Metro PCS 2009 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2009 Metro PCS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

92

In August 2009, the FASB issued Accounting Standards Update 2009-05 (“ASU 2009-05”), “Measuring

Liabilities at Fair Value,” which updates ASC 820 (Topic 820, “Fair Value Measurements and Disclosures”).

ASU 2009-05 addresses the impact of transfer restrictions on the fair value of a liability that is traded as an asset as

an input to the valuation of the underlying liability, and clarifies when to make adjustments to fair value. ASU

2009-05 is effective for periods ending after August 26, 2009. The implementation of this standard did not have a

material impact on our financial condition, results of operations or cash flows.

In October 2009, the FASB issued Accounting Standards Update 2009-13, “Multiple-Deliverable Revenue

Arrangements - a consensus of the EITF,” (“ASU 2009-13”) which amends ASC 605 (Topic 605, “Revenue

Recognition”). This amended guidance addresses the determination of when individual deliverables within an

arrangement may be treated as separate units of accounting and modifies the manner in which transaction

consideration is allocated across the separately identifiable deliverables. ASU 2009-13 is effective prospectively for

the Company on January 1, 2011, although early adoption is permitted provided that it is retroactively applied to the

beginning of the year of adoption. We have not yet determined the effect on our financial condition or results of

operations upon adoption of ASU 2009-13.

In December 2009, the FASB issued ASU 2009-17, “Amendments to FASB Interpretation 46(R),” (“ASU 2009-

17”) revising authoritative guidance associated with the consolidation of variable interest entities. This revised

guidance replaces the current quantitative-based assessment for determining which enterprise has a controlling

interest in a variable interest entity with an approach that is now primarily qualitative. This qualitative approach

focuses on identifying the enterprise that has (i) the power to direct the activities of the variable interest entity that

can most significantly impact the entity’s performance; and (ii) the obligation to absorb losses and the right to

receive benefits from the entity that could potentially be significant to the variable interest entity. This revised

guidance also requires an ongoing assessment of whether an enterprise is the primary beneficiary of a variable

interest entity rather than a reassessment only upon the occurrence of specific events. ASU 2009-17 was effective

for the Company on January 1, 2010. The implementation of this standard did not have a material impact on our

financial condition, results of operations or cash flows.

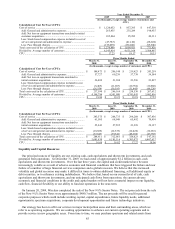

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

Market risk is the potential loss arising from adverse changes in market prices and rates, including interest rates.

We do not routinely enter into derivatives or other financial instruments for trading, speculative or hedging

purposes, unless it is hedging interest rate risk exposure or is required by our senior secured credit facility. We do

not currently conduct business internationally, so we are generally not subject to foreign currency exchange rate

risk.

As of December 31, 2009, we had approximately $1.5 billion in outstanding indebtedness under our senior

secured credit facility that bears interest at floating rates based on the London Inter Bank Offered Rate, or LIBOR,

plus 2.25%. The interest rate on the outstanding debt under our senior secured credit facility as of December 31,

2009 was 6.474%, which includes the impact of our interest rate protection agreements. On November 21, 2006, to

manage our interest rate risk exposure and fulfill a requirement of our senior secured credit facility, we entered into

a three-year interest rate protection agreement. This agreement covers a notional amount of $1.0 billion and

effectively converts this portion of our variable rate debt to fixed-rate debt at an annual rate of 7.169%. The

quarterly interest settlement periods began on February 1, 2007. The interest rate swap agreement expired in

February 2010. On April 30, 2008, to manage our interest rate risk exposure, we entered into a two-year interest

rate protection agreement. The agreement was effective on June 30, 2008, covers a notional amount of $500.0

million and effectively converts this portion of our variable rate debt to fixed rate debt at an annual rate of 5.464%.

The monthly interest settlement periods began on June 30, 2008. The interest rate protection agreement expires on

June 30, 2010. If market LIBOR rates increase 100 basis points over the rates in effect at December 31, 2009,

annual interest expense on the approximate $48.0 million in variable rate debt that is not subject to interest rate

protection agreements would increase approximately $0.5 million.

Item 8. Financial Statements and Supplementary Data

The information required by this item is included in Part IV, Item 15(a)(1) and are presented beginning on Page

F-1.