Cigna 2011 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2011 Cigna annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

95CIGNA CORPORATION2011 Form10K

PART II

ITEM 8 Financial Statements and Supplementary Data

volatility ranges from 16% to 36% for equity funds, 4% to 12% for

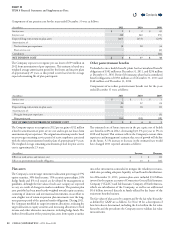

bond funds, and 1% to 2% for money market funds.

•

e mortality assumption is 70% of the 1994 Group Annuity Mortality

table, with 1% annual improvement beginning January1,2000.

•

e annual lapse rate assumption reects experience that diers by

the company issuing the underlying variable annuity contracts, ranges

from 1% to 12% at December31,2011, and depends on the time

since contract issue and the relative value of the guarantee.

•

e annual annuity election rate assumption reects experience

that diers by the company issuing the underlying variable annuity

contracts and depends on the annuitant’s age, the relative value

of the guarantee and whether a contractholder has had a previous

opportunity to elect the benet. Immediately after the expiration

of the waiting period, the assumed probability that an individual

will annuitize their variable annuity contract is up to 80%. For the

second and subsequent annual opportunities to elect the benet,

the assumed probability of election is up to 35%. Actual data is still

emerging for the Company as well as the industry and the estimates

are based on this limited data.

•

e nonperformance risk adjustment is incorporated by adding an

additional spread to the discount rate in the calculation of both(1)

the GMIB liability to reect a hypothetical market participant’s

view of the risk of the Company not fullling its GMIB obligations,

and(2) the GMIB asset to reect a hypothetical market participant’s

view of the reinsurers’ credit risk, after considering collateral. e

estimated market-implied spread is company-specic for each party

involved to the extent that company-specic market data is available

and is based on industry averages for similarly-rated companies when

company-specic data is not available. e spread is impacted by

the credit default swap spreads of the specic parent companies,

adjusted to reect subsidiaries’ credit ratings relative to their parent

company and any available collateral. e additional spread over

LIBOR incorporated into the discount rate ranged from 20 to 160

basis points for the GMIB liability and from 50 to 125 basis points

for the GMIB reinsurance asset for that portion of the interest rate

curve most relevant to these policies.

•

e risk and prot charge assumption is based on the Company’s

estimate of the capital and return on capital that would be required

by a hypothetical market participant.

e Company regularly evaluates each of the assumptions used in

establishing these assets and liabilities by considering how a hypothetical

market participant would set assumptions at each valuation date. Capital

markets assumptions are expected to change at each valuation date

reecting currently observable market conditions. Other assumptions

may also change based on a hypothetical market participant’s view of

actual experience as it emerges over time or other factors that impact the

net liability. If the emergence of future experience or future assumptions

diers from the assumptions used in estimating these assets and liabilities,

the resulting impact could be material to the Company’s consolidated

results of operations, and in certain situations, could be material to

the Company’s nancial condition.

GMIB liabilities are reported in the Company’s Consolidated Balance

Sheets in Accounts payable, accrued expenses and other liabilities.

GMIB assets associated with these contracts represent net receivables

in connection with reinsurance that the Company has purchased from

two external reinsurers and are reported in the Company’s Consolidated

Balance Sheets in Other assets, including other intangibles.

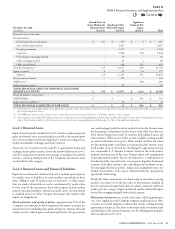

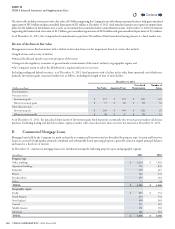

Changes in Level 3 Financial Assets and Financial

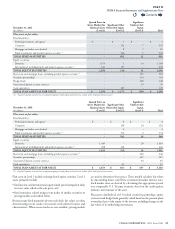

Liabilities Carried at Fair Value

The following tables summarize the changes in financial assets

and nancial liabilities classied in Level3 for the years ended

December31,2011 and 2010. ese tables exclude separate account assets

as changes in fair values of these assets accrue directly to policyholders.

Gains and losses reported in this table may include changes in fair

value that are attributable to both observable and unobservable inputs.

(In millions)

Fixed

Maturities&

Equity Securities GMIB Assets GMIB Liabilities GMIB Net

Balance at January1,2011 $ 933 $ 480 $ (903) $ (423)

Gains (losses) included in income:

GMIB fair value gain/(loss) - 270 (504) (234)

Other 10 - - -

Total gains (losses) included in shareholders’ net income 10 270 (504) (234)

Gains included in other comprehensive income 7 - - -

Gains required to adjust future policy benets for settlement annuities(1) 41 - - -

Purchases, issuances, settlements:

Purchases 129 - - -

Sales (20) - - -

Settlements (61) (38) 74 36

Total purchases, sales and settlements 48 (38) 74 36

Transfers into/(out of) Level3:

Transfers into Level3 81 - - -

Transfers out of Level3 (118) - - -

Total transfers into/(out of) Level3 (37) - - -

Balance at December31,2011 $ 1,002 $ 712 $ (1,333) $ (621)

Total gains (losses) included in shareholders’ net income attributable

toinstruments held at the reporting date $ 6 $ 270 $ (504) $ (234)

(1) Amounts do not accrue to shareholders.

Contents

Q