Holiday Inn 2005 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2005 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

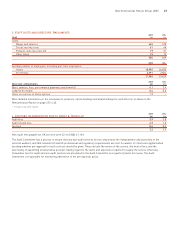

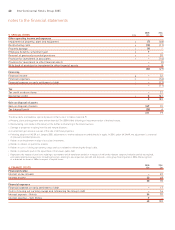

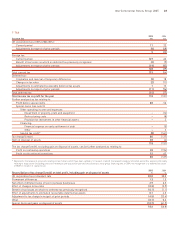

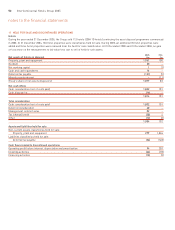

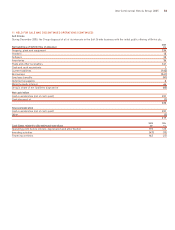

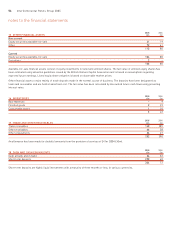

3 STAFF COSTS AND DIRECTORS’ EMOLUMENTS

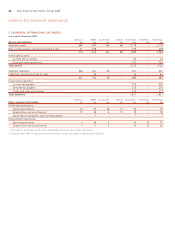

2005 2004

Staff £m £m

Costs:

Wages and salaries 465 570

Social security costs 61 66

Pension costs (see note 23) 19 21

Other plans 15 12

560 669

2005 2004

Average number of employees, including part-time employees:

Hotels 18,995 26,835

Soft Drinks 2,991 2,824

21,986 29,659

2005 2004

Directors’ emoluments £m £m

Basic salaries, fees, performance payments and benefits* 4.1 3.4

Long-term reward 0.4 0.6

Gains on exercise of share options 1.7 –

More detailed information on the emoluments, pensions, option holdings and shareholdings for each Director is shown in the

Remuneration Report on pages 25 to 33.

* Includes long-term reward.

2005 2004

4 AUDITORS’ REMUNERATION PAID TO ERNST & YOUNG LLP £m £m

Audit fees 3.9 3.8

Audit related fees 2.7 1.6

Tax fees 0.6 0.5

7.2 5.9

Non-audit fees payable for UK services were £2.1m (2004 £1.1m).

The Audit Committee has a process to ensure that any non-audit services do not compromise the independence and objectivity of the

external auditors, and that relevant UK and US professional and regulatory requirements are met. A number of criteria are applied when

deciding whether pre-approval for such services should be given. These include the nature of the service, the level of fees, and the

practicality of appointing an alternative provider, having regard to the skills and experience required to supply the service effectively.

Cumulative fees for audit and non-audit services are presented to the Audit Committee on a quarterly basis for review. The Audit

Committee is responsible for monitoring adherence to the pre-approval policy.

InterContinental Hotels Group 2005 47