Albertsons 2007 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2007 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

SU

PERVAL

U

IN

C

. and

S

ubsidiaries

N

OTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

a

nd measurement of a tax position taken or expected to be taken in a tax return. Additionall

y

, FIN 48 provide

s

g

uidance on subsequent derecognition of tax positions, financial statement classification, recognition of interest

a

n

d

pena

l

t

i

es, account

i

ng

i

n

i

nter

i

m per

i

o

d

s, an

ddi

sc

l

osure an

d

trans

i

t

i

on requ

i

rements. FIN 48

i

se

ff

ect

i

ve

f

or

the Compan

y

’s fiscal

y

ear be

g

innin

g

Februar

y

2

5

, 2007, with earl

y

adoption permitted. The Compan

y

is in the

process of evaluating the impact of adoption of FIN 48.

I

nSe

p

tember 2006, the FASB issued SFAS No. 1

5

7, “Fair Value Measurements” (“SFAS No. 1

5

7”). SFAS

N

o. 157 clarifies the principle that fair value should be based on the assumptions market participants would us

e

w

hen pricin

g

an asset or liabilit

y

and establishes a fair value hierarch

y

that prioritizes the information used t

o

d

evelop those assumptions. Under the standard, fair value measurements would be separatel

y

disclosed b

y

leve

l

w

ithin the fair value hierarchy. SFAS 157 is effective for the Company’s fiscal year beginning February 24

,

2

008, with earl

y

adoption permitted. The Compan

y

is in the process of evaluatin

g

the impact of adoption of

SFAS No. 1

5

7

.

I

n September 2006, the FASB issued SFAS No. 1

5

8, “Emplo

y

ers’ Accountin

g

for Defined Benefit Pension and

Other Postretirement Plans – an amendment of FASB Statements No. 87, 88, 106 and 132

(

R

)

”

(

“SFA

S

N

o. 158”). SFAS No. 158 requires an employer that sponsors one or more single-employer defined benefit plan

s

to (a) reco

g

nize the overfunded or underfunded status of a benefit plan in its statement of financial position,

(b

) recogn

i

ze as a component o

f

ot

h

er compre

h

ens

i

ve

i

ncome, net o

f

tax, t

h

ega

i

ns or

l

osses an

d

pr

i

or serv

i

ce

costs or cre

di

ts t

h

at ar

i

se

d

ur

i

n

g

t

h

e per

i

o

db

ut are not reco

g

n

i

ze

d

as components o

f

net per

i

o

di

c

b

ene

fi

t cost

pursuant to SFAS No. 87, “Emplo

y

ers’ Accountin

g

for Pensions”, or SFAS No. 106, “Emplo

y

ers’ Accountin

g

f

or Postret

i

rement Bene

fi

ts Ot

h

er T

h

an Pens

i

ons”, (c) measure

d

e

fi

ne

db

ene

fi

tp

l

an assets an

d

o

bli

gat

i

ons as o

f

t

h

e

d

ate o

f

t

h

e emp

l

o

y

er’s

fi

sca

ly

ear-en

d

,an

d

(

d

)

di

sc

l

ose

i

nt

h

e notes to

fi

nanc

i

a

l

statements a

ddi

t

i

ona

l

information about certain effects on net periodic benefit cost for the next fiscal

y

ear that arise from dela

y

e

d

recognition of the gains or losses, prior service costs or credits, and transition asset or obligation. SFAS No. 15

8

is effective for the Compan

y

’s fiscal

y

ear endin

g

Februar

y

24, 2007. The adoption of SFAS No. 158 and its

effects are described in Note 1

5

—Benefit Plans

.

I

n September 2006, the SEC issued Staff Accountin

g

Bulletin No. 108, “Considerin

g

the Effects of Prior Year

M

isstatements when Quantifying Misstatements in Current Year Financial Statements” (“SAB 108”). SAB 108

prov

id

es

i

nterpret

i

ve gu

id

ance on

h

ow t

h

ee

ff

ects o

f

t

h

e carryover or reversa

l

o

f

pr

i

or year m

i

sstatements s

h

ou

ld

b

e considered in quantif

y

in

g

a current

y

ear misstatement. The Securities and Exchan

g

e Commission staf

f

b

elieves that registrants should quantify errors using both a balance sheet and an income statement approach and

eva

l

uate w

h

et

h

er e

i

t

h

er approac

h

resu

l

ts

i

n quant

if

y

i

ng a m

i

sstatement t

h

at, w

h

en a

ll

re

l

evant quant

i

tat

i

ve an

d

qualitative factors are considered, is material. SAB 108 is effective for the Compan

y

’s fiscal

y

ear endin

g

F

ebruary 24, 2007 and did not have a material effect on the Company’s consolidated financial statements

.

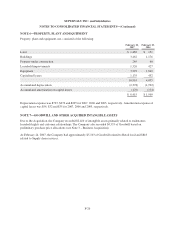

N

O

TE 5—

C

L

OS

ED PR

O

PERTIE

S

AND A

SS

ET IMPAIRMENT

C

HAR

G

E

S

Durin

g

fiscal 2007, the Compan

y

committed to a plan to dispose of 18 Scott’s retail stores. Related to thi

s

d

isposition, the Company recorded a fourth quarter pre-tax charge of

$

26 million, which includes property, plan

t

a

nd equipment related impairment char

g

es of $6,

g

oodwill impairment char

g

es of $19 and other char

g

es of $1

.

During fiscal 200

6

, the Company announced the plans to dispose of twenty corporate operated Shop ’n Save

retail stores in Pittsbur

g

h. Related to this disposition, the Compan

y

recorded a char

g

e of $65 million, whic

h

included property, plant and equipment related impairment charges of

$

52 million, goodwill impairment charges

o

f

$

7 million and other charges of

$

6 million.

During fiscal 200

6

, the Company sold 2

6

Cub Foods stores located primarily in the Chicago area to the Cerberu

s

Group for a pre-tax and after-tax loss of approximatel

y

$95 and $61, respectivel

y

. The pre-tax loss is included in

Sellin

g

and administrative expenses on the Consolidated Statements of Earnin

g

s.

F

-

24