Kraft 2006 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2006 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

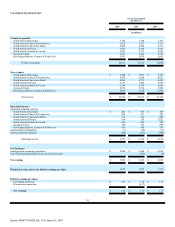

related allowances are not significant to the Company's consolidated financial position or results of operations.

Depreciation, Amortization and Goodwill Valuation. The Company depreciates property, plant and equipment and amortizes definite life intangibles using

the straight-line method over the estimated useful lives of the assets.

The Company is required to conduct an annual review of goodwill and intangible assets for potential impairment. Goodwill impairment testing requires a

comparison between the carrying value and fair value of each reporting unit. If the carrying value exceeds the fair value, goodwill is considered impaired. The

amount of impairment loss is measured as the difference between the carrying value and implied fair value of goodwill, which is determined using discounted

cash flows. Impairment testing for non-amortizable intangible assets requires a comparison between the fair value and carrying value of the intangible asset. If

the carrying value exceeds fair value, the intangible asset is considered impaired and is reduced to fair value. These calculations may be affected by the market

conditions noted below in the Business Environment section and under the "Risk Factors" section in Part 1, Item 1A of this Annual Report on Form 10-K, as well

as interest rates, general economic conditions and projected growth rates. During the first quarter of 2006, the Company completed its annual review of goodwill

and intangible assets and recorded non-cash pre-tax charges of $24 million related to an intangible asset impairment for biscuits assets in Egypt and hot cereal

assets in the United States. Additionally, in 2006, as part of the sale of its pet snacks brand and assets, the Company recorded non-cash pre-tax asset impairment

charges of $86 million, which included the write-off of a portion of the associated goodwill and intangible assets of $25 million and $55 million, respectively, as

well as $6 million of asset write-downs. In January 2007, the Company announced the sale of its hot cereal assets and trademarks. In anticipation of the sale, the

Company recorded a pre-tax asset impairment charge of $69 million in 2006 for these assets, which included the write-off of a portion of the associated goodwill

and intangible assets of $15 million and $52 million, respectively, as well as $2 million of asset write-downs. During the first quarter of 2005, the Company

completed its annual review of goodwill and intangible assets and no impairment charges resulted from this review. However, as part of the sale of certain

Canadian assets and two brands, the Company recorded non-cash pre-tax asset impairment charges of $269 million in 2005, which included impairment of

goodwill and intangible assets of $13 million and $118 million, respectively, as well as $138 million of asset write-downs.

Impairment of Long-Lived Assets. The Company reviews long-lived assets, including amortizable intangible assets, for impairment whenever events or

changes in business circumstances indicate that the carrying amount of the assets may not be fully recoverable. The Company performs undiscounted operating

cash flow analyses to determine if an impairment exists. These analyses are affected by interest rates, general economic conditions and projected growth rates.

For purposes of recognition and measurement of an impairment of assets held for use, the Company groups assets and liabilities at the lowest level for which

cash flows are separately identifiable. If an impairment is determined to exist, any related impairment loss is calculated based on fair value. Impairment losses on

assets to be disposed of, if any, are based on the estimated proceeds to be received, less costs of disposal. As previously discussed, the Company recorded

non-cash pre-tax asset impairment charges of $245 million related to itsTassimo hot beverage business in 2006. The charges are included in asset impairment and

exit costs in the consolidated statement of earnings.

Marketing and Advertising Costs. As required by U.S. GAAP, the Company records marketing costs as an expense in the year to which such costs relate.

The Company does not defer amounts on its year-end consolidated balance sheet with respect to marketing costs. The Company expenses advertising costs as

incurred. Consumer incentive and trade promotion activities are recorded as a reduction of revenues based on amounts estimated as being due to customers and

consumers at the end of a period, based principally on historical utilization and redemption rates. For interim reporting

28

Source: KRAFT FOODS INC, 10-K, March 01, 2007