APS 2015 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2015 APS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

|

|

Table of Contents

Regulatory Accounting

Regulatory accounting allows for the actions of regulators, such as the ACC and FERC, to be reflected in our financial

statements. Their actions may cause us to capitalize costs that would otherwise be included as an expense in the current period by

unregulated companies. Regulatory assets represent incurred costs that have been deferred because they are probable of future

recovery in customer rates. Regulatory liabilities generally represent expected future costs that have already been collected from

customers. Management continually assesses whether our regulatory assets are probable of future recovery by considering factors such

as applicable regulatory environment changes and recent rate orders to other regulated entities in the same jurisdiction. This

determination reflects the current political and regulatory climate in Arizona and is subject to change in the future. If future recovery of

costs ceases to be probable, the assets would be written off as a charge in current period earnings. We had $1,364 million of regulatory

assets and $1,140 million of regulatory liabilities on the Consolidated Balance Sheets at December 31, 2015.

Included in the balance of regulatory assets at December 31, 2015 is a regulatory asset of $619 million for pension benefits.

This regulatory asset represents the future recovery of these costs through retail rates as these amounts are charged to earnings. If these

costs are disallowed by the ACC, this regulatory asset would be charged to OCI and result in lower future earnings.

See Notes 1 and 3 for more information.

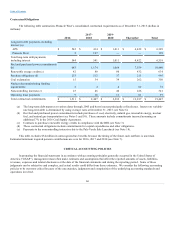

Pensions and Other Postretirement Benefit Accounting

Changes in our actuarial assumptions used in calculating our pension and other postretirement benefit liability and expense can

have a significant impact on our earnings and financial position. The most relevant actuarial assumptions are the discount rate used to

measure our liability and net periodic cost, the expected long-term rate of return on plan assets used to estimate earnings on invested

funds over the long-term, the mortality assumptions, and the assumed healthcare cost trend rates. We review these assumptions on an

annual basis and adjust them as necessary.

The following chart reflects the sensitivities that a change in certain actuarial assumptions would have had on the December 31,

2015 reported pension liability on the Consolidated Balance Sheets and our 2015 reported pension expense, after consideration of

amounts capitalized or billed to electric plant participants, on Pinnacle West’s Consolidated Statements of Income (dollars in millions):

Increase (Decrease)

Actuarial Assumption (a)

Impact on

Pension

Liability

Impact on

Pension

Expense

Discount rate:

Increase 1%

$ (329)

$ (11)

Decrease 1%

399

16

Expected long-term rate of return on plan assets:

Increase 1%

—

(13)

Decrease 1%

—

13

(a) Each fluctuation assumes that the other assumptions of the calculation are held constant while the rates are changed by one

percentage point.

67