Berkshire Hathaway 2009 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2009 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

|

|

Management’s Discussion (Continued)

Derivative contract liabilities (Continued)

availability of data on newer contracts, which is used for comparison. We entered into one credit default contract in 2009, while

several contracts expired or terminated. Accordingly, our remaining risk under credit default contracts has declined from year

end 2008.

We determine the estimated fair value of equity index put option contracts based on the widely used Black-Scholes option

valuation model. Inputs to the model include the current index value, strike price, discount rate, dividend rate and contract

expiration date. The weighted average discount and dividend rates used as of December 31, 2009 were 4.0% and 2.7%,

respectively, and were each approximately 4.0% as of December 31, 2008. The discount rates as of December 31, 2009 and

2008 were approximately 55 basis points and 125 basis points (on a weighted average basis), respectively, over benchmark

interest rates and represented an estimate of the spread between our borrowing rates and the benchmark rates for comparable

durations. The spread adjustments were based on spreads for our obligations and obligations for comparably rated issuers. We

believe the most significant economic risks relate to changes in the index value component and to a lesser degree to the foreign

currency component. For additional information, see our Market Risk Disclosures.

The Black-Scholes model also incorporates volatility estimates that measure potential price changes over time. The

weighted average volatility used as of December 31, 2009 was approximately 22%, which was relatively unchanged from year

end 2008. The weighted average volatilities are based on the volatility input for each equity index put option contract weighted

by the notional value of each equity index put option contract as compared to the aggregate notional value of all equity index

put option contracts. The volatility input for each equity index put option contract is based upon the implied volatility at the

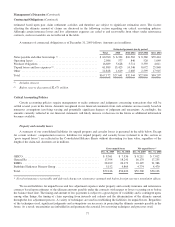

inception of each equity index put option contract. The impact on fair value as of December 31, 2009 ($7.3 billion) from

changes in volatility is summarized below. The values of contracts in an actual exchange are affected by market conditions and

perceptions of the buyers and sellers. Actual values in an exchange may differ significantly from the values produced by any

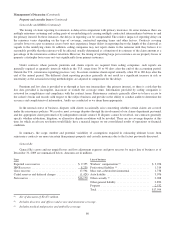

mathematical model. Dollars are in millions.

Hypothetical change in volatility (percentage points) Hypothetical fair value

Increase 2 percentage points .............................................................. $7,885

Increase 4 percentage points .............................................................. 8,459

Decrease 2 percentage points .............................................................. 6,734

Decrease 4 percentage points .............................................................. 6,163

Other Critical Accounting Policies

We record deferred charges with respect to liabilities assumed under retroactive reinsurance contracts. At the inception of

these contracts, the deferred charges represent the difference between the consideration received and the estimated ultimate

liability for unpaid losses. Deferred charges are amortized using the interest method over an estimate of the ultimate claim

payment period with the periodic amortization reflected in earnings as a component of losses and loss expenses. Deferred

charge balances are adjusted periodically to reflect new projections of the amount and timing of loss payments. Adjustments to

these assumptions are applied retrospectively from the inception of the contract. Unamortized deferred charges were $4.0 billion

at December 31, 2009. Significant changes in the estimated amount and payment timing of unpaid losses may have a significant

effect on unamortized deferred charges and the amount of periodic amortization.

Our Consolidated Balance Sheet as of December 31, 2009 includes goodwill of acquired businesses of approximately

$34.0 billion. We evaluate goodwill for impairment at least annually and conducted an annual review in the fourth quarter. Such

tests include determining the estimated fair value of our reporting units and performing goodwill impairment tests. There are

several methods of estimating a reporting unit’s fair value, including market quotations, underlying asset and liability fair value

determinations and other valuation techniques, such as discounted projected future net earnings or net cash flows and multiples

of earnings. We primarily use discounted projected future earnings or cash flow methods. The key assumptions and inputs used

in such methods may involve forecasting revenues and expenses, operating cash flows and capital expenditures as well as an

appropriate discount rate. A significant amount of judgment is required in estimating the fair value of the reporting unit and

performing goodwill impairment tests. Due to the inherent uncertainty in forecasting cash flows and earnings, actual future

results may vary significantly from the forecasts. If the carrying amount of a reporting unit, including goodwill, exceeds the

estimated fair value, then individual assets (including identifiable intangible assets) and liabilities of the reporting unit are

estimated at fair value. The excess of the estimated fair value of the reporting unit over the estimated fair value of net assets

would establish the implied value of goodwill. The excess of the recorded amount of goodwill over the implied value is then

charged to earnings as an impairment loss.

85