Tyson Foods 2008 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2008 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

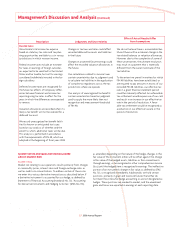

26 Tyson Foods, Inc.

Management’s Discussion and Analysis (continued)

Description Judgments and Uncertainties

Effect if Actual Results Differ

from Assumptions

Goodwill impairment is determined using a

two-step process. The fi rst step is to identify

if a potential impairment exists by compar-

ing the fair value of a reporting unit with its

carrying amount, including goodwill. If the

fair value of a reporting unit exceeds its

carrying amount, goodwill of the reporting

unit is not considered to have a potential

impairment and the second step of the

impairment test is not necessary. However,

if the carrying amount of a reporting unit

exceeds its fair value, the second step is per-

formed to determine if goodwill is impaired

and to measure the amount of impairment

loss to recognize, if any.

The second step compares the implied fair

value of goodwill with the carrying amount

of goodwill. If the implied fair value of

goodwill exceeds the carrying amount,

then goodwill is not considered impaired.

However, if the carrying amount of goodwill

exceeds the implied fair value, an impair-

ment loss is recognized in an amount equal

to that excess.

The implied fair value of goodwill is deter-

mined in the same manner as the amount of

goodwill recognized in a business combina-

tion (i.e., the fair value of the reporting unit

is allocated to all the assets and liabilities,

including any unrecognized intangible assets,

as if the reporting unit had been acquired

in a business combination and the fair value

of the reporting unit was the purchase price

paid to acquire the reporting unit).

For our other intangible assets, if the carry-

ing value of the intangible asset exceeds its

fair value, an impairment loss is recognized

in an amount equal to that excess.

We have elected to make the fi rst day of the

fourth quarter the annual impairment assess-

ment date for goodwill and other intangible

assets. However, we could be required to

evaluate the recoverability of goodwill and

other intangible assets prior to the required

annual assessment if we experience disrup-

tions to the business, unexpected signifi cant

declines in operating results, divestiture of a

signifi cant component of the business or a

sustained decline in market capitalization.

We estimate the fair value of our report-

ing units, generally our operating segments,

using various valuation techniques, with

the primary technique being a discounted

cash fl ow analysis. A discounted cash fl ow

analysis requires us to make various judg-

mental assumptions about sales, operating

margins, growth rates and discount rates.

Assumptions about sales, operating margins

and growth rates are based on our budgets,

business plans, economic projections,

anticipated future cash fl ows and market-

place data. Assumptions are also made for

varying perpetual growth rates for periods

beyond the long-term business plan period.

While estimating the fair value of our Beef

and Chicken reporting units, we assumed

operating margins in future years in excess

of the margins realized in the most cur-

rent year. The fair value estimates for these

reporting units assume normalized operating

margin assumptions and improved operating

effi ciencies based on long-term expectations

and margins historically realized in the beef

and chicken industries. We estimate the fair

value of our Beef reporting unit would be

in excess of its carrying amount, including

goodwill, by sustaining long-term operating

margins of approximately 2.3%. We estimate

the fair value of our Chicken reporting units

would be in excess of its carrying amount,

including goodwill, by sustaining long-term

operating margins of approximately 5.1%.

Other intangible asset fair values have been

calculated for trademarks using a royalty

rate method and using the present value of

future cash fl ows for patents and in-process

technology. Assumptions about royalty

rates are based on the rates at which similar

brands and trademarks are licensed in the

marketplace.

Our impairment analysis contains uncer-

tainties due to uncontrollable events that

could positively or negatively impact the

anticipated future economic and operating

conditions.

We have not made any material changes

in the accounting methodology used to

evaluate impairment of goodwill and other

intangible assets during the last three years.

As a result of the fi rst step of the 2008

goodwill impairment analysis, the fair value

of each reporting unit exceeded its carrying

value. Therefore, the second step was not

necessary. However, a 6% decline in fair value

of our Beef reporting unit or an 11% decline

in fair value of our Chicken reporting unit

would have caused the carrying values for

these reporting units to be in excess of fair

values which would require the second step

to be performed. The second step could

have resulted in an impairment loss for

goodwill.

While we believe we have made reasonable

estimates and assumptions to calculate the

fair value of the reporting units and other

intangible assets, it is possible a material

change could occur. If our actual results

are not consistent with our estimates and

assumptions used to calculate fair value, we

may be required to perform the second step

which could result in a material impairment

of our goodwill.

During the latter part of the fourth quarter

of fi scal 2008 and continuing into November

2008, our market capitalization was below

book value. While we considered the market

capitalization decline in our evaluation of

fair value of goodwill, we determined it did

not impact the overall goodwill impairment

analysis as we believe the decline to be

primarily attributed to the negative market

conditions as a result of the credit crisis,

indications of a possible recession and cur-

rent issues within the poultry industry. We

will continue to monitor our market capital-

ization as a potential impairment indicator

considering overall market conditions and

poultry industry events.

Our fi scal 2008 other intangible asset

impairment analysis did not result in a mate-

rial impairment charge. A hypothetical 10%

decrease in the fair value of intangible assets

would not result in a material impairment.

Impairment of goodwill and other intangible assets