Cigna 2011 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2011 Cigna annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

58 CIGNA CORPORATION2011 Form10K

PART II

ITEM 7 Management’s Discussion and Analysis of Financial Condition and Results of Operations

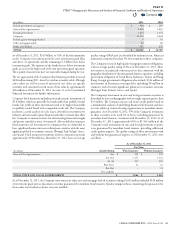

Uses of Capital

Acquisitions

In 2011, the Company paid approximately $115million to acquire

FirstAssist, and in 2010, the Company acquired Vanbreda International

for $412million. e acquisitions were funded from available cash.

See Note3 for further information.

Pension funding

e Company contributed $250million to its domestic qualied

pension plans in 2011, $212million in 2010 and $410million in 2009.

Share repurchase

In 2011 the Company repurchased 5.3million shares for approximately

$225million. e total remaining share repurchase authorization as

of February23,2012 was $522million. e Company repurchased

6.2million shares for $201million during 2010, and did not repurchase

any shares in 2009.

Arbor funding

e Company deployed $150million of capital to its subsidiary, Cigna

Arbor Life Insurance Company (“Arbor”) in support of an internal

reinsurance transaction related to the GMDB and GMIB businesses.

See page51 of this MD&A under “Run-o Operations” for additional

discussion of this matter.

Repayments of long-term debt

In 2011, the Company repaid $449million in maturing long-term debt.

In December2010, the Company settled approximately $270million

of outstanding debt (8.5% Notesand 6.35% Notes) through a tender

oer process. See Note15 to the Consolidated Financial Statements

for additional information.

Liquidity and Capital Resources Outlook

At December31,2011, there was approximately $3.8billion in cash

and short-term investments available at the parent company level. In

2012, the parent company’s cash obligations are expected to consist

of the following:

•Acquisition of HealthSpring for approximately $3.8billion;

•

scheduled interest payments of $246million on outstanding long-

term debt of $5.0billion at December31,2011;

•

contributions to the domestic qualied pension plan of $250million;

and

•approximately $100million of commercial paper outstanding as of

December 31, 2011. e Company expects to have approximately

$225 million outstanding as of March 31, 2012.

Based on cash on hand, current projections for dividends from the

Company’s subsidiaries, as well as its ability to issue additional commercial

paper, debt or equity securities in the capital markets, the Company

expects to have sucient liquidity to meet its obligations.

However, the Company’s cash projections may not be realized and the

demand for funds could exceed available cash if:

•ongoing businesses experience unexpected shortfalls in earnings;

•

regulatory restrictions or rating agency capital guidelines reduce the

amount of dividends available to be distributed to the parent company

from the insurance and HMO subsidiaries (including the impact

of equity market deterioration and volatility on subsidiary capital);

•

signicant disruption or volatility in the capital and credit markets

reduces the Company’s ability to raise capital or creates unexpected

losses related to the GMDB and GMIB businesses;

•

a substantial increase in funding over current projections is required

for the Company’s pension plan; or

•

a substantial increase in funding is required for the Company’s GMDB

and GMIB equity and interest rate hedge programs.

In those cases, the Company expects to have the exibility to satisfy

liquidity needs through a variety of measures, including intercompany

borrowings and sales of liquid investments. e parent company may

borrow up to $600million from CGLIC without prior state approval.

In addition, the Company may use short-term borrowings, such as the

commercial paper program and the committed line of credit agreement

of up to $1.5billion subject to the maximum debt leverage covenant in

its line of credit agreement. As of December31,2011, the Company had

$1.4billion of borrowing capacity under the credit agreement, reecting

$118million of letters of credit issued as of December31,2011. Within

the maximum debt leverage covenant in the line of credit agreement,

the Company has approximately $4billion of additional borrowing

capacity in addition to the $5.1billion of debt outstanding.

ough the Company believes it has adequate sources of liquidity,

signicant disruption or volatility in the capital and credit markets

could aect the Company’s ability to access those markets for additional

borrowings or increase costs associated with borrowing funds.

Solvency regulation

Many states have adopted some form of the National Association of

Insurance Commissioners (“NAIC”) model solvency-related laws and

risk-based capital rules (“RBC rules”) for life and health insurance

companies. e RBC rules recommend a minimum level of capital

depending on the types and quality of investments held, the types of

business written and the types of liabilities incurred. If the ratio of the

insurer’s adjusted surplus to its risk-based capital falls below statutory

required minimums, the insurer could be subject to regulatory actions

ranging from increased scrutiny to conservatorship.

In addition, various non-U.S. jurisdictions prescribe minimum surplus

requirements that are based upon solvency, liquidity and reserve coverage

measures. During 2011, the Company’s HMOs and life and health

insurance subsidiaries, as well as non-U.S. insurance subsidiaries, were

compliant with applicable RBC and non-U.S. surplus rules.

Unfunded Pension Plan Liability

As of December31,2011, the unfunded pension liability was $1.8billion,

an increase from December31,2010, reecting a decline in discount rates

of 100basis points, and lower than expected asset returns, partially oset

by pension contributions of $250million in 2011. Pension contributions

in 2012 under the Pension Protection Act of 2006 are not expected to

Contents

Q