CarMax 2011 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2011 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

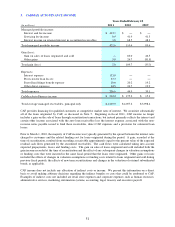

56

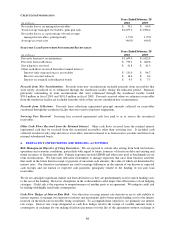

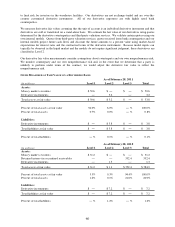

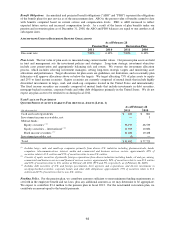

CREDIT LOSS INFORMATION

(In millions)

Net credit losses on managed receivables 70.1$ 69.8$

Total average managed receivables, principal only 4,057.2$ 3,998.4$

Net credit losses as a percentage of total average

managed receivables, principal only 1.73% 1.75%

Average recovery rate 49.8% 44.0%

Years Ended February 28

2010

2009

SELECTED CASH FLOWS FROM SECURITIZED RECEIVABLES

(In millions)

Proceeds from new securitizations 1,647.0$ 1,622.8$

Proceeds from collections 779.2$ 840.6$

Servicing fees received 41.8$ 41.3$

Other cash flows received from the retained interest:

Interest-only strip and excess receivables 131.0$ 96.7$

Reserve account releases 16.6$ 6.4$

Interest on retained subordinated bonds 9.5$ 7.5$

Years Ended February 28

2010

2009

Proceeds from New Securitizations. Proceeds from new securitizations included proceeds from receivables that

were newly securitized in or refinanced through the warehouse facility during the indicated period. Balances

previously outstanding in term securitizations that were refinanced through the warehouse facility totaled

$76.0 million in fiscal 2010 and $101.0 million in fiscal 2009. Proceeds received when we refinance receivables

from the warehouse facility are excluded from this table as they are not considered new securitizations.

Proceeds from Collections. Proceeds from collections represented principal amounts collected on receivables

securitized through the warehouse facility that were used to fund new originations.

Servicing Fees Received. Servicing fees received represented cash fees paid to us to service the securitized

receivables.

Other Cash Flows Received from the Retained Interest. Other cash flows received from the retained interest

represented cash that we received from the securitized receivables other than servicing fees. It included cash

collected on interest-only strip and excess receivables, amounts released to us from reserve accounts and interest on

retained subordinated bonds.

6. DERIVATIVE INSTRUMENTS AND HEDGING ACTIVITIES

Risk Management Objective of Using Derivatives. We are exposed to certain risks arising from both our business

operations and economic conditions, particularly with regard to future issuances of fixed-rate debt and existing and

future issuances of floating-rate debt. Primary exposures include LIBOR and other rates used as benchmarks in our

term securitizations. We enter into derivative instruments to manage exposures that arise from business activities

that result in the future known receipt or payment of uncertain cash amounts, the value of which are determined by

interest rates. Our derivative instruments are used to manage differences in the amount of our known or expected

cash receipts and our known or expected cash payments principally related to the funding of our auto loan

receivables.

We do not anticipate significant market risk from derivatives as they are predominantly used to match funding costs

to the use of the funding. However, disruptions in the credit markets could impact the effectiveness of our hedging

strategies. Credit risk is the exposure to nonperformance of another party to an agreement. We mitigate credit risk

by dealing with highly rated bank counterparties.

Cash Flow Hedges of Interest Rate Risk. Our objectives in using interest rate derivatives are to add stability to

interest expense, to manage our exposure to interest rate movements and to better match funding costs to the interest

received on the fixed-rate receivables being securitized. To accomplish these objectives, we primarily use interest

rate swaps. Interest rate swaps designated as cash flow hedges involve the receipt of variable amounts from a

counterparty in exchange for our making fixed-rate payments over the life of the agreements without exchange of