Tyson Foods 2008 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2008 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

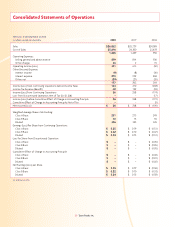

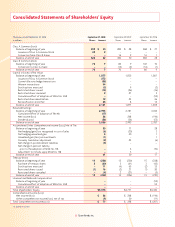

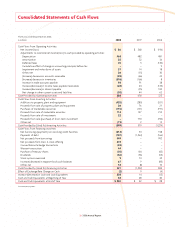

23 2008 Annual Report

Management’s Discussion and Analysis (continued)

be within the control of the entity. FIN 47 requires an entity to

recognize a liability for the fair value of a conditional asset retire-

ment obligation if the fair value of the liability can be reasonably

estimated. Uncertainty about the timing and/or method of settlement

of a conditional asset retirement obligation should be factored into

the measurement of the liability when suffi cient information exists.

We adopted FIN 47 as of September 30, 2006. See Note 2, “Change

in Accounting Principle” in the Notes to Consolidated Financial State-

ments for the impact of the adoption of FIN 47.

RECENTLY ISSUED ACCOUNTING PRONOUNCEMENTS

In September 2006, the FASB issued Statement of Financial Accounting

Standards No. 157, “Fair Value Measurements” (SFAS No. 157). SFAS No. 157

provides guidance for using fair value to measure assets and liabilities.

This standard also responds to investors’ requests for expanded

information about the extent to which companies measure assets

and liabilities at fair value, the information used to measure fair value

and the effect of fair value measurements on earnings. SFAS No. 157

applies whenever other standards require (or permit) assets or liabil-

ities to be measured at fair value. Beginning September 28, 2008,

we partially applied SFAS No. 157 as allowed by FASB Staff Position

(FSP) 157-2, which delayed the effective date of SFAS No. 157 for

nonfi nancial assets and liabilities. As of September 28, 2008, we have

applied the provisions of SFAS No. 157 to our fi nancial instruments

and the impact was not material. Under FSP 157-2, we will be required

to apply SFAS No. 157 to our nonfi nancial assets and liabilities at the

beginning of fi scal 2010. We are currently reviewing the applicability

of SFAS No. 157 to our nonfi nancial assets and liabilities as well as the

potential impact on our consolidated fi nancial statements.

In February 2007, the FASB issued Statement of Financial Accounting

Standards No. 159, “The Fair Value Option for Financial Assets and

Financial Liabilities, including an amendment of FASB Statement

No. 115” (SFAS No. 159). This statement provides companies with an

option to report selected fi nancial assets and liabilities fi rm commit-

ments, and nonfi nancial warranty and insurance contracts at fair value

on a contract-by-contract basis, with changes in fair value recognized

in earnings each reporting period. At September 28, 2008, we did not

elect the fair value option under SFAS No. 159 and therefore there

was no impact to our consolidated fi nancial statements.

In December 2007, the FASB issued Statement of Financial Accounting

Standards No. 160, “Noncontrolling Interests in Consolidated Finan-

cial Statements” (SFAS No. 160). SFAS No. 160 amends Accounting

Research Bulletin No. 51, “Consolidated Financial Statements” to

establish accounting and reporting standards for a noncontrolling

interest in a subsidiary and for the deconsolidation of a subsidiary.

This statement clarifi es that a noncontrolling interest in a subsidiary is

an ownership interest in the consolidated entity and should be

reported as equity in the consolidated fi nancial statements, rather

than in the liability or mezzanine section between liabilities and

equity. SFAS No. 160 also requires consolidated net income be

reported at amounts that include the amounts attributable to

both the parent and the noncontrolling interest. The impact of

SFAS No. 160 will not have a material impact on our current

Consolidated Financial Statements. SFAS No. 160 is effective for

fi scal years, and interim periods within those fi scal years, beginning

on or after December 15, 2008; therefore, we expect to adopt SFAS

No. 160 at the beginning of fi scal 2010.

In December 2007, the FASB issued Statement of Financial Account-

ing Standards No. 141R, “Business Combinations” (SFAS No. 141R). SFAS

No. 141R establishes principles and requirements for how an acquirer

in a business combination: 1) recognizes and measures in its fi nancial

statements identifi able assets acquired, liabilities assumed, and any

noncontrolling interest in the acquiree; 2) recognizes and measures

goodwill acquired in a business combination or a gain from a bargain

purchase; and 3) determines what information to disclose to enable

users of the fi nancial statements to evaluate the nature and fi nancial

effects of a business combination. SFAS No. 141R is effective for busi-

ness combinations for which the acquisition date is on or after the

beginning of the fi rst annual reporting period beginning on or after

December 15, 2008; therefore, we expect to adopt SFAS No. 141R for

any business combinations entered into beginning in fi scal 2010.

In March 2008, the FASB issued Statement of Financial Accounting

Standards No. 161, “Disclosures about Derivative Instruments and

Hedging Activities – an amendment of FASB Statement No. 133” (SFAS

No. 161). SFAS No. 161 establishes enhanced disclosure requirements

about: 1) how and why an entity uses derivative instruments; 2) how

derivative instruments and related hedged items are accounted

for under Statement 133 and its related interpretations; and 3) how

derivative instruments and related hedged items affect an entity’s

fi nancial position, fi nancial performance and cash fl ows. SFAS No. 161

is effective for fi nancial statements issued for fi scal years and interim

periods beginning after November 15, 2008; therefore, we expect to

adopt SFAS No. 161 in the second quarter of fi scal 2009.

In May 2008, the FASB issued FASB Staff Position No. APB 14-1,

“Accounting for Convertible Debt Instruments That May Be Settled

in Cash upon Conversion (Including Partial Cash Settlement)” (FSP

APB 14-1). FSP APB 14-1 specifi es that issuers of convertible debt

instruments that may be settled in cash upon conversion (including

partial cash settlement) should separately account for the liability

and equity components in a manner that will refl ect the entity’s non-

convertible debt borrowing rate when interest cost is recognized in

subsequent periods. The amount allocated to the equity component

represents a discount to the debt, which is amortized into interest

expense using the effective interest method over the life of the debt.

FSP APB 14-1 is effective for fi nancial statements issued for fi scal years

beginning after December 15, 2008, and interim periods within those

fi scal years. Early adoption is not permitted. Therefore, we expect to

adopt the provisions of FSP APB 14-1 beginning in the fi rst quarter of

fi scal 2010. The provisions of FSP APB 14-1 are required to be applied

retrospectively to all periods presented. Upon retrospective adoption,

we anticipate our effective interest rate on our 3.25% Convertible