CarMax 2011 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2011 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

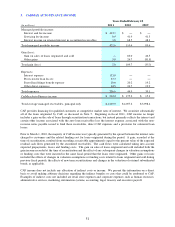

55

each future period by the number of periods until that future period, summing those products and dividing the sum

by the initial principal balance.

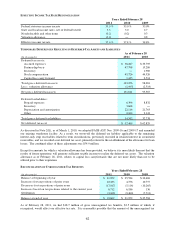

Interest-Only Strip Receivables. Interest-only strip receivables represented the present value of residual cash flows

we expected to receive over the life of the securitized receivables. The value of these receivables was determined by

estimating the future cash flows using our assumptions of key factors, such as finance charge income, loss rates,

prepayment rates, funding costs and discount rates appropriate for the type of asset and risk. The value of interest-

only strip receivables could have been affected by external factors, such as changes in the behavior patterns of

customers, changes in the strength of the economy and developments in the interest rate and credit markets;

therefore, actual performance could have differed from these assumptions. We evaluated the performance of the

receivables relative to these assumptions on a regular basis. Any financial impact resulting from a change in

performance was recognized in earnings in the period in which it occurred. Effective March 1, 2010, interest-only

strip receivables are no longer reported on the consolidated balance sheets.

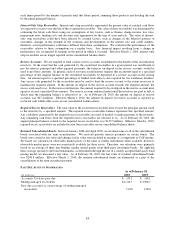

Reserve Accounts. We are required to fund various reserve accounts established for the benefit of the securitization

investors. In the event that the cash generated by the securitized receivables in a given period was insufficient to

pay the interest, principal and other required payments, the balances on deposit in the reserve accounts would be

used to pay those amounts. In general, each of our term securitizations requires that an amount equal to a specified

percentage of the original balance of the securitized receivables be deposited in a reserve account on the closing

date. An amount equal to a specified percentage of funded receivables is also required for our warehouse facilities.

Any excess cash generated by the receivables must be used to fund the reserve account to the extent necessary to

maintain the required amount. If the amount on deposit in the reserve account exceeds the required amount, the

excess is released to us. In the term securitizations, the amount required to be on deposit in the reserve account must

equal or exceed a specified floor amount. The reserve account remains funded until the investors are paid in full, at

which time the remaining balance is released to us. As of February 28, 2010, the amount on deposit in reserve

accounts was $47.4 million. Effective March 1, 2010, the amount on deposit in reserve accounts is reported as

restricted cash within other assets on our consolidated balance sheets.

Required Excess Receivables. The total value of the securitized receivables must exceed the principal amount owed

to the investors by a specified amount. The required excess receivables balance represents this specified amount.

Any cash flows generated by the required excess receivables are used, if needed, to make payments to the investors.

Any remaining cash flows from the required excess receivables are released to us. As of February 28, 2010, the

unpaid principal balance related to the required excess receivables was $129.5 million. Effective March 1, 2010,

required excess receivables are included in auto loan receivables on our consolidated balance sheets.

Retained Subordinated Bonds. Between January 2008 and April 2009, we retained some or all of the subordinated

bonds associated with our term securitizations. We received periodic interest payments on certain bonds. The

bonds were carried at fair value and changes in fair value were included in earnings as a component of CAF income.

We based our valuation on observable market prices of the same or similar instruments when available; however,

observable market prices were not consistently available for these assets. Therefore, our valuations were primarily

based on an average of three non-binding, market spread quotes from third-party investment banks. By applying

these average spreads to the bond benchmarks, as determined through the use of a widely accepted third-party bond

pricing model, we measured a fair value. As of February 28, 2010, the fair value of retained subordinated bonds

was $248.8 million. Effective March 1, 2010, the retained subordinated bonds are eliminated as a part of the

consolidation of the term securitization trusts.

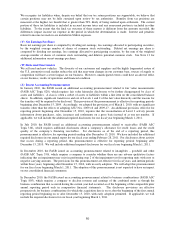

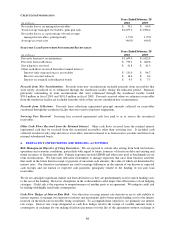

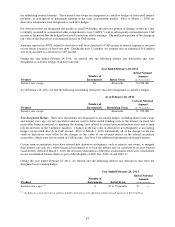

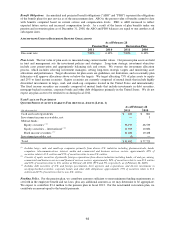

PAST DUE ACCOUNT INFORMATION

(In millions)

Accounts 31+ days past due 133.2$ 118.1$

Ending managed receivables 4,112.7$ 3,986.7$

Past due accounts as a percentage of ending managed

receivables

3.24% 2.96%

As of February 28

2010

2009