MoneyGram 2004 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2004 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

|

|

Table of Contents

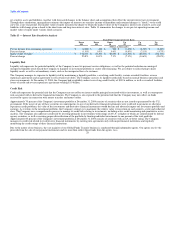

result, we have credit exposure to our agents, which averages approximately $1,100 million, representing a combination of money orders, money transfers and

bill payment proceeds. This credit exposure is spread across almost 27,000 agents, of which 13 owe us in excess of $15.0 million each at any one time. Agents

typically have from one to three days to remit the funds, with longer remittance schedules granted to international agents and certain domestic agents under

certain circumstances. The Company assesses the creditworthiness of each potential agent before accepting it into our distribution network. The Company

actively monitors the credit risk of active agents on an on-going basis by conducting periodic comprehensive financial reviews and cash flow analysis of our

agents who average high volumes of money order sales. In addition, the Company frequently takes additional steps to minimize agent credit risk, such as

requiring owner guarantees, corporate guarantees and other forms of security where appropriate. The Company monitors remittance patterns versus reported

sales by agent on a daily basis. The Company also utilizes software embedded in each point of sale terminal to control both the number and dollar amount of

money orders sold. This software also allows the Company to monitor for suspicious transactions or volumes of sales, assisting the Company in uncovering

irregularities such as money laundering, fraud or agent self-use. Finally, the Company has the ability to remotely disable money order dispensers or

transaction devices to prevent agents from issuing money orders or performing money transfers if suspicious activity is noted or remittances are not received

according to the agent's contract. The point of sale software requires each location to be re-authorized on a daily basis for transaction processing.

Operational Risk

Operational risk represents the risk of direct or indirect loss resulting from inadequate or failed internal processes, people and systems or from external events.

We rely on the ability of our employees and our internal systems and processes to process a large number of transactions in an efficient, uninterrupted and

error-free manner. In addition, we rely on third-party vendors to process and clear our money orders and official checks. We currently rely on ten principal

clearing banks, two of which clear our money orders and eight of which clear our official checks. In the event of a breakdown, security breach or improper

operation of our systems or processes, or improper action by our employees, agents, customer financial institutions or third party vendors, we could suffer

financial loss, loss of customers, regulatory sanctions and damage to our reputation. In addition, we currently operate in approximately 170 countries and plan

to continue to expand our international business. Our ability to grow in international markets and our future results could be harmed by a number of factors,

including changes in political and economic conditions, potential instability in certain regions, changes in foreign policy and adoption of foreign laws

detrimental to our business.

In order to mitigate and control operational risk, we have developed and continue to enhance specific policies and procedures that are designed to identify,

measure, control and manage operational risk at levels we believe are appropriate throughout the organization and within such departments as accounting,

operations, technology, legal and compliance. These control mechanisms attempt to ensure that operations policies and procedures are being followed and that

our various businesses are operating within established corporate policies and limits. We have disaster recovery plans in place that we believe will cover

critical systems on a company-wide basis, and redundancies are built into the systems. We also use periodic self-assessments and internal audit reviews as a

further check on operational risk.

Regulatory Risk

Regulatory risk represents the risk of non-compliance with applicable legal and regulatory requirements. The Company is generally subject to extensive

regulation in the various jurisdictions in which we conduct our business, including state regulation, U.S. federal anti-money laundering laws, the requirements

of the Office of Foreign Assets Control (which prohibit us from transmitting money to specified countries or on behalf of prohibited individuals), the 2001

U.S.A. Patriot Act and foreign regulations. Failure to comply with the laws and regulatory requirements could result in, among other things, revocation of

required licenses or registrations, loss of approved status, termination of contracts with customers and enforcement actions and fines. We have established

procedures that are designed to ensure compliance with applicable regulatory requirements, including those relating to, among others, money laundering,

suspicious activity, privacy and recordkeeping. The Company has a Compliance Officer who is responsible for ensuring compliance with our regulatory

requirements, as well as a team of employees dedicated to maintaining compliance with licensing and reporting obligations and ensuring com-

29