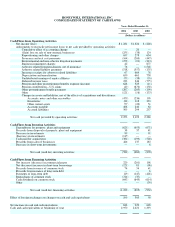

Honeywell 2004 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2004 Honeywell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

|

|

HONEYWELL INTERNATIONAL INC.

NOTES TO FINANCIAL STATEMENTS—(Continued)

(Dollars in millions, except per share amounts)

Prescription Drug, Improvement and Modernization Act of 2003 (the Act) for employers that sponsor postretirement health care plans

that provide prescription drug coverage that is at least actuarially equivalent to that offered by Medicare Part D. We have determined

that the enactment of the Act does not have a material impact on our accumulated postretirement benefit obligation and, therefore, is

not a “significant event” as defined in FSP No. 106-2 for our postretirement health care plans. Accordingly, as permitted, we adopted

FSP No. 106-2 on December 31, 2004 and such adoption did not have a material effect on our consolidated financial statements.

In December 2003, the FASB issued Statement of Financial Accounting Standards No. 132 (Revised 2003), “Employers'

Disclosures about Pensions and Other Postretirement Benefits, an amendment of FASB Statements No. 87, 88, and 106” (SFAS

No. 132-Revised 2003) which revises employers' disclosures about pension plans and other postretirement benefit plans. All

provisions of this statement are effective for the year ended December 31, 2004. See Note 22 for further information.

In January 2003, the FASB issued FIN 46, which provides guidance on consolidation of variable interest entities. In December

2003, the FASB deferred the effective date of FIN 46 for certain variable interest entities (i.e., non-special purpose entities) until the

first quarter of 2004. Our full adoption of the provisions of FIN 46 did not have a material effect on our consolidated financial

statements.

In November 2002, the FASB issued FASB Interpretation No. 45, “Guarantor's Accounting and Disclosure Requirements for

Guarantees, Including Indirect Guarantees of Indebtedness of Others” (FIN 45), which requires us to recognize a liability for the fair

value of an obligation assumed by issuing a guarantee. FIN 45 was effective for guarantees issued or modified on or after January 1,

2003. The adoption of FIN 45 did not have a material effect on our consolidated financial statements. See Note 21 for further

information.

In November 2002, the Emerging Issues Task Force (EITF) reached a consensus on EITF Issue No. 00-21, “Accounting for

Revenue Arrangements with Multiple Deliverables”. EITF Issue No. 00-21 provides guidance on when and how to separate elements

of an arrangement that may involve the delivery or performance of multiple products, services and rights to use assets into separate

units of accounting. The guidance in the consensus was effective for revenue arrangements entered into in fiscal periods beginning

after June 15, 2003. We adopted EITF Issue No. 00-21 prospectively in the quarter beginning July 1, 2003. The adoption of EITF

Issue No. 00-21 did not have a material effect on our consolidated financial statements.

In June 2002, the FASB issued Statement of Financial Accounting Standards No. 146, “Accounting for Costs Associated with Exit

or Disposal Activities” (SFAS No. 146), the provisions of which were effective for any exit or disposal activities initiated by us after

December 31, 2002. SFAS No. 146 provides guidance on the recognition and measurement of liabilities associated with exit or

disposal activities and requires that such liabilities be recognized when incurred. The adoption of the provisions of SFAS No. 146

impacted the measurement and timing of costs associated with any exit or disposal activities initiated after December 31, 2002.

In June 2001, the FASB issued Statement of Financial Accounting Standards No. 143, “Accounting for Asset Retirement

Obligations” (SFAS No. 143) which requires recognition of the fair value of obligations associated with the retirement of tangible

long-lived assets when there is a legal obligation to incur such costs. Upon initial recognition of a liability the cost is capitalized as

part of the related long-lived asset and depreciated over the corresponding asset's useful life. SFAS No. 143 primarily impacts our

accounting for costs associated with the future retirement of nuclear fuel conversion facilities in our Specialty Materials reportable

segment. Upon adoption on January 1, 2003, we recorded an increase in property, plant and equipment, net of $16 million and

recognized an asset retirement obligation of $47 million. This resulted in the recognition of a non-cash charge of $31 million ($20

million after-tax, or $0.02 per share) that was reported as a cumulative effect of an accounting

52