Cisco 2006 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2006 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79

|

|

72 Cisco Systems, Inc.

Accuracy of Fair Value Estimates The Company uses third-party analyses to assist in developing the assumptions used in, as well as

calibrating, its lattice-binomial model. The Company is responsible for determining the assumptions used in estimating the fair value of its

share-based payment awards.

The Company’s determination of fair value of share-based payment awards on the date of grant using an option-pricing model is

affected by the Company’s stock price as well as assumptions regarding a number of highly complex and subjective variables. These

variables include, but are not limited to the Company’s expected stock price volatility over the term of the awards, and actual and projected

employee stock option exercise behaviors. Option-pricing models were developed for use in estimating the value of traded options that have

no vesting or hedging restrictions and are fully transferable. Because the Company’s employee stock options have certain characteristics

that are signicantly different from traded options, and because changes in the subjective assumptions can materially affect the estimated

value, in management’s opinion, the existing valuation models may not provide an accurate measure of the fair value of the Company’s

employee stock options. Although the fair value of employee stock options is determined in accordance with SFAS 123(R) and SAB 107

using an option-pricing model, that value may not be indicative of the fair value observed in a willing buyer/willing seller market transaction.

Employee 401(k) Plans

The Company sponsors the Cisco Systems, Inc. 401(k) Plan (the “Plan”) to provide retirement benets for its employees. As allowed under

Section 401(k) of the Internal Revenue Code, the Plan provides tax-deferred salary contributions for eligible employees. The Plan allows

employees to contribute from 1% to 25% of their annual compensation to the Plan on a pretax and after-tax basis. Employee contributions

are limited to a maximum annual amount as set periodically by the Internal Revenue Code. The Company matches pretax employee

contributions up to 50% of the rst 6% of eligible earnings that are contributed by employees. Therefore, the maximum matching contribution

that the Company may allocate to each participant’s account will not exceed $6,600 for the 2006 calendar year due to the $220,000 annual

limit on eligible earnings imposed by the Internal Revenue Code. All matching contributions vest immediately. The Company’s matching

contributions to the Plan totaled $96 million, $84 million, and $81 million in scal 2006, 2005, and 2004, respectively.

The Plan allows employees who meet the age requirements and reach the Plan contribution limits to make a catch-up contribution not

to exceed the lesser of 50% of their eligible compensation or the limit set forth in the Internal Revenue Code. The catch-up contributions

are not eligible for matching contributions. In addition, the Plan provides for discretionary prot-sharing contributions as determined by the

Board of Directors. Such contributions to the Plan are allocated among eligible participants in the proportion of their salaries to the total

salaries of all participants. There were no discretionary prot-sharing contributions made in scal 2006, 2005, or 2004.

The Company also has other 401(k) plans that it sponsors. These plans arose from acquisitions of other companies and the Company’s

contributions to these plans were not material to the Company on either an individual or aggregate basis for any of the scal years presented.

Defined Benefit and Deferred Compensation Plans Assumed from Scientific-Atlanta

Upon completion of the acquisition of Scientic-Atlanta, the Company assumed certain dened benet plans related to employee pensions

and other post-employment benets. Scientic-Atlanta had a dened benet pension plan covering substantially all of its domestic employees

and dened benet pension plans covering certain international employees (collectively, the “Pension Plans”); a restoration retirement plan

for certain domestic employees (the “Restoration Plan”); supplemental executive retirement plans for certain key ofcers (“SERPs”); and

subsidized health care and life insurance benets for eligible retirees (“Retiree Medical and Life Plans”). The fair value of the liabilities of

these plans was determined at the July 29, 2006 measurement date. The fair value determination of the liabilities reects the Company’s

intent to integrate the Scientic-Atlanta employee benet programs with those of the Company. As a result, no additional benets will be

accrued under the Pension Plans, the Restoration Plan, and the SERPs after February 2008.

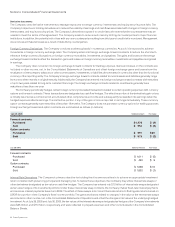

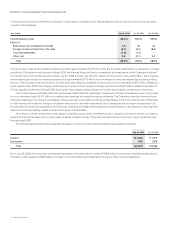

The following table sets forth projected benet obligations, plan assets, and amounts recorded in other long-term liabilities as of

July 29, 2006, using July 29, 2006 as a measurement date for all actuarial calculations of asset and liability values and signicant actuarial

assumptions (in millions):

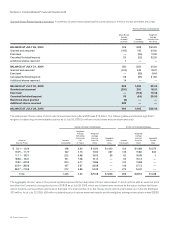

Pension Plans

Restoration

Plan SERPs Total

Projected benefit obligations $ 146 $ 9 $ 59 $ 214

Fair value of plan assets ( 95) — — (95)

Accrued benefit liability $ 51 $ 9 $ 59 $ 119

Notes to Consolidated Financial Statements