Berkshire Hathaway 2009 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2009 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

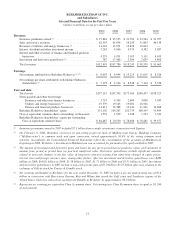

Notes to Consolidated Financial Statements (Continued)

(1) Significant accounting policies and practices (Continued)

(f) Derivatives

We carry derivative contracts at estimated fair value in the accompanying Consolidated Balance Sheets. Such

balances reflect reductions permitted under master netting agreements with counterparties. The changes in fair value

of derivative contracts that do not qualify as hedging instruments for financial reporting purposes are recorded in

earnings as derivative gains/losses.

Cash collateral received from or paid to counterparties to secure derivative contract assets or liabilities is included in

other liabilities or assets of finance and financial products businesses. Securities received from counterparties as

collateral are not recorded as assets and securities delivered to counterparties as collateral continue to be reflected as

assets in our Consolidated Balance Sheets.

(g) Fair value measurements

As defined under GAAP, fair value is the price that would be received to sell an asset or paid to transfer a liability

between market participants in the principal market or in the most advantageous market when no principal market

exists. Market participants are assumed to be independent, knowledgeable, able and willing to transact an exchange

and not under duress. Nonperformance or credit risk is considered in determining the fair value of liabilities.

Considerable judgment may be required in interpreting market data used to develop the estimates of fair value.

Accordingly, estimates of fair value presented herein are not necessarily indicative of the amounts that could be

realized in a current or future market exchange.

Effective April 1, 2009, the FASB amended ASC 820 Fair Value Measurements and Disclosures to clarify that

adjustments to transaction prices or quoted market prices may be required in illiquid or disorderly markets in order to

estimate fair value. This amendment prescribes no specific methodology for making adjustments to transaction prices

or quoted prices but rather confirms that different valuation techniques may be appropriate under the circumstances to

determine the value that would be received to sell an asset or paid to transfer a liability in an orderly transaction. In

August 2009, the FASB issued Accounting Standards Update 2009-05, “Measuring Liabilities at Fair Value” (“ASU

2009-05”). ASU 2009-05 provides guidance on valuing a liability when a quoted price in an active market is not

available and was effective October 1, 2009. The adoption of the amendment to ASC 820 and ASU 2009-05 did not

have a material impact on our Consolidated Financial Statements.

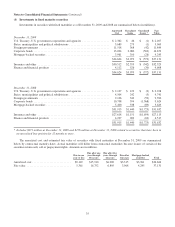

(h) Inventories

Inventories consist of manufactured goods and purchased goods acquired for resale. Manufactured inventory costs

include raw materials, direct and indirect labor and factory overhead. Inventories are stated at the lower of cost or

market. As of December 31, 2009, approximately 40% of the total inventory cost was determined using the

last-in-first-out (“LIFO”) method, 32% using the first-in-first-out (“FIFO”) method, with the remainder using the

specific identification method or average cost methods. With respect to inventories carried at LIFO cost, the aggregate

difference in value between LIFO cost and cost determined under FIFO methods was $661 million and $607 million

as of December 31, 2009 and 2008, respectively.

(i) Property, plant and equipment

Additions to property, plant and equipment are recorded at cost. The cost of major additions and betterments are

capitalized, while the cost of replacements, maintenance and repairs that do not improve or extend the useful lives of

the related assets are expensed as incurred. Interest over the construction period is capitalized as a component of cost

of constructed assets. In addition, the cost of constructed assets of certain of our regulated utility and energy

subsidiaries that are subject to ASC 980 Regulated Operations also includes an equity allowance for funds used during

construction. Also see Note 1(p).

Depreciation is provided principally on the straight-line method over estimated useful lives. Depreciation of assets of

certain regulated utility and energy subsidiaries is provided over recovery periods based on composite asset class lives

as agreed to by regulators.

30