Albertsons 2013 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2013 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

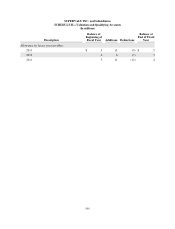

|

|

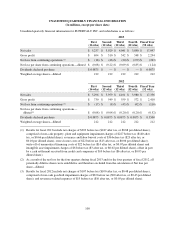

Divestitures

During the second quarter of fiscal 2012, the Company announced it had reached an agreement to sell 107 fuel

centers which were part of the Retail Food segment. The Company received $89 in cash and recognized a pre-tax

loss of $7 during fiscal 2012, of which $1 and $6 of the pre-tax loss is presented as continuing operations and

discontinued operations, respectively, related to the sale of the fuel centers. The Company finalized the sale of

the fuel centers during the third and fourth quarters of fiscal 2012.

NOTE 16—SUBSEQUENT EVENTS

On March 21, 2013, the Company completed the sale of NAI for $100 in cash subject to working capital

adjustments, and the assumption of certain debt and capital lease obligations of approximately $3,200, which

were retained by NAI.

Concurrently with the execution of the Stock Purchase Agreement, the Company entered into a Tender Offer

Agreement (the “Tender Offer Agreement”) with Symphony Investors, LLC, owned by a Cerberus Capital

Management, L.P. (“Cerberus”)-led investor consortium (“Symphony Investors”) and Cerberus, pursuant to

which, upon the terms and subject to the conditions of the Tender Offer Agreement, and contingent upon the NAI

Banner Sale, Symphony Investors tendered for up to 30 percent of the issued and outstanding common stock of

the Company at a purchase price of $4.00 per share in cash (the “Tender Offer”). Approximately 12 shares were

validly tendered, representing approximately 5.5 percent of the issued and outstanding shares at the time of the

Tender Offer expiration on March 20, 2013. All shares that were validly tendered and not properly withdrawn

were accepted for payment in accordance with the terms of Tender Offer. In addition, pursuant to the terms of the

Tender Offer Agreement, on March 21, 2013, SUPERVALU issued approximately 42 additional shares of

common stock (approximately 19.9 percent of outstanding shares prior to the share issuance) to Symphony

Investors at the Tender Offer price per share of $4.00, resulting in $170 in cash proceeds to the Company, which

brought Symphony Investors ownership percent to 21.2 percent after the share issuance. Cash proceeds from the

share issuance provided additional cash inflows from financing activities of $170 during the first quarter of fiscal

2014, which were used to reduce outstanding borrowings under the ABL Facility described below. The share

issuance will have a dilutive effect on future net earnings (loss) per share due to the additional 42 shares

outstanding.

Following the sale of NAI, the Company remains contingently liable with respect to certain self-insurance

commitments as a result of parental guarantees issued by SUPERVALU INC. with respect to the obligations of

NAI that were incurred while NAI was a subsidiary of the Company. The total amount of all such guarantees was

$411 and represented $369 on a discounted basis. Because NAI remains a primary obligor on these self-insurance

obligations, the Company believes that the likelihood that it will be required to assume a material amount of

these obligations is remote. Accordingly, no amount has been recorded in the Consolidated Balance Sheets for

these parent guarantees.

On March 21, 2013, the Company entered into (i) an amended and restated five-year $1,000 asset-based

revolving credit facility (the “ABL Facility”), secured by the Company’s inventory, credit card receivables and

certain other assets, which will bear interest at the rate of LIBOR plus 1.75 percent to LIBOR plus 2.25 percent,

depending on utilization and (ii) a new six-year $1,500 term loan (the “Term Loan Facility”), secured by

substantially all of the Company’s real estate, equipment and certain other assets, which will bear interest at the

rate of LIBOR plus 5.00 percent and include a floor on LIBOR set at 1.25 percent (collectively, the “Refinancing

Transactions”).

The proceeds of the Refinancing Transactions were used to replace the Company’s existing five-year $1,650

Revolving ABL Credit Facility, the existing $850 Secured Term Loan Facility and the $200 accounts receivable

securitization facility, and refinanced the $490 of 7.5% senior notes due 2014.

97