Tyson Foods 2008 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2008 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

20 Tyson Foods, Inc.

Management’s Discussion and Analysis (continued)

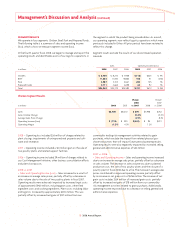

Deterioration of Credit and Capital Markets

Credit market conditions deteriorated rapidly during our fourth

quarter of fi scal 2008 and continue into our fi rst quarter of fi scal

2009. Several major banks and fi nancial institutions failed or were

forced to seek assistance through distressed sales or emergency

government measures. While not all-inclusive, the following

summarizes some of the impacts to our business:

Credit Facilities Cash fl ows from operating activities are our primary

source of liquidity for funding debt service and capital expenditures.

However, we rely on our revolving credit and accounts receivable

securitization facilities to provide additional liquidity for work-

ing capital needs, letters of credit, and as a source of fi nancing for

international growth. Our revolving credit facility has total com-

mitted capacity of $1.0 billion. As of September 27, 2008, we had

outstanding letters of credit totaling $291 million, none of which

were drawn upon, which left $709 million available for borrowing.

Our revolving credit facility is funded by a syndicate of 35 banks,

with commitments ranging from $5 million to $78 million per bank.

If any of the banks in the syndicate were unable to perform on their

commitments to fund the facility, our liquidity could be impaired,

which could reduce our ability to fund working capital needs or

fi nance our international growth strategy.

Our accounts receivable securitization facility has $750 million of

committed funding, of which the entire amount was available for

borrowing as of September 27, 2008. Our accounts receivable

securitization facility is funded by a syndicate of three banks, with

a commitment of $250 million per bank. To date, all of the banks in

the syndicate have continued to meet their commitments despite

the recent market turmoil. If any of the banks in the syndicate were

unable to perform on their commitments to fund the facility, our

liquidity could be impaired, which could reduce our ability to fund

working capital needs or fi nance our international growth strategy.

We have borrowed against this facility subsequent to fi scal 2008

and all of the banks in the syndicate performed their obligations

to fund these borrowings.

Current market conditions have also resulted in higher credit spreads

on long-term borrowings and signifi cantly reduced demand for new

corporate debt issuances.

Equity – Class A Common Stock Equity prices, including our own

Class A Common Stock, have fallen and experienced abnormally

high volatility during the current period. If these conditions persist,

our cost of capital will increase signifi cantly.

Customers/Suppliers The fi nancial condition of some of our

customers and suppliers could also be impaired by current market

conditions. Although we have not experienced a material increase in

customer bad debts or non-performance by suppliers, current market

conditions increase the probability that we could experience losses

from customer or supplier defaults. Should current credit and capital

market conditions result in a prolonged economic downturn in the

United States and abroad, demand for protein products could be

reduced, which could result in a reduction of sales, operating

income and cash fl ows.

Investments The value of our investments in equity and debt securi-

ties, including our marketable debt securities, company-owned life

insurance and pension and other postretirement plan assets, has

been negatively impacted by the recent market declines. These

instruments were recorded at fair value as of September 27, 2008;

however, subsequent to September 27, 2008, through November 1,

2008, we have seen an additional reduction in fair value of approxi-

mately $32 million. While we believe this reduction in fair value

is temporary, if current market conditions continue, we could be

required to recognize $10 million of expense in the fi rst quarter

of fi scal 2009. The remaining change in fair value would be deferred

in other comprehensive income unless determined to be perma-

nently impaired.

We currently oversee two domestic and one foreign subsidiary

non-contributory qualifi ed defi ned benefi t pension plans. All three

pension plans are frozen to new participants and no additional

benefi ts will accrue for participants. Based on our 2008 actuarial

valuation, we anticipate contributions of approximately $1 million

to these plans for fi scal 2009. We also have one domestic unfunded

defi ned benefi t plan. Based on our 2008 actuarial valuation, we

anticipate contributions of approximately $1 million to this plan

in fi scal 2009.

Financial Instruments As part of our commodity risk management

activities, we use derivative fi nancial instruments, primarily futures

and options, to reduce our exposure to various market risks related

to commodity purchases. Similar to the capital markets, the com-

modities markets have seen a similar decline over the past several

months. Grain prices reached an all-time high during our fourth

quarter of fi scal 2008 before falling sharply to the current levels.

While the reduction in grain prices benefi t us long-term, we may be

required to record additional losses related to these fi nancial instru-

ments in the fi rst quarter of fi scal 2009 if grain prices remain lower

than prices at the end of fi scal 2008.

Insurance We rely on insurers as a protection against liability claims,

property damage and various other risks. Our primary insurers main-

tain an A.M. Best Financial Strength Rating of A+ or better. Never-

theless, we continue to monitor this situation as insurers have been

and are expected to continue to be impacted by the current capital

market environment.