Xcel Energy 2003 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2003 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

|

|

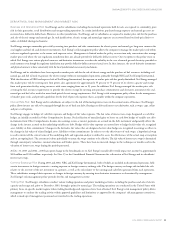

32 XCEL ENERGY 2003 ANNUAL REPORT

MANAGEMENT’S DISCUSSION AND ANALYSIS

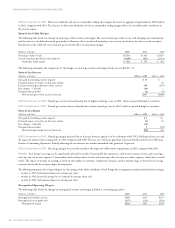

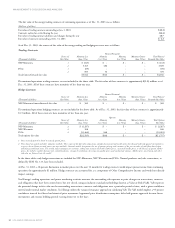

Accounting Policy Judgments/Uncertainties Affecting Application See Additional Discussion At

Income Tax Accruals –Application of tax statutes and regulations Management’s Discussion and Analysis:

to transactions Factors Affecting Results of Continuing Operations

–Anticipated future decisions of tax authorities Tax Matters

–Ability of tax authority decisions/positions to Notes to Consolidated Financial Statements

withstand legal challenges and appeals Notes 1, 10 and 17

–Ability to realize tax benefits through carrybacks

to prior periods or carryovers to future periods

Benefit Plan Accounting –Future rate of return on pension and other plan Management’s Discussion and Analysis:

assets, including impacts of any changes to Factors Affecting Results of Continuing Operations

investment portfolio composition Pension Plan Costs and Assumptions

–Discount rates used in valuing benefit obligation Notes to Consolidated Financial Statements

–Actuarial period selected to recognize deferred Notes 1 and 12

investment gains and losses

Asset Valuation –Regional economic conditions affecting asset Management’s Discussion and Analysis:

operation, market prices and related cash flows Results of Operations

–Foreign currency valuations changes Statement of Operations Analysis – Discontinued Operations

–Regulatory and political environments and Factors Affecting Results of Continuing Operations

requirements Impact of Nonregulated Investments

–Levels of future market penetration and Notes to Consolidated Financial Statements

customer growth Note 3

Xcel Energy continually makes informed judgments and estimates related to these critical accounting policy areas, based on an evaluation of the varying

assumptions and uncertainties for each area. For example:

–probable outcomes of regulatory proceedings are assessed in cases of requested cost recovery or other approvals from regulators;

–the ability to operate plant facilities and recover the related costs over their useful operating lives, or such other period designated by our regulators,

is assumed;

–probable outcomes of reviews and challenges raised by tax authorities, including appeals and litigation where necessary, are assessed;

–returns are projected regarding earnings on pension investments, and the salary increases provided to employees over their periods of service; and

–future cash inflows of operations are projected in order to assess whether they will be sufficient to recover future cash outflows, including the impacts

of product price changes and market penetration to customer groups.

The information and assumptions underlying many of these judgments and estimates will be affected by events beyond the control of Xcel Energy, or

otherwise change over time. This may require adjustments to recorded results to better reflect the events and updated information that becomes available.

The accompanying financial statements reflect management’s best estimates and judgments of the impacts of these factors as of Dec. 31, 2003.

Recently Implemented Accounting Changes

For a discussion of accounting changes implemented in 2003 and other significant accounting policies, see Notes 1, 16 and 18 to the Consolidated

Financial Statements.

Pending Accounting Changes

FASB Interpretation No. 46 (FIN No. 46) In January 2003, the Financial Accounting Standards Board (FASB) issued FIN No. 46, requiring an

enterprise’s consolidated financial statements to include subsidiaries in which the enterprise has a controlling financial interest. Historically, consolidation

has been required only for subsidiaries in which an enterprise has a majority voting interest. Under FIN No. 46, an enterprise’s consolidated financial

statements will include the consolidation of variable interest entities, which are entities in which the enterprise has a controlling financial interest.

As a result, Xcel Energy expects that it will be required to consolidate all or a portion of its affordable housing investments made through Eloigne,

which currently are accounted for under the equity method. The Xcel Energy utility subsidiaries are party to purchased power agreements, and based

on the current guidance, these contracts are not expected to be considered variable interest arrangements under the provisions of FIN No. 46. However,

Xcel Energy is still evaluating the issue. Additionally, Xcel Energy is evaluating other arrangements based on criteria in FIN No. 46, and it is likely

that some arrangements will require consolidation.

As of Dec. 31, 2003, the assets of the affordable housing investments were approximately $142 million and long-term liabilities were approximately

$78 million. Currently, investments of $56 million are reflected as a component of investments in unconsolidated affiliates in the Dec. 31, 2003,

Consolidated Balance Sheet. FIN No. 46 requires that for entities to be consolidated, the entities’ assets be initially recorded at their carrying amounts at

the date the new requirement first applies. If determining carrying amounts as required is impractical, the assets are to be measured at fair value as of the

first date the new requirements apply. Any difference between the net consolidated amounts added to Xcel Energy’s balance sheet and the amount of any

previously recognized interest in the newly consolidated entity should be recognized in earnings as the cumulative-effect adjustment of an accounting

change. Xcel Energy plans to adopt FIN No. 46 in the first quarter of 2004. The impact of consolidating these entities is not expected to have a material

impact on net income.