CarMax 2011 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2011 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

51

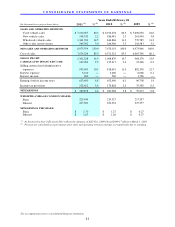

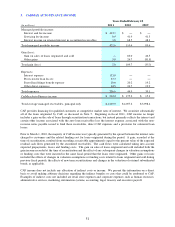

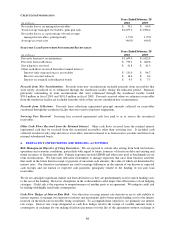

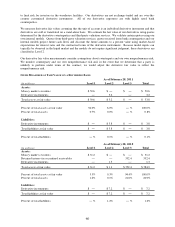

3. CARMAX AUTO FINANCE INCOME

(In millions)

Managed portfolio income:

Interest and fee income

$ 419.1 $ ― $ ―

Servicing fee income

0.9 41.9 41.3

Interest income on retained interest in securitized receivables

1.6 68.5 48.3

Total managed portfolio income

421.6 110.4 89.6

Gain (loss):

Gain on sales of loans originated and sold

― 83.0 46.5

Other gains

5.0 26.7 (81.8)

Total gain (loss)

5.0 109.7 (35.3)

Expenses:

Interest expense

133.8 ― ―

Provision for loan losses

27.7 ― ―

Payroll and fringe benefit expense

20.6 20.2 19.2

Other direct expenses

24.5 24.7 19.9

Total expenses

206.6 44.9 39.1

CarMax Auto Finance income

$ 220.0 $ 175.2 $ 15.3

Total average managed receivables, principal only

$ 4,229.9 $ 4,057.2 $ 3,998.4

Years Ended February 28

2011

2010

2009

CAF provides financing for qualified customers at competitive market rates of interest. We securitize substantially

all of the loans originated by CAF, as discussed in Note 5. Beginning in fiscal 2011, CAF income no longer

includes a gain on the sale of loans through securitization transactions, but instead primarily reflects the interest and

certain other income associated with the auto loan receivables less the interest expense associated with the non-

recourse notes payable issued to fund these receivables, direct CAF expenses and a provision for estimated loan

losses.

Prior to March 1, 2010, the majority of CAF income was typically generated by the spread between the interest rates

charged to customers and the related funding cost for loans originated during the period. A gain, recorded at the

time of securitization, resulted from recording a receivable approximately equal to the present value of the expected

residual cash flows generated by the securitized receivables. The cash flows were calculated taking into account

expected prepayments, losses and funding costs. The gain on sales of loans originated and sold included both the

gain income recorded at the time of securitization and the effect of any subsequent changes in valuation assumptions

or funding costs that were incurred in the same fiscal period that the loans were originated. Other gains or losses

included the effects of changes in valuation assumptions or funding costs related to loans originated and sold during

previous fiscal periods, the effects of new term securitizations and changes in the valuation of retained subordinated

bonds, as applicable.

CAF income does not include any allocation of indirect costs or income. We present this information on a direct

basis to avoid making arbitrary decisions regarding the indirect benefits or costs that could be attributed to CAF.

Examples of indirect costs not included are retail store expenses and corporate expenses such as human resources,

administrative services, marketing, information systems, accounting, legal, treasury and executive payroll.