the expected rate of return on

plan assets, the discount rate or the rate of compensation increases would

have the following effect on 2003 pension expense:

Increase/(Decrease) in

pension expense

50 basis point 50 basis point

Increase Decrease

Rate of return on assets $(4.4) $ 4.4

Discount rate (7.7) 8.7

Rate of compensation increase 4.1 (3.4)

26