Motorola 2004 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2004 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

56 MANAGEMENT'S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

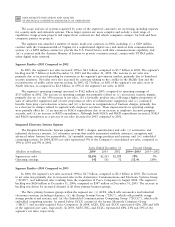

reÖecting increased developmental engineering expenditures due to additional investment in new product

development. The segment's industry typically experiences short life cycles for new products and, therefore, it is

vital to the segment's success that new, compelling products are constantly introduced. Accordingly, a strong

commitment to R&D is required to fuel long-term growth.

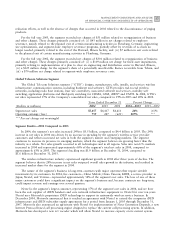

Segment ResultsÌ2003 Compared to 2002

In 2003, the segment's net sales decreased 2% to $11.0 billion, compared to $11.2 billion in 2002. The 2%

decrease in net sales in 2003 reÖected the interaction of a number of factors. In the fourth quarter of 2003,

traditionally the segment's highest sales quarter, the segment was unable to meet demand for shipments of certain

products, primarily those featuring integrated cameras, due to supply constraints for a key component. This had an

adverse eÅect on fourth quarter net sales, which were down 3% from the fourth quarter of 2002. As further

discussed below, the segment's net sales in Asia decreased 42% in 2003, due to ongoing intense competition in that

region, particularly in China, and the impact of Severe Acute Respiratory Syndrome (""SARS'') during the Ñrst half

of the year. Also, in 2002, the segment discontinued sales of paging products. The 2002 results included

$176 million of net sales of paging products, while 2003 did not include paging product sales.

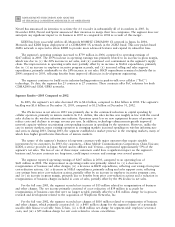

The segment's backlog was $2.2 billion at December 31, 2003, compared to $1.1 billion at December 31,

2002. Backlog increased primarily as a result of demand for new products that were introduced in the second half

of 2003, including handsets with integrated cameras. Backlog was also impacted by the component supply

constraints, which resulted in the segment's inability to meet the demand for certain new products in the fourth

quarter of 2003.

For the full year 2003, the segment believes total industry unit shipments (also referred to as industry ""sell-

in'') increased approximately 20% compared to 2002. This growth was higher than expected by most industry

analysts. Unfortunately, the growth in unit shipments in the segment lagged behind the unit growth in the overall

industry, as unit shipments for the segment grew by only 7% in 2003 compared to 2002. Correspondingly, the

segment's market share is estimated to have declined in 2003.

The 7% increase in unit shipments by the segment was oÅset by a decrease in the segment's ASP, which

declined 8% on an annual basis in 2003. For comparison, the decline in ASP for the segment was 5% in 2002 and

12% in 2001. The overall decline in ASP in 2003 was caused primarily by: (i) a shift in product mix, particularly

during the Ñrst half of the year, toward lower-priced handsets, (ii) the intense competition from new and existing

handset manufacturers in the Asian market, and (iii) unusually high sales of end-of-life products in the third

quarter of 2003, reÖecting the segment's aggressive steps to sell aging inventory. During the second half of 2003, the

segment introduced several feature-rich, higher-tier products, with features including cameras, large color displays,

expanded software applications, messaging functionality, advanced gaming features and an increased opportunity for

personalization. These products began to ship in volume during the fourth quarter of 2003 and, as a result, there

was a sequential increase in ASP from the third quarter to the fourth quarter in 2003.

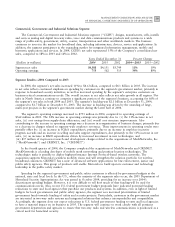

A few customers represented a signiÑcant portion of the segment's net sales in 2003. During 2003, purchases of

iDEN products by Nextel comprised approximately 18% of the segment's net sales, compared to 15% in 2002. In

addition, approximately 9% of the segment's net sales were to the China market and were primarily used on mobile

systems operated by China Mobile and China Unicom, the two largest wireless operators in China. In 2003,

although the U.S. market continued to be the segment's largest market, sales into non-U.S. markets represented

more than half of the segment's total revenue.

The segment's operating earnings in 2003 were $479 million, compared to operating earnings of $503 million

in 2002. The 5% decline in operating earnings was primarily related to: (i) a decline in gross margin, and (ii) an

increase in research and development (R&D) expenditures, partially oÅset by: (i) a decrease in reorganization of

business and other charges, and (ii) a decrease in SG&A expenditures. The decline in gross margin primarily reÖects

the $196 million decline in net sales, which was driven by the 8% decline in ASP and the loss of sales from the

exited paging business. These negative inÖuences were partially oÅset by a decrease in certain manufacturing costs

due to beneÑts from prior and ongoing cost-reduction actions and supply-chain eÇciencies. The increase in R&D

expenditures reÖects an increase in developmental engineering expenditures due to the number of new product

oÅerings by the segment. The segment's industry typically experiences short life cycles for new products and,

therefore, it is vital to the segment's success that new, compelling products are constantly introduced. Accordingly,

a strong commitment to R&D is required to fuel long-term growth. The decrease in SG&A expenditures reÖects a

decline in overall administrative and general spending, which was driven by beneÑts from prior and ongoing cost-