Tyson Foods 2008 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2008 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

27 2008 Annual Report

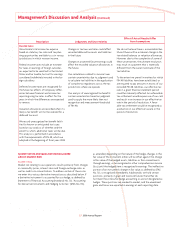

Management’s Discussion and Analysis (continued)

Description Judgments and Uncertainties

Effect if Actual Results Differ

from Assumptions

Income taxes

We estimate total income tax expense

based on statutory tax rates and tax plan-

ning opportunities available to us in various

jurisdictions in which we earn income.

Federal income taxes include an estimate

for taxes on earnings of foreign subsidiar-

ies expected to be remitted to the United

States and be taxable, but not for earnings

considered indefi nitely invested in the for-

eign subsidiary.

Deferred income taxes are recognized for

the future tax effects of temporary differ-

ences between fi nancial and income tax

reporting using tax rates in effect for the

years in which the differences are expected

to reverse.

Valuation allowances are recorded when it is

likely a tax benefi t will not be realized for a

deferred tax asset.

We record unrecognized tax benefi t liabili-

ties for known or anticipated tax issues

based on our analysis of whether, and the

extent to which, additional taxes will be due.

This analysis is performed in accordance

with the requirements of FIN 48, which we

adopted at the beginning of fi scal year 2008.

Changes in tax laws and rates could affect

recorded deferred tax assets and liabilities

in the future.

Changes in projected future earnings could

affect the recorded valuation allowances in

the future.

Our calculations related to income taxes

contain uncertainties due to judgment used

to calculate tax liabilities in the application

of complex tax regulations across the tax

jurisdictions where we operate.

Our analysis of unrecognized tax benefi ts

contain uncertainties based on judgment

used to apply the more likely than not

recognition and measurement thresholds

of FIN 48.

We do not believe there is a reasonable like-

lihood there will be a material change in the

tax related balances or valuation allowances.

However, due to the complexity of some of

these uncertainties, the ultimate resolution

may result in a payment that is materially

different from the current estimate of the

tax liabilities.

To the extent we prevail in matters for which

FIN 48 liabilities have been established, or

are required to pay amounts in excess of our

recorded FIN 48 liabilities, our effective tax

rate in a given fi nancial statement period

could be materially affected. An unfavorable

tax settlement would require use of our cash

and result in an increase in our effective tax

rate in the period of resolution. A favor-

able tax settlement would be recognized as

a reduction in our effective tax rate in the

period of resolution.

QUANTITATIVE AND QUALITATIVE DISCLOSURE

ABOUT MARKET RISK

MARKET RISK

Market risk relating to our operations results primarily from changes

in commodity prices, interest rates and foreign exchange rates, as

well as credit risk concentrations. To address certain of these risks,

we enter into various derivative transactions as described below. If

a derivative instrument is accounted for as a hedge, as defi ned by

Statement of Financial Accounting Standards No. 133, “Accounting

for Derivative Instruments and Hedging Activities” (SFAS No. 133),

as amended, depending on the nature of the hedge, changes in the

fair value of the instrument either will be offset against the change

in fair value of the hedged assets, liabilities or fi rm commitments

through earnings, or be recognized in other comprehensive income

(loss) until the hedged item is recognized in earnings. The ineffective

portion of an instrument’s change in fair value, as defi ned by SFAS

No. 133, is recognized immediately. Additionally, we hold certain

positions, primarily in grain and livestock futures that either do

not meet the criteria for hedge accounting or are not designated as

hedges. These positions are marked to market, and the unrealized

gains and losses are reported in earnings at each reporting date.