Cisco 2006 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2006 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

|

|

2006 Annual Report 21

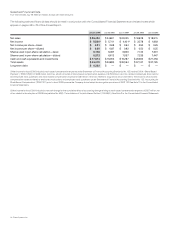

Contracts, Internet commerce agreements, and customer purchase orders are generally used to determine the existence of an

arrangement. Shipping documents and customer acceptance, when applicable, are used to verify delivery. We assess whether the fee is

xed or determinable based on the payment terms associated with the transaction and whether the sales price is subject to refund or

adjustment. We assess collectibility based primarily on the creditworthiness of the customer as determined by credit checks and analysis,

as well as the customer’s payment history. When a sale involves multiple elements, such as sales of products that include services, the entire

fee from the arrangement is allocated to each respective element based on its relative fair value and recognized when revenue recognition

criteria for each element are met. The amount of product and service revenue recognized is impacted by our judgment as to whether an

arrangement includes multiple elements and, if so, whether vendor-specic objective evidence of fair value exists. Changes to the elements

in an arrangement and our ability to establish vendor-specic objective evidence for those elements could affect the timing of the revenue

recognition. Our total deferred revenue for products was $1.6 billion and $1.4 billion as of July 29, 2006 and July 30, 2005, respectively.

Technical support services revenue is deferred and recognized ratably over the period during which the services are to be performed,

which is typically from one to three years. Advanced services revenue is recognized upon delivery or completion of performance. Our total

deferred revenue for services was $4.1 billion and $3.6 billion as of July 29, 2006 and July 30, 2005, respectively.

We make sales to distributors and retail partners and recognize revenue based on a sell-through method using information provided

by them. Our distributors and retail partners participate in various cooperative marketing and other programs, and we maintain estimated

accruals and allowances for these programs. If actual credits received by our distributors and retail partners for these programs were to

deviate signicantly from our estimates, which are based on historical experience, our revenue could be adversely affected.

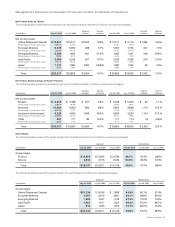

Allowance for Doubtful Accounts and Sales Returns

Our accounts receivable balance, net of allowance for doubtful accounts, was $3.3 billion and $2.2 billion as of July 29, 2006 and July 30, 2005,

respectively. The allowance for doubtful accounts was $175 million, or 5.0% of the gross accounts receivable balance, as of July 29, 2006

and $162 million, or 6.8% of the gross accounts receivable balance, as of July 30, 2005. The allowance is based on our assessment of the

collectibility of customer accounts. We regularly review the allowance by considering factors such as historical experience, credit quality,

age of the accounts receivable balances, and current economic conditions that may affect a customer’s ability to pay.

Our provision for doubtful accounts was $24 million for scal 2006. We had no provision for doubtful accounts in scal 2005 and our

provision for doubtful accounts was $19 million in scal 2004. If a major customer’s creditworthiness deteriorates, or if actual defaults are

higher than our historical experience, or if other circumstances arise, our estimates of the recoverability of amounts due to us could be

overstated, and additional allowances could be required, which could have an adverse impact on our revenue.

A reserve for future sales returns is established based on historical trends in product return rates. The reserve for future sales returns as

of July 29, 2006 and July 30, 2005 was $80 million and $63 million, respectively, and was recorded as a reduction of our accounts receivable.

If the actual future returns were to deviate from the historical data on which the reserve had been established, our revenue could be

adversely affected.

Allowance for Inventory and Liability for Purchase Commitments with Contract Manufacturers and Suppliers

Our inventory balance was $1.4 billion and $1.3 billion as of July 29, 2006 and July 30, 2005, respectively. Our inventory allowance was

$152 million and $159 million as of July 29, 2006 and July 30, 2005, respectively. We provide allowances for inventory based on excess and

obsolete inventories determined primarily by future demand forecasts. The allowance is measured as the difference between the cost of

the inventory and market based upon assumptions about future demand and is charged to the provision for inventory, which is a component

of our cost of sales. At the point of the loss recognition, a new, lower-cost basis for that inventory is established, and subsequent changes

in facts and circumstances do not result in the restoration or increase in that newly established cost basis.

Our provision for inventory was $162 million, $221 million, and $205 million for scal 2006, 2005, and 2004, respectively. If there were to

be a sudden and signicant decrease in demand for our products, or if there were a higher incidence of inventory obsolescence because

of rapidly changing technology and customer requirements, we could be required to increase our inventory allowances, and our gross margin

could be adversely affected. In the third quarter of scal 2006, we began the initial implementation of the lean manufacturing model.

Inventory management remains an area of focus as we balance the need to maintain strategic inventory levels to ensure competitive lead

times with the risk of inventory obsolescence.

In addition, we record a liability for rm, noncancelable, and unconditional purchase commitments with contract manufacturers and

suppliers for quantities in excess of our future demand forecasts consistent with our allowance for inventory. As of July 29, 2006, the liability for

these purchase commitments was $148 million, compared with $87 million as of July 30, 2005, and was included in other accrued liabilities.

Management’s Discussion and Analysis of Financial Condition and Results of Operations