Cisco 2006 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2006 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

|

|

2006 Annual Report 37

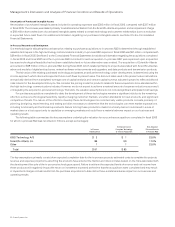

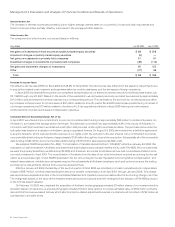

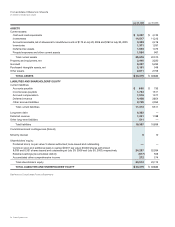

Deferred Revenue The following table presents the breakdown of deferred revenue (in millions):

July 30, 2005

Increase

(Decrease)July 29, 2006

Service $ 4,088 $ 3,618 $ 470

Product 1,561 1,424 137

Total $ 5,649 $ 5,042 $ 607

Reported as:

Current $ 4,408 $ 3,854 $ 554

Noncurrent 1,241 1,188 53

Total $ 5,649 $ 5,042 $ 607

The increase in deferred service revenue reects the impact of the increase in the volume of technical support contract initiations and

renewals, partially offset by the ongoing amortization of deferred service revenue. The increase in deferred product revenue was related

primarily to the timing of cash receipts related to unrecognized revenue from two-tier distributors.

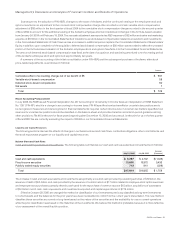

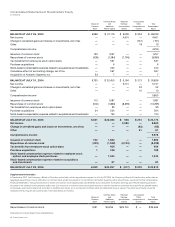

Long-Term Debt The following table summarizes our long-term debt as of July 29, 2006 (in millions, except percentages):

Amount Effective Rate(1)

Senior notes:

2009 Notes $ 500 5.27%

2011 Notes 3,000 5.39%

2016 Notes 3,000 5.62%

Total senior notes 6,500

Other notes 5

Unamortized discount (18)

Fair value adjustment (155)

Total $ 6,332

(1) The effective rates for the 2011 Notes and the 2016 Notes reect the variable rate in effect as of July 29, 2006 on the interest rate swaps designated as fair value

hedges of those notes, including the amortization of the discount.

In February 2006, we issued $500 million of senior oating interest rate notes due 2009 (the “2009 Notes”), $3.0 billion of 5.25% senior notes

due 2011 (the “2011 Notes”) and $3.0 billion of 5.50% senior notes due 2016 (the “2016 Notes”), for an aggregate principal amount of $6.5

billion. The debt issuance was used to fund the acquisition of Scientic-Atlanta and for general corporate purposes. The 2011 Notes and

the 2016 Notes are redeemable by us at any time, subject to a make-whole premium. To achieve our interest rate objectives, we entered into

$6.0 billion notional amount of interest rate swaps. In effect, these swaps convert the xed interest rates of the 2011 Notes and the 2016

Notes to oating interest rates based on LIBOR. Gains and losses in the fair value of the interest rate swaps offset changes in the fair value of

the underlying debt. See Note 8 to the Consolidated Financial Statements. We were in compliance with all debt covenants as of July 29, 2006.

Contractual Obligations

Our cash ows from operations are dependent on a number of factors, including uctuations in our operating results, shipment linearity,

accounts receivable collections, inventory management, excess tax benets from stock-based compensation, and the timing and amount

of tax and other payments. As a result, the impact of contractual obligations on our liquidity and capital resources in future periods should

be analyzed in conjunction with such factors. In addition, we plan for and measure our liquidity and capital resources through an annual

budgeting process.

Management’s Discussion and Analysis of Financial Condition and Results of Operations