Motorola 2004 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2004 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

99

MOTOROLA INC. AND SUBSIDIARIES NOTES TO

CONSOLIDATED FINANCIAL STATEMENTS(Dollars in millions, except as noted)

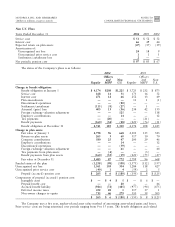

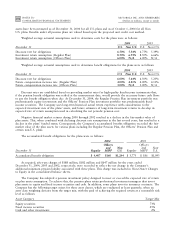

5. Risk Management

Derivative Financial Instruments

Foreign Currency Risk

As a multinational company, the Company's transactions are denominated in a variety of currencies. The

Company uses Ñnancial instruments to hedge, and therefore attempts to reduce its overall exposure to the eÅects of

currency Öuctuations on cash Öows. The Company's policy is not to speculate in Ñnancial instruments for proÑt on

the exchange rate price Öuctuation, trade in currencies for which there are no underlying exposures, or enter into

trades for any currency to intentionally increase the underlying exposure. Instruments that are designated as hedges

must be eÅective at reducing the risk associated with the exposure being hedged and must be designated as a hedge

at the inception of the contract. Accordingly, changes in market values of hedge instruments must be highly

correlated with changes in market values of underlying hedged items both at inception of the hedge and over the

life of the hedge contract.

The Company's strategy in foreign exchange exposure issues is to oÅset the gains or losses of the Ñnancial

instruments against losses or gains on the underlying operational cash Öows or investments based on the operating

business units' assessment of risk. Almost all of the Company's non-functional currency receivables and payables,

which are denominated in major currencies that can be traded on open markets, are hedged. The Company uses

forward contracts and options to hedge these currency exposures. In addition, the Company hedges some Ñrmly

committed transactions and some forecasted transactions. The Company expects that it may hedge investments in

foreign subsidiaries in the future. A portion of the Company's exposure is from currencies that are not traded in

liquid markets and these are addressed, to the extent reasonably possible, through managing net asset positions,

product pricing, and component sourcing.

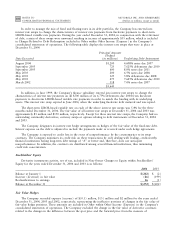

At December 31, 2004 and 2003, the Company had net outstanding foreign exchange contracts totaling

$3.9 billion and $2.7 billion, respectively. Management believes that these Ñnancial instruments should not subject

the Company to undue risk due to foreign exchange movements because gains and losses on these contracts should

oÅset losses and gains on the assets, liabilities and transactions being hedged except for the ineÅective portion of

the instruments which are charged to Other within Other Income (Expense) in the Company's consolidated

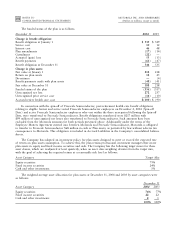

statements of operations. The following table shows, in millions of U.S. dollars, the Ñve largest net foreign

exchange hedge positions as of December 31, 2004 compared to their respective positions at December 31, 2003:

December 31

Buy (Sell)

2004

2003

Euro $(1,588) $(1,114)

Chinese Renminbi (821) (341)

Brazilian Real (318) (172)

Canadian Dollar 212 187

Japanese Yen (179) (29)

The Company is exposed to credit-related losses if counterparties to Ñnancial instruments fail to perform their

obligations. However, it does not expect any counterparties, which presently have high credit ratings, to fail to meet

their obligations.

Interest Rate Risk

At December 31, 2004, the Company's short-term debt of $317 million consisted primarily of $300 million of

commercial paper, priced at short-term interest rates. The Company had $5.0 billion of long-term debt including

current maturities, which is primarily priced at long-term, Ñxed interest rates.