Asus 2011 Annual Report Download - page 159

Download and view the complete annual report

Please find page 159 of the 2011 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

155

~27~

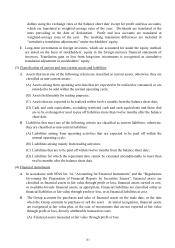

(5) Notes and accounts receivable and other receivables

A. Notes and accounts receivable are claims resulting from the sale of goods or services. Other

receivables are those arising from transactions other than the sale of goods or services.

Before December 31, 2010, allowance for doubtful accounts is provided according to the

evaluation of the collectability of notes and accounts receivable and other receivables, taking

into account the bad debts incurred in prior years and the aging analysis of the receivables.

B. Effective January 1, 2011, notes and accounts receivable and other receivables are recognized

initially at fair value and subsequently measured at amortized cost using the effective interest

method, less provision for accumulated impairment. A provision for impairment is established

when there is objective evidence that the receivables are impaired. The amount of the

provision is the difference between the asset’s carrying amount and the present value of

estimated future cash flows, discounted at the original effective interest rate. When the fair

value of the asset subsequently increases and the increase can be objectively related to an event

occurring after the impairment loss was recognized in profit or loss, the impairment loss shall

be reversed to the extent of the loss previously recognized in profit or loss. Such recovery of

impairment loss shall not make the asset’s carrying amount more than its amortized cost where

no accumulated impairment loss was recognized. Subsequent recoveries of amounts previously

written off are recognized in profit.

(6) Inventories

The costs of inventories consist of those necessary expenditures incurred in bringing each item of

inventory to its usable condition and location. Cost is calculated on a weighted-average basis.

Inventories are valued at the lower of cost or net realizable value. Net realizable value by item is

determined based on the estimated selling price in the ordinary course of business, less estimated

costs of completion and costs to sell.

(7) Long-term equity investments accounted for under the equity method

A. Long-term investments are accounted for under the equity method when the percentage of

ownership held by the Group exceeds 20% or if the Group owns less than 20% of the

investee’s capital but have significant influence on the investee’s operations. If an investee

company accounted for under the equity method issues new shares and the Company does not

purchase new shares proportionately, then the investment percentage, and the equity in net

assets of the investee, will be changed. The effect of such change is adjusted against the

additional paid-in capital resulting from long-term equity investments or retained earnings.

B. The difference between the cost of the investment and the amount of underlying equity in net

assets of an investee attributed to depreciable, depletable, or amortizable assets is amortized

over the estimated remaining economic years. The difference attributed to the carrying amount

in excess of or lower than the fair value of assets is written off entirely when the difference

disappear. The cost of investment in excess of the fair value of identifiable net assets is

recognized as goodwill and is no longer amortized. The difference attributed to the fair value

of identifiable net assets in excess of the cost of investment causes a proportional decrease in

the carrying amount of non-current assets. When the carrying amount of non-current assets is

reduced to zero, the remaining difference is recorded as extraordinary gain.