U-Haul 2006 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2006 U-Haul annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

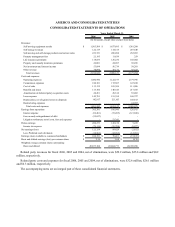

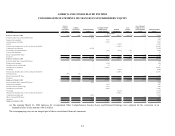

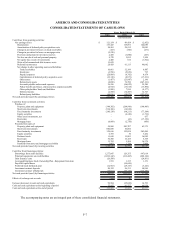

AMERCO AND CONSOLIDATED ENTITIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS -- (CONTINUED)

Cash and Cash Equivalents

The Company considers cash equivalents to be highly liquid debt securities with insignificant interest rate risk with

original maturities from the date of purchase of three months or less.

Financial Instruments that potentially subject the Company to concentrations of credit risk consist principally of cash

deposits. Accounts at each United States financial institution are insured by the Federal Deposit Insurance Corporation

(FDIC) up to $100,000. Accounts at each Canadian financial institution are insured by the Canada Deposit Insurance

Corporation (CDIC) up to $100,000 CAD per account. At March 31, 2006, and March 31, 2005, the Company had

approximately $143.8 million and $44.5 million, respectively, in excess of FDIC and CDIC insured limits. To mitigate this

risk, the Company selects financial institutions based on their credit ratings and financial strength.

Investments

Fixed Maturities. Fixed maturity investments consist of either marketable debt or redeemable preferred stocks. As of

the balance sheet dates, these investments are classified as available-for-sale or held-to-maturity investments are recorded at

cost, as adjusted for the amortization of premiums or the accretion of discounts. Available-for-sale investments are

reported at fair value, with unrealized gains or losses recorded net of taxes and applicable adjustments to deferred policy

acquisition costs in stockholders’ equity. Fair value for these investments is based on quoted market prices, dealer quotes

or discounted cash flows. The cost of investments sold is based on the specific identification method.

For investments accounted for under FAS 115, in determining if and when a decline in market value below amortized

cost is an other than a temporary impairment, management makes certain assumptions or judgments in its assessment

including but not limited to: ability to hold the security, quoted market prices, dealer quotes, discounted cash flows,

industry factors, financial factors, and issuer specific information. Other than temporary impairments, to the extent of the

decline, as well as realized gains or losses on the sale or exchange of investments are recognized in the current period

operating results.

Mortgage Loans and Notes on Real Estate. Mortgage loans and notes on real estate are reported at their unpaid balance,

net of any allowance for possible losses and any unamortized premium or discount.

Recognition of Investment Income. Interest income from bonds and mortgage notes is recognized when it becomes

earned. Dividends on common and preferred stocks are recognized on the ex-dividend dates. Realized gains and losses on

the sale or exchange of investments are recognized at the trade date.

Fair Values

Fair values of cash equivalents approximate cost due to the short period of time to maturity. Fair values of short-term

investments, investments available-for-sale, long-term investments, mortgage loans and notes on real estate, and interest

rate cap and swap contracts are based on quoted market prices, dealer quotes or discounted cash flows. Fair values of trade

receivables approximate their recorded value.

Limited credit risk exists on trade receivables due to the diversity of our customer base and their dispersion across broad

geographic markets. The Company’ s financial instruments that are exposed to concentrations of credit risk consist primarily

of temporary cash investments, trade receivables and notes receivable. The Company places its temporary cash investments

with financial institutions and limits the amount of credit exposure to any one financial institution.

The Company has mortgage receivables, which potentially expose the Company to credit risk. The portfolio of notes is

principally collateralized by mini-warehouse storage facilities and other residential and commercial properties. The

Company has not experienced losses related to the notes from individual notes or groups of notes in any particular industry

or geographic area. The estimated fair values were determined using the discounted cash flow method and using interest

rates currently offered for similar loans to borrowers with similar credit ratings.

Other investments including short-term investments are substantially current or bear reasonable interest rates. As a

result, the carrying values of these financial instruments approximate fair value. The fair value of long-term debt is based

on current rates at which the Company could borrow funds with similar remaining maturities and approximates the carrying

amount due to its recent issuance.

F-10