Volvo 1997 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 1997 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

|

|

35

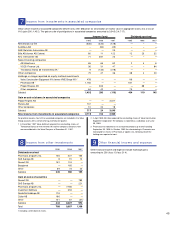

their contractual obligations, based on individual assessments. In addition, central

provisions are made for each sales-financing company for credit and residual

value risks. At year-end 1997, these central provisions corresponded to 2.3% of

the value of the credit portfolio. Considering that the sales-financing operations

entail a major undertaking in specific countries, an additional provision of

SEK 300 M was made, which is not charged against the sales-financing opera-

tions. As a result, total central reserves amount to 3.0% of the credit portfolio.

Realized losses for sales-financing operations which were charged against opera-

ting income in 1997 amounted to 0.2% of the credit portfolio.

Treasury

Volvo Group Finance

Volvo Group Finance Sweden AB and subsidiaries carry out most of Volvo’s

financial transactions. Coordinated financial management offers better opportun-

ities to utilize Volvo’s financial assets and cash flow effectively and to manage

risks related to financial management in a professional manner. Financial man-

agement is divided into two main areas: internal-bank activities and risk manage-

ment. The internal bank is responsible for optimizing the balance sheet as well

as the flow of payments and currencies. Risk management is responsible for

dealing with various types of financial risks in Volvo’s business, and for taking

advantage of market opportunities to improve Volvo’s net interest position.

Volvo Group Finance is active through subsidiaries in Europe, Asia and North

America. In December 1997 it was decided to transfer the operations in the sub-

sidiary Volvo Group Finance Europe B.V. to the parent company. The decision

was made with a view to further integrate the business.

Effective in 1998, Volvo Group Finance Sweden AB and its subsidiaries are

responsible for managing the Volvo Group’s net interest income/expense.

Insurance

Försäkrings AB Volvia offers direct-writing automobile insurance to owners of

Volvo and Renault cars in Sweden and, since the autumn of 1997, in Finland.

The company has cooperation agreements with both the Dial and Skandia

insurance companies, as well as reinsurance agreements with companies in

Norway and Great Britain. Volvia’s share of the market for insurance on Volvo

and Renault cars in Sweden increased to 35% (33) in 1997.

Volvo Group Insurance Försäkrings AB and its subsidiaries in Luxembourg

and Ireland constitute an important part of the Group’s risk-management opera-

tions. These so-called captive companies reinsure the greater part of the internal

risks in the property insurance sector.

The Volvo Group’s financial risks are described in Note 30 on page 53.

Risk exposure

Volvo’s finance operations are controlled by

groupwide policies which are revised annually

and thereafter approved by AB Volvo’s Board

of Directors. These policies pertain primarily to

various types of financial risks such as curren-

cy exposure, m atching of liquidity and interest

term s. In addition som e segm ents of sales

financing result in specific credit risk s and

residual risks.

Credit risks in sales financing

Volvo’s sales financing involves credit risks dis-

tributed am ong a large number of individual

end-custom ers and dealers. Collateral is in the

form of the financed products. In granting

credit, a balance between risk exposure and

expected return is sought. These activities are

guided by com m on policies for credit and rules

for customer classification. The credit portfolio

should be well distributed between various

custom er categories and individual industries.

Credit risks are m anaged through active credit

monitoring and routines for follow-up, and in

certain cases repossession of the products.

In addition, provisions are m ade to credit risk

reserves.

Residual value risk in sales financing

Residual value risks are attributable to con-

tracts involving operational leasing. It involves

the risk that the value of the leased item at

expiration of the leasing contract is different

than what was anticipated when the operation-

al leasing contract was concluded. This means

that the lessor may be forced to liquidate the

products at a loss. Residual value risk s are

managed through having a good k nowledge

about the m arket, know-how about the prod-

uct and price trends as well as activities to

support the second-hand value of the products.

In addition, provisions are made to residual

value reserves to balance the differences be-

tween anticipated and actual residual value.

Interest-rate and liquidity risks

in sales financing

Interest rate changes that occur during a con-

tract’s term m ay affect earnings. As a result,

the highest degree of matching of fixed

periods for borrowing and lending is sought.

At year end 1997, the degree of m atching was

about 90%.

In a com parable manner, the term of bor-

rowing shall correlate with the term of the con-

tract. This degree of m atching was also about

90% at year-end 1997.