Honeywell 2004 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2004 Honeywell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

|

|

HONEYWELL INTERNATIONAL INC.

NOTES TO FINANCIAL STATEMENTS—(Continued)

(Dollars in millions, except per share amounts)

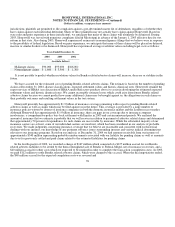

of cash expenditures depends on a number of factors, including the timing of litigation and settlements of remediation liability,

personal injury and property damage claims, regulatory approval of cleanup projects, remedial techniques to be utilized and

agreements with other parties.

Although we do not currently possess sufficient information to reasonably estimate the amounts of liabilities to be recorded upon

future completion of studies, litigation or settlements, and neither the timing nor the amount of the ultimate costs associated with

environmental matters can be determined, they could be material to our consolidated results of operations or operating cash flows in

the periods recognized or paid. However, considering our past experience and existing reserves, we do not expect that these

environmental matters will have a material adverse effect on our consolidated financial position.

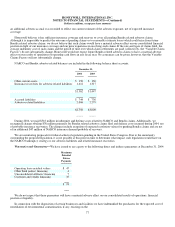

In the matter entitled Interfaith Community Organization, et al. v. Honeywell International Inc., et al., the United States District

Court for the District of New Jersey held in May 2003 that a predecessor Honeywell site located in Jersey City, New Jersey

constituted an imminent and substantial endangerment and ordered Honeywell to conduct the excavation and transport for offsite

disposal of approximately one million tons of chromium residue present at the site. Honeywell appealed the Court's decision to the

Third Circuit Court of Appeals (Appeals Court). As disclosed in prior SEC filings, we believed that the District Court-ordered remedy

would be remanded, reversed or replaced and, accordingly, provisions previously made in our financial statements for remedial costs

at this site did not assume excavation and offsite removal of chromium. On February 18, 2005, the Appeals Court denied Honeywell's

appeal. In light of the Appeals Court decision, we recorded a pre-tax charge of $278 million in the fourth quarter of 2004, which

reflects the incremental cost of implementing the Court-ordered remedy. Implementation of the excavation and offsite removal

remedy is expected to take place over a five-year period, and the cost of implementation is expected to be incurred evenly over that

period. We do not expect implementation of the remedy to have a material adverse effect on our future consolidated results of

operations, operating cash flows or financial position.

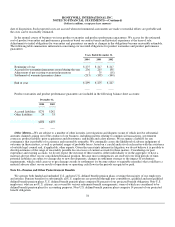

In accordance with a 1992 consent decree with the State of New York, Honeywell is studying environmental conditions in and

around Onondaga Lake (the Lake) in Syracuse, New York. The purpose of the study is to identify, evaluate and propose remedial

measures that can be taken to remedy historic industrial contamination in the Lake. A predecessor company to Honeywell operated a

chemical plant which is alleged to have contributed mercury and other contaminants to the Lake. In November 2004, the New York

State Department of Environmental Conservation (the DEC) issued its Proposed Plan for remediation of industrial contamination in

the Lake. There will be a public comment period until March 1, 2005, and the Proposed Plan is subject to review by the U.S.

Environmental Protection Agency. The DEC is currently expected to issue its Record of Decision in the first half of 2005.

The Proposed Plan calls for a combined dredging/capping remedy generally in line with the approach recommended in the

Feasibility Study submitted by Honeywell in May 2004 (the May 2004 Feasibility Study). Although the Proposed Plan calls for

additional remediation in certain parts of the Lake, it would not require the most extensive dredging alternatives described in the May

2004 Feasibility Study. The DEC's aggregate cost estimate is based on the high end of the range of potential costs for major elements

of the Proposed Plan and includes a contingency. The actual cost of the Proposed Plan will depend upon, among other things, the

resolution of certain technical issues during the design phase of the remediation, expected to occur sometime in 2007 and beyond.

Based on currently available information and analysis performed by our engineering consultants, our estimated cost of

implementing the remedy set forth in the Proposed Plan is consistent with amounts previously provided for in our financial statements.

Our estimating process considered a range of possible outcomes and amounts recorded reflect our best estimate at this time. We do not

believe that this matter will have a material adverse impact on our consolidated financial position.

72