Cigna 2011 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2011 Cigna annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

82 CIGNA CORPORATION2011 Form10K

PART II

ITEM 8 Financial Statements and Supplementary Data

in eect, accrues to the Company and directly impacts shareholders’

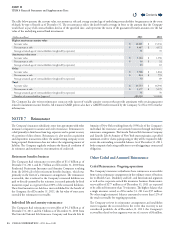

net income. An account is in decit when the accumulated medical

costs and administrative charges, including prot charges, exceed the

accumulated premium received. Adjustments to medical claims payable

on accounts in surplus accrue directly to the policyholder with no impact

on the Company’s shareholders’ net income. An account is in surplus

when the accumulated premium received exceeds the accumulated

medical costs and administrative charges, including prot charges.

NOTE 6 Guaranteed Minimum Death Benefit Contracts

e Company’s reinsurance operations, which were discontinued in

2000 and are now an inactive business in run-o mode, reinsured a

guaranteed minimum death benet (“GMDB”), also known as variable

annuity death benets (“VADBe”), under certain variable annuities

issued by other insurance companies. ese variable annuities are

essentially investments in mutual funds combined with a death benet.

e Company has equity and other market exposures as a result of this

product. In periods of declining equity markets and in periods of at

equity markets following a decline, the Company’s liabilities for these

guaranteed minimum death benets increase. Conversely, in periods

of rising equity markets, the Company’s liabilities for these guaranteed

minimum death benets decrease.

In 2000, the Company determined that the GMDB reinsurance

business was premium decient because the recorded future policy

benet reserve was less than the expected present value of future claims

and expenses less the expected present value of future premiums and

investment income using revised assumptions based on actual and

expected experience. e Company tests for premium deciency by

reviewing its reserve each quarter using current market conditions and

its long-term assumptions. Under premium deciency accounting,

if the recorded reserve is determined insucient, an increase to the

reserve is reected as a charge to current period income. Consistent with

GAAP, the Company does not recognize gains on premium decient

long duration products.

See Note12 for further information on the Company’s dynamic

hedge programs that are used to reduce certain equity and interest

rate exposures associated with this business.

e Company had future policy benet reserves for GMDB contracts

of $1.2billion as of December31,2011, and $1.1billion as of

December31,2010. e determination of liabilities for GMDB requires

the Company to make critical accounting estimates. e Company

estimates its liabilities for GMDB exposures using an internal model

run using many scenarios and based on assumptions regarding lapse,

future partial surrenders, claim mortality (deaths that result in claims),

interest rates (mean investment performance and discount rate) and

volatility. Lapse refers to the full surrender of an annuity prior to a

contractholder’s death. Future partial surrender refers to the fact that

most contractholders have the ability to withdraw substantially all of

their mutual fund investments while retaining the death benet coverage

in eect at the time of the withdrawal. Mean investment performance

for underlying equity mutual funds refers to market rates expected

to be earned on the hedging instruments over the life of the GMDB

equity hedge program, and for underlying xed income mutual funds

refers to the expected market return over the life of the contracts.

Market volatility refers to market uctuation. ese assumptions are

based on the Company’s experience and future expectations over the

long-term period, consistent with the long-term nature of this product.

e Company regularly evaluates these assumptions and changes its

estimates if actual experience or other evidence suggests that assumptions

should be revised. If actual experience diers from the assumptions

(including lapse, future partial surrenders, claim mortality, interest

rates and volatility) used in estimating these liabilities, the result could

have a material adverse eect on the Company’s consolidated results

of operations, and in certain situations, could have a material adverse

eect on the Company’s nancial condition.

e following provides information about the Company’s reserving

methodology and assumptions for GMDB as of December31,2011:

•

e reserves represent estimates of the present value of net amounts

expected to be paid, less the present value of net future premiums.

Included in net amounts expected to be paid is the excess of the

guaranteed death benets over the values of the contractholders’ accounts

(based on underlying equity and bond mutual fund investments).

•

e reserves include an estimate for partial surrenders that essentially

lock in the death benet for a particular policy based on annual election

rates that vary from 0% to 15% depending on the net amount at risk

for each policy and whether surrender charges apply.

•

e assumed mean investment performance (“growth interest rate”)

for the underlying equity mutual funds for the portion of the liability

that is covered by the Company’s growth interest rate hedge program

is based on the market-observable LIBOR swap curve. e assumed

mean investment performance for the remainder of the underlying

equity mutual funds considers the Company’s GMDB equity hedge

program using futures contracts, and is based on the Company’s view

that short-term interest rates will average 4.75% over future periods,

but considers that current short-term rates are less than 4.75%.

e mean investment performance assumption for the underlying

xed income mutual funds (bonds and money market) is 5% based

on a review of historical returns. e investment performance for

underlying equity and xed income mutual funds is reduced by fund

fees ranging from 1% to 3% across all funds.

•

e volatility assumption is based on a review of historical monthly

returns for each key index (e.g. S&P500) over a period of at least

ten years. Volatility represents the dispersion of historical returns

compared to the average historical return (standard deviation) for

each index. e assumption is 16% to 25%, varying by equity fund

type; 4% to 10%, varying by bond fund type; and 2% for money

market funds. ese volatility assumptions are used along with the

mean investment performance assumption to project future return

scenarios.

•

e discount rate is 5.75%, which is determined based on the

underlying and projected yield of the portfolio of assets supporting

the GMDB liability.

•e claim mortality assumption is 65% to 89% of the 1994 Group

Annuity Mortality table, with 1% annual improvement beginning

January1,2000. e assumption reects that for certain contracts,

a spousal beneciary is allowed to elect to continue a contract by

becoming its new owner, thereby postponing the death claim rather

than receiving the death benet currently. For certain issuers of these

Contents

Q