Berkshire Hathaway 2009 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2009 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

|

|

Management’s Discussion (Continued)

Property and casualty losses (Continued)

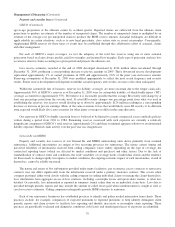

General Re (Continued)

occurrences. After deducting $148 million for the change in net reserve discounts during the year, workers’ compensation losses

from prior years reduced pre-tax earnings in 2009 by $95 million. To illustrate the sensitivity of changes in expected loss

emergence patterns and expected loss ratios for our significant excess-of-loss workers’ compensation reserve cells, an increase

of ten points in the tail of the expected emergence pattern and an increase of ten percent in the expected loss ratios would

produce a net increase in our nominal IBNR reserves of approximately $704 million and $408 million on a discounted basis as

of December 31, 2009. The increase in discounted reserves would produce a corresponding decrease in pre-tax earnings. We

believe it is reasonably possible for the tail of the expected loss emergence patterns and expected loss ratios to increase at these

rates.

Our other casualty and general liability reported losses (excluding mass tort losses) were favorable in 2009 relative to

expectations. Casualty losses tend to be long-tail and it should not be assumed that favorable loss experience in a given year

means that loss reserve amounts currently established will continue to develop favorably. For our significant other casualty and

general liability reserve cells (including medical malpractice, umbrella, auto and general liability), an increase of five points in

the tails of the expected emergence patterns and an increase of five percent in expected loss ratios (one percent for large

international proportional reserve cells) would produce a net increase in our nominal IBNR reserves and a corresponding

reduction in pre-tax earnings of approximately $922 million. We believe it is reasonably possible for the tail of the expected loss

emergence patterns and expected loss ratios to increase at these rates in any of the individual aforementioned reserve cells.

However, given the diversification in worldwide business, more likely outcomes are believed to be less than $922 million.

Our property losses were lower than expected in 2009 but the nature of property loss experience tends to be more volatile

because of the effect of catastrophes and large individual property losses. In response to favorable claim developments and

another year of information, estimated remaining World Trade Center losses were reduced by $17 million.

In certain reserve cells within excess directors and officers and errors and omissions (“D&O and E&O”) coverages, IBNR

reserves are based on estimated ultimate losses without consideration of expected emergence patterns. These cells often involve

a spike in loss activity arising from recent industry developments making it difficult to select an expected loss emergence

pattern. For our large D&O and E&O reserve cells an increase of ten points in the tail of the expected emergence pattern (for

those cells where emergence patterns are considered) and an increase of ten percent in the expected loss ratios would produce a

net increase in nominal IBNR reserves and a corresponding reduction in pre-tax earnings of approximately $220 million. We

believe it is reasonably possible for the tail of the expected loss emergence patterns and expected loss ratios to increase at these

rates.

Overall industry-wide loss experience data and informed judgment are used when internal loss data is of limited reliability,

such as in setting the estimates for mass tort, asbestos and hazardous waste (collectively, “mass tort”) claims. Unpaid mass tort

reserves at December 31, 2009 were approximately $1.7 billion gross and $1.3 billion net of reinsurance. Such reserves were

approximately $1.8 billion gross and $1.2 billion net of reinsurance as of December 31, 2008. Mass tort net claims paid were

about $87 million in 2009. In 2009, ultimate loss estimates for asbestos and environmental claims were increased by $83

million. In addition to the previously described methodologies, we consider “survival ratios” based on net claim payments in

recent years versus net unpaid losses as a rough guide to reserve adequacy. The survival ratio based on claims payments made

over the last three years was approximately 14.5 years as of December 31, 2009. The insurance industry’s comparable survival

ratio for asbestos and pollution reserves was approximately 8 years. Estimating mass tort losses is very difficult due to the

changing legal environment. Although such reserves are believed to be adequate, significant reserve increases may be required

in the future if new exposures or claimants are identified, new claims are reported or new theories of liability emerge.

82