Albertsons 2013 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2013 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

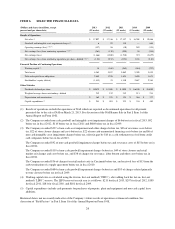

allowances, with no offsetting changes to the base price on the products purchased, would impact gross profit by

less than 10 basis points.

Inventories

Inventories are valued at the lower of cost or market. Substantially all of the Company’s inventory consists of

finished goods.

The Company uses one of either replacement cost, weighted average cost, or the retail inventory method (“RIM”)

to value discrete inventory items at lower of cost or market before application of any last-in, first-out (“LIFO”)

reserve. As of February 23, 2013 and February 25, 2012, approximately 60 percent of the Company’s inventories

were valued under the LIFO method.

As of February 23, 2013 and February 25, 2012, approximately 5 percent and 4 percent, respectively, of the

Company’s inventories were valued under the replacement cost method before application of any LIFO reserve.

The weighted average cost and RIM methods of inventory valuation together comprised approximately

55 percent and 56 percent of inventory as of February 23, 2013 and February 25, 2012, respectively, before

application of any LIFO reserve.

Under the replacement cost method applied on a LIFO basis, the most recent purchase cost is used to calculate

the current cost of inventory before application of any LIFO reserve. The replacement cost approach results in

inventories being valued at the lower of cost or market because of the high inventory turnover and the resulting

low inventory days supply on hand combined with infrequent vendor price changes for these items of inventory.

The Company uses one of either cost, weighted average cost, RIM or replacement cost to value certain discrete

inventory items under the first-in, first-out method (“FIFO”). The replacement cost approach under the FIFO

method is predominantly utilized in determining the value of high turnover perishable items, including produce,

deli, bakery, meat and floral.

As of February 23, 2013 and February 25, 2012, approximately 23 percent and 22 percent, respectively, of the

Company’s inventories were valued using the cost, weighted average cost and RIM methods under the FIFO

method of inventory accounting. The remaining 17 percent and 18 percent of the Company’s inventories as of

February 23, 2013 and February 25, 2012, respectively, were valued using the replacement cost approach under

the FIFO method of inventory accounting. The replacement cost approach applied under the FIFO method results

in inventories recorded at the lower of cost or market because of the very high inventory turnover and the

resulting low inventory days supply for these items of inventory.

During fiscal 2013, 2012 and 2011, inventory quantities in certain LIFO layers were reduced. These reductions

resulted in a liquidation of LIFO inventory quantities carried at lower costs prevailing in prior years as compared

with the cost of fiscal 2013, 2012 and 2011 purchases. As a result, Cost of sales decreased by $6, $9 and $5 in

fiscal 2013, 2012 and 2011, respectively. If the FIFO method had been used to determine cost of inventories for

which the LIFO method is used, the Company’s inventories would have been higher by approximately $211 and

$207 as of February 23, 2013 and February 25, 2012, respectively.

The Company evaluates inventory shortages throughout each fiscal year based on actual physical counts in its

facilities. Allowances for inventory shortages are recorded based on the results of these counts to provide for

estimated shortages as of the end of each fiscal year.

Long-Lived Assets

The Company monitors the recoverability of its long-lived assets such as buildings and equipment, whenever

events or changes in circumstances indicate that the carrying amount of such assets may not be fully recoverable,

34