Cisco 2006 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2006 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

|

|

42 Cisco Systems, Inc.

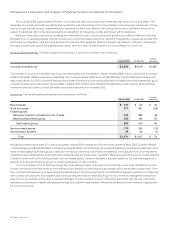

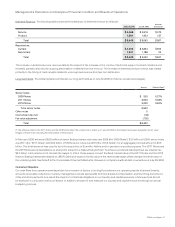

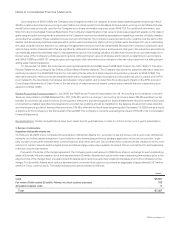

Foreign exchange forward and option contracts as of July 29, 2006 and July 30, 2005 are summarized as follows (in millions):

Notional Amount Fair ValueJuly 29, 2006

Forward contracts:

Purchased $ 1,376 $ (2)

Sold $ 554 $ (3)

Option contracts:

Purchased $ 591 $ 20

Sold $ 573 $ (2)

July 30, 2005 Notional Amount Fair Value

Forward contracts:

Purchased $ 1,011 $ (5)

Sold $ 450 $ 9

Option contracts:

Purchased $ 1,028 $ 10

Sold $ 1,002 $ (7)

Our foreign exchange forward contracts related to current assets and liabilities generally range from one to three months in original

maturity. Additionally, we have entered into foreign exchange forward contracts related to long-term customer nancings with maturities of

up to two years. The foreign exchange forward contracts related to investments generally have maturities of less than one year. Currency

option contracts generally have maturities of less than 18 months. We do not enter into foreign exchange forward and option contracts for

trading purposes. We do not expect gains or losses on these derivative instruments to have a material impact on our nancial results. See

Note 8 to the Consolidated Financial Statements.

Interest Rate Derivatives

Our primary objective for holding xed income securities is to achieve an appropriate investment return consistent with preserving principal

and managing risk. To realize these objectives, we may utilize interest rate swaps or other derivatives designated as fair value or cash ow

hedges. We have entered into $1.0 billion of interest rate swaps designated as fair value hedges of our investment portfolio. Under these

interest rate swap contracts, we make xed-rate interest payments and receive interest payments based on LIBOR. The effect of these swaps

is to convert xed-rate returns to oating-rate returns based on LIBOR for a portion of our xed income portfolio. The gains and losses related

to changes in the value of the interest rate swaps are included in other income, net, in the Consolidated Statements of Operations and

offset the changes in fair value of the underlying hedged investment. As of July 29, 2006 and July 30, 2005, the fair values of the interest

rate swaps designated as hedges of our investments were $45 million and $15 million, respectively, and were reected in prepaid expenses

and other current assets in the Consolidated Balance Sheets.

In conjunction with our issuance of xed-rate senior notes in February 2006, we entered into $6.0 billion of interest rate swaps designated

as fair value hedges of our xed-rate debt. Under these interest rate swap contracts, we receive xed-rate interest payments and make

interest payments based on LIBOR. The effect of these swaps is to convert xed-rate interest expense to oating-rate interest expense

based on LIBOR. The gains and losses related to changes in the value of the interest rate swaps are included in other income, net, in the

Consolidated Statements of Operations and offset the changes in fair value of the underlying debt. As of July 29, 2006, the fair value of the

interest rate swaps designated as hedges of our debt was $155 million and was reected in other long-term liabilities in the Consolidated

Balance Sheets.

Equity Derivatives

We maintain a portfolio of publicly traded equity securities which are subject to price risk. We may hold equity securities for strategic

purposes or to diversify our overall investment portfolio. To manage our exposure to changes in the fair value of certain equity securities, we

may, from time to time, enter into equity derivative contracts. As of July 29,2006, we have entered into forward sale and option agreements on

certain publicly traded equity securities designated as fair value hedges. The gains and losses due to changes in the value of the hedging

instruments are included in other income, net, in the Consolidated Statements of Operations and offset the change in the fair value of the

underlying hedged investment. As of July 29, 2006, the notional and fair value amounts of the derivatives were $164 million and $93 million,

respectively. As of July 30, 2005, the notional and fair value amounts of the derivatives were $198 million and $19 million, respectively.

Quantitative and Qualitative Disclosures About Market Risk