Xcel Energy 2003 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2003 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

66 XCEL ENERGY 2003 ANNUAL REPORT

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Cash Flows Cash funding requirements can be impacted by changes to actuarial assumptions, actual asset levels and other pertinent calculations

prescribed by the funding requirements of income tax and other pension-related regulations. These regulations did not require cash funding in the years

2001 through 2003 for Xcel Energy’s pension plans, and is not expected to require cash funding in 2004. PSCo elected to make a voluntary contribution

of $30 million to its pension plan for bargaining employees in 2003, and it plans to voluntarily contribute another $10 million to the plan in 2004.

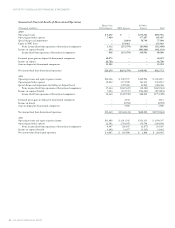

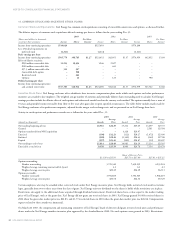

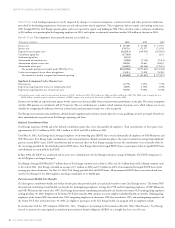

Benefit Costs The components of net periodic pension cost (credit) are:

(Thousands of dollars) 2003 2002 2001

Service cost $ 67,449 $ 65,649 $ 57,521

Interest cost 170,731 172,377 172,159

Expected return on plan assets (322,011) (339,932) (325,635)

Curtailment (gain) loss (17,363) – 1,121

Settlement (gain) loss (1,135) ––

Amortization of transition asset (1,996) (7,314) (7,314)

Amortization of prior service cost 28,230 22,663 20,835

Amortization of net gain (44,825) (69,264) (72,413)

Net periodic pension cost (credit) under SFAS No. 87(a) $(120,920) $(155,821) $(153,726)

Credits not recognized due to effects of regulation 51,311 71,928 76,509

Net benefit cost (credit) recognized for financial reporting $ (69,609) $ (83,893) $ (77,217)

Significant Assumptions Used to Measure Costs

Discount rate 6.75% 7.25% 7.75%

Expected average long-term increase in compensation level 4.00% 4.50% 4.50%

Expected average long-term rate of return on assets 9.25% 9.50% 9.50%

(a) Includes pension credits related to discontinued operations of $18.7 million for 2003, $9.6 million for 2002, and $8.2 million for 2001. The 2003 credit is largely due to a

$20.0 million curtailment gain related to termination of NRG employees as a result of the divestiture of NRG in December 2003.

Pension costs include an expected return impact for the current year that may differ from actual investment performance in the plan. The return assumption

used for 2004 pension cost calculations will be 9.0 percent. The cost calculation uses a market-related valuation of pension assets, which reduces year-to-year

volatility by recognizing the differences between assumed and actual investment returns over a five-year period.

Xcel Energy also maintains noncontributory, defined-benefit supplemental-retirement-income plans for certain qualifying executive personnel. Benefits for

these unfunded plans are paid out of Xcel Energy’s operating cash flows.

Defined Contribution Plans

Xcel Energy maintains 401(k) and other defined contribution plans that cover substantially all employees. Total contributions to these plans were

approximately $15.9 million in 2003, $18.3 million in 2002, and $29.0 million in 2001.

Until May 6, 2002, Xcel Energy had a leveraged employee stock ownership plan (ESOP) that covered substantially all employees of NSP-Minnesota and

NSP-Wisconsin. Xcel Energy made contributions to this noncontributory, defined contribution plan to the extent it realized tax savings from dividends

paid on certain ESOP shares. ESOP contributions had no material effect on Xcel Energy earnings because the contributions were essentially offset by

the tax savings provided by the dividends paid on ESOP shares. Xcel Energy allocated leveraged ESOP shares to participants when it repaid ESOP loans

with dividends on stock held by the ESOP.

In May 2002, the ESOP was terminated and its assets were combined into the Xcel Energy retirement savings 401(k) plan. The ESOP component of

the 401(k) plan is no longer leveraged.

Xcel Energy’s leveraged ESOP held 10.7 million shares of Xcel Energy common stock at May 6, 2002, and 10.5 million shares of Xcel Energy common stock

at the end of 2001. Xcel Energy excluded an average of 0.7 million in 2002 and 0.9 million in 2001 of uncommitted leveraged ESOP shares from

earnings-per-share calculations. On Nov. 19, 2002, Xcel Energy paid off all of the ESOP loans. All uncommitted ESOP shares were released and were

used by Xcel Energy for the 2002 employer matching contribution to its 401(k) plan.

Postretirement Health Care Benefits

Xcel Energy has contributory health and welfare benefit plans that provide health care and death benefits to most Xcel Energy retirees. The former NSP

discontinued contributing toward health care benefits for nonbargaining employees retiring after 1998 and for bargaining employees of NSP-Minnesota

and NSP-Wisconsin who retired after 1999. Xcel Energy discontinued contributing toward health care benefits for former NCE nonbargaining employees

retiring after June 30, 2003. Employees of the former NCE who retired in 2002 continue to receive employer-subsidized health care benefits. Nonbargaining

employees of the former NSP who retired after 1998; bargaining employees of the former NSP who retired after 1999; and nonbargaining employees of

the former NCE who retired after June 30, 2003, are eligible to participate in the Xcel Energy health care program with no employer subsidy.

In conjunction with the 1993 adoption of SFAS No. 106 – “Employers’ Accounting for Postretirement Benefits Other Than Pension,” Xcel Energy

elected to amortize the unrecognized accumulated postretirement benefit obligation (APBO) on a straight-line basis over 20 years.