CarMax 2011 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2011 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

28

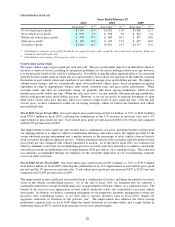

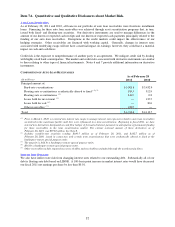

Impact of Inflation

Historically, inflation has not been a significant contributor to results. Profitability is primarily affected by our

ability to achieve targeted unit sales and gross profit dollars per vehicle rather than on average retail prices.

However, increases in average vehicle selling prices benefit the SG&A ratio and CAF income, to the extent the

average amount financed also increases.

During fiscal 2011 and 2010, we experienced a period of appreciation in used vehicle wholesale pricing. We

believe the appreciation resulted, in part, from a reduced supply of used vehicles in the market that was caused by

the dramatic decline in new car industry sales and the associated slow down in used vehicle trade-in activity in fiscal

2010 and fiscal 2009. The appreciation also reflected a rebound in pricing compared with the severe depreciation

experienced in fiscal 2009. The higher wholesale values increased both our vehicle acquisition costs and our

average selling prices for used and wholesale vehicles.

During fiscal 2009, the weakness in the economy and the stresses on consumer spending contributed to the industry-

wide slowdown in the sale of new and used vehicles and to the unprecedented decline in wholesale market prices for

most vehicle classes during the first three quarters of the year. A sharp increase in gasoline prices particularly

pressured wholesale valuations for SUVs and trucks. These lower wholesale values reduced our vehicle acquisition

costs and contributed to the decline in our used and wholesale vehicle average selling price.

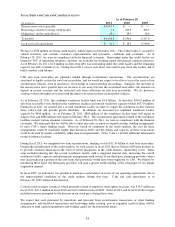

CarMax Auto Finance Income

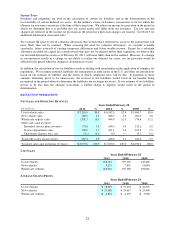

CAF provides financing for a portion of our used and new car retail sales. Because the purchase of a vehicle is

generally reliant on the consumer’s ability to obtain on-the-spot financing, it is important to our business that

financing be available to creditworthy customers. While financing can also be obtained from third-party sources, we

believe that total reliance on third parties can create unacceptable volatility and business risk. Furthermore, we

believe that our processes and systems, the transparency of our pricing and our vehicle quality provide a unique and

ideal environment in which to procure high quality auto loans, both for CAF and for the third-party financing

providers. Generally, CAF has provided us the opportunity to capture additional profits and cash flows from auto

loan receivables while managing our reliance on third-party financing sources. We also believe CAF enables us to

capture additional sales.

CAF provides financing for qualified customers at competitive market rates of interest. The majority of CAF

income has typically been generated by the spread between the interest rates charged to customers and the related

cost of funds. Substantially all of the loans originated by CAF are sold in securitization transactions.

As described in the Critical Accounting Policies section of this MD&A, as of March 1, 2010, we adopted ASU Nos.

2009-16 and 2009-17 on a prospective basis. Beginning in fiscal 2011, CAF income no longer includes a gain on

the sale of loans through securitization transactions, but instead primarily reflects the interest and fee income

associated with owning and servicing the auto loan receivables less the interest expense associated with the non-

recourse notes payable issued to fund these receivables, direct CAF expenses and a provision for estimated loan

losses.