Xcel Energy 2003 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2003 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

28 XCEL ENERGY 2003 ANNUAL REPORT

MANAGEMENT’S DISCUSSION AND ANALYSIS

Utility Industry Changes

The structure of the electric and natural gas utility industry has been subject to change. Merger and acquisition activity in the past has been significant

as utilities combined to capture economies of scale or establish a strategic niche in preparing for the future, although such activity slowed substantially

after 2001. All utilities were required to provide nondiscriminatory access to the use of their transmission systems in 1996. In addition, the FERC issued

a series of regulatory orders in 2003. These orders, among other things, standardized the methods and pricing of power generation interconnections,

established new standards of conduct rules for transmission providers and new code of conduct rules for utilities with market-based rate authority.

Xcel Energy has not yet estimated the full impact of the new FERC regulatory orders, but it could be material.

Some states had begun to allow retail customers to choose their electricity supplier, while other states have delayed or canceled industry restructuring.

There were no significant retail electric or natural gas restructuring efforts in the states served by Xcel Energy in 2003.

Xcel Energy cannot predict the outcome of restructuring proceedings in the electric utility jurisdictions it serves at this time. The resolution of these

matters may have a significant impact on the financial position, results of operations and cash flows of Xcel Energy.

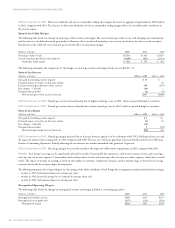

Pension Plan Costs and Assumptions

Xcel Energy’s pension costs are based on an actuarial calculation that includes a number of key assumptions, most notably the annual return level that

pension investment assets will earn in the future and the interest rate used to discount future pension benefit payments to a present value obligation for

financial reporting. In addition, the actuarial calculation uses an asset-smoothing methodology to reduce the volatility of varying investment performance

over time. Note 12 to the Consolidated Financial Statements discusses the rate of return and discount rate used in the calculation of pension costs and

obligations in the accompanying financial statements.

Pension costs have been increasing in recent years, and are expected to increase further over the next several years, due to lower-than-expected

investment returns experienced in 2000, 2001 and 2002 and decreases in interest rates used to discount benefit obligations. While investment

returns exceeded the assumed level of 9.25 percent in 2003, investment returns in 2001 and 2002 were below the assumed level of 9.5 percent and

discount rates have declined from the 7.25-percent to 8-percent levels used in 1999 through 2002 cost determinations to 6.75 percent used in

2003. Xcel Energy continually reviews its pension assumptions and, in 2004, expects to change the investment return assumption to 9.0 percent

and the discount rate assumption to 6.25 percent.

The investment gains or losses resulting from the difference between the expected pension returns assumed on smoothed or “market-related” asset levels

and actual returns earned is deferred in the year the difference arises and recognized over the subsequent five-year period. This gain or loss recognition

occurs by using a five-year, moving-average value of pension assets to measure expected asset returns in the cost determination process, and by amortizing

deferred investment gains or losses over the subsequent five-year period. Based on the use of average market-related asset values, and considering the

expected recognition of past investment gains and losses over the next five years, achieving the assumed rate of asset return of 9.0 percent in each future

year and holding other assumptions constant, Xcel Energy currently projects that the pension costs recognized for financial reporting purposes in continuing

operations will increase from a credit, or negative expense, of $51 million in 2003 to a credit of $25 million in 2004 and zero in 2005. Pension costs are

currently a credit due to the recognized investment asset returns exceeding the other pension cost components, such as benefits earned for current service

and interest costs for the effects of the passage of time on discounted obligations.

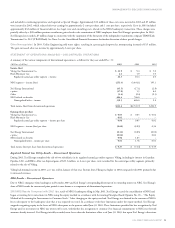

Xcel Energy bases its discount rate assumption on benchmark interest rates quoted by an established credit rating agency, Moody’s Investors Service

(Moody’s), and has consistently benchmarked the interest rate used to derive the discount rate to the movements in the long-term corporate bond indices

for bonds rated Aaa through Baa by Moody’s, which have a period to maturity comparable to our projected benefit obligations. At Dec. 31, 2003, the

annualized Moody’s Aa index rate, roughly in the middle of the Aaa and Baa range, declined by about 0.5 percent from the prior year end, which resulted

in a corresponding decrease from 6.75 percent at year-end 2002 to a 6.25-percent pension discount rate at year-end 2003. This rate was used to value

the actuarial benefit obligations at that date, and will be used in 2004 pension cost determinations.

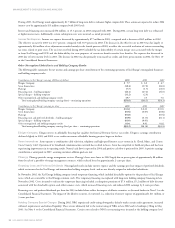

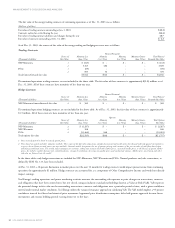

If Xcel Energy were to use alternative assumptions for pension cost determinations, a 1-percent change would result in the following impacts on the

estimated pension costs recognized by Xcel Energy for financial reporting purposes:

–a 100 basis point higher rate of return, 10.0 percent, would decrease 2004 pension costs by $18.4 million;

–a 100 basis point lower rate of return, 8.0 percent, would increase 2004 pension costs by $18.4 million;

–a 100 basis point higher discount rate, 7.25 percent, would decrease 2004 pension costs by $9.5 million; and

–a 100 basis point lower discount rate, 5.25 percent, would increase 2004 pension costs by $8.8 million.

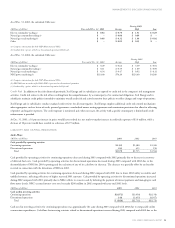

Alternative Employee Retirement Income Security Act of 1974 (ERISA) funding assumptions would also change the expected future cash funding requirements

for the pension plans. Cash funding requirements can be affected by changes to actuarial assumptions, actual asset levels and other calculations prescribed by

the funding requirements of income tax and other pension-related regulations. These regulations did not require cash funding in recent years for Xcel

Energy’s pension plans, and do not require funding in 2004. Assuming that future asset return levels equal the actuarial assumption of 9.0 percent for the

years 2004 and 2005, Xcel Energy projects, under current funding regulations, that cash funding would be required in the amount of approximately

$0 million for 2005 and $15 million for 2006. Actual performance can affect these funding requirements significantly. Current funding regulations

were under legislative review in 2004 and, if not retained in their current form, could change these funding requirements materially. To begin meeting