Albertsons 2007 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2007 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

SU

PERVAL

U

IN

C

. and

S

ubsidiaries

N

OTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

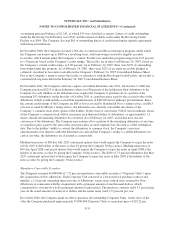

N

O

TE 4—NEW AND RE

C

ENTLY AD

O

PTED A

CCOU

NTIN

GS

TANDARD

S

I

n December 2004, the Financial Accountin

g

Standards Board (“FASB”) issued SFAS No. 123 (Revised 2004)

,

“Share Based Payment” (“SFAS No. 123(R)”). SFAS No. 123(R) addresses the accounting for share-based

payments,

i

nc

l

u

di

ng grants o

f

emp

l

oyee stoc

k

opt

i

ons. Un

d

er t

h

e new stan

d

ar

d

, compan

i

es are no

l

onger a

bl

et

o

a

ccount for share-based compensation transactions usin

g

the intrinsic value method in accordance with

Accounting Principles Board (“APB”) Opinion No. 2

5

, “Accounting for Stock Issued to Employees” (“APB

Opinion No. 25”). Instead, companies are required to account for such transactions using a fair-value method and

reco

g

nize the expense in their consolidated statements of earnin

g

s. SFAS No. 123(R) and related FASB Staf

f

Positions became effective for the Company on February 26, 2006. The adoption of SFAS No. 123(R) and its

e

ff

ects are

d

escr

ib

e

di

n Note 12—Stoc

k

-Base

d

Compensat

i

on.

I

n November 2004, the FASB issued SFAS No. 1

5

1, “Inventory Costs, an Amendment of ARB No. 43, Chapter

4

” (“SFAS No. 151”). SFAS No. 151 clarifies that inventory costs that are “abnormal” are required to be charge

d

to expense as incurred as opposed to bein

g

capitalized into inventor

y

as a product cost. SFAS No. 1

5

1 provide

s

examples of “abnormal” costs to include costs of idle facilities, excess freight and handling costs, and wasted

materials (spoilage). SFAS No. 151 became effective for the Company on February 26, 2006 and did not have

a

material effect on the Compan

y

’s consolidated financial statements.

I

n December 2004, the FASB issued SFAS No. 153, “Exchanges of Nonmonetary Assets, an amendment of AP

B

O

p

inion No. 29” (“SFAS No. 1

5

3”). SFAS No. 1

5

3 amends APB O

p

inion No. 29 to eliminate the exce

p

tion fo

r

nonmonetary exchanges of similar productive assets and replaces it with a general exception for exchanges o

f

nonmonetary assets t

h

at

d

o not

h

ave commerc

i

a

l

su

b

stance. A nonmonetary exc

h

ange

h

as commerc

i

a

l

su

b

stanc

e

if the future cash flows of the entit

y

are expected to chan

g

esi

g

nificantl

y

as a result of the exchan

g

e. SFAS

N

o. 1

5

3 became effective for the Company on February 26, 2006 and did not have a material effect on th

e

C

ompany’s conso

lid

ate

dfi

nanc

i

a

l

statements

.

I

n May 200

5

, the FASB issued SFAS No. 1

5

4, “Accounting Changes and Error Corrections—a Replacement of

APB Opinion No. 20 and FASB Statement No. 3” (“SFAS No. 154”). SFAS No. 154 requires retrospective

a

pplication as the required method for reportin

g

a chan

g

e in accountin

g

principle, unless impracticable or unles

s

a

pronouncement includes alternative transition provisions. SFAS No. 1

5

4 also requires that a change in

d

eprec

i

at

i

on, amort

i

zat

i

on or

d

ep

l

et

i

on met

h

o

df

or

l

ong-

li

ve

d

, non-

fi

nanc

i

a

l

assets

b

e accounte

df

or as a c

h

ang

e

in accountin

g

estimate effected b

y

a chan

g

e in accountin

g

principle. This statement carries forward the

g

uidanc

e

in APB Opinion No. 20, “Accounting Changes,” for the reporting of a correction of an error and a change i

n

a

ccounting estimate. SFAS No. 154 became effective for the Company on February 26, 2006 and did not have a

material effect on the Compan

y

’s consolidated financial statements.

I

n June 200

6,

the FASB ratified the consensuses of EITF Issue No. 0

6

-3

,

“How Taxes Collected from Customers

a

nd Remitted to Governmental Authorities Should Be Presented in the Income Statement (That Is, Gross versus

N

et Presentation)” (“EITF 06-3”). EITF 06-3 indicates that the income statement presentation on either a gros

s

b

as

i

s or a net

b

as

i

so

f

t

h

e taxes w

i

t

hi

nt

h

e scope o

f

t

h

e

i

ssue

i

s an account

i

ng po

li

cy

d

ec

i

s

i

on. T

h

e Company’

s

a

ccountin

g

polic

y

is to present the taxes within the scope of EITF 0

6

-3 on a net basis. The adoption of EITF 0

6

-

3

in the first fiscal quarter of 2007 did not result in a change to the Company’s accounting policy and, accordingly,

did

not

h

ave a mater

i

a

l

e

ff

ect on t

h

e Company’s conso

lid

ate

dfi

nanc

i

a

l

statements.

I

n July 2006, the FASB issued Interpretation No. 48, “Accounting for Uncertainty in Income Taxes—an

I

nterpretat

i

on o

f

FASB Statement No. 109” (“FIN 48”). FIN 48 c

l

ar

ifi

es t

h

e account

i

ng

f

or uncerta

i

nty

i

n

i

ncome

taxes reco

g

nized in an entit

y

’s financial statements in accordance with SFAS No. 109, “Accountin

g

for Income

T

axes,” and prescribes a recognition threshold and measurement attribute for the financial statement recognitio

n

F-

23