BMW 2014 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2014 BMW annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

|

|

23 COMBINED MANAGEMENT REPORT

General economic environment in 2014

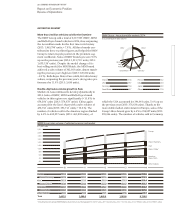

Overall, the global economy grew by 3.3 % in 2014, with

significant differences in growth rates recorded from

region to region. After a weak start, the USA performed

strongly over the year as a whole. The growth rate in

China remained at a relatively high level, despite a

moderate slowdown in economic momentum. As a result

of the value added tax hike, Japan recorded a steeper

drop in growth than had been expected. Even though

recession was overcome in Europe as a whole, the

re-

covery could hardly be described as dynamic, especially

in the major economies. The ongoing weak performance

of some major emerging markets, in particular Brazil

and Russia, also held down the global growth rate. Al-

though the Indian economy regained some momentum,

the growth rate was still lower than in recent years.

In line with its previous announcements, the US Reserve

Bank brought its bond-buying programme to an end

during the year under report, resulting – in spring 2014

– in considerable turmoil for the currencies of some of

the world’s emerging market countries. However, so far,

this first step to scale back its highly expansionary

monetary policy has not had a major adverse impact,

either in the USA or in other countries.

After a two-year lull, the eurozone returned to growth

in 2014, albeit at a modest rate of 0.8 %. The German

economy grew overall by 1.5 %. France was once again

only able to report a very low growth rate of 0.4 %. Italy’s

economy contracted for the third year in succession,

this time at a less pronounced rate than in previous years

(–

0.4 %). By contrast, most of the other southern

Euro-

pean economies recovered well and recorded positive

growth again after years of recession.

As the largest European economy outside the eurozone,

the United Kingdom saw a continuation of its run of

good quarterly figures and recorded a growth rate of

2.6 % for the year as a whole. Although bolstered by

monetary and fiscal policies implemented on a massive

scale, it appears that the UK economy has now found

a stronger footing to enable it to grow at a decent pace

over a sustained period of time.

The cyclical upturn in the USA gained further momen-

tum in 2014. Although the reported growth rate of 2.4 %

was similarly high compared to the previous year, it was

only the

impact of the severe winter that prevented an

even better

performance for the year as a whole. The

upturn was driven once again primarily by the private

sector, with the strongest stimulus coming from the

employment and property markets. At the same time,

the downward

pressure on public-sector budgets and

the gradual

scaling back of expansionary monetary

policies held

down growth in the US economy slightly.

The Japanese economy was influenced by a mixture of

positive and negative factors in 2014, including a

con-

tinuation of highly expansionary monetary policies on

the one hand, and a hike in the value added tax rate in

April on the other. The overall outcome was that growth

slipped to 0.3 % in Japan in 2014.

With a slightly reduced growth rate of 7.4 %, China re-

mained

by far the most dynamic of the world’s major

economies. By contrast, the performance of other major

emerging economies was generally disappointing. India,

for instance, managed a slightly improved growth rate

of 5.4 % in 2014, still trailing against growth rates

re-

ported

in previous years. Brazil and Russia grew by 0.2 %

and 0.6 % respectively, not far short of recession.

Currency markets

The US dollar averaged an exchange rate of 1.33 to the

euro in 2014, similar to the previous year’s level. How-

ever, the range of fluctuation was much greater, with

the US dollar initially losing value only then to surge

during the second half of the year to finish at US dollar

1.21 to the euro. The British pound also appreciated in

value, which is reflected in an annual average exchange

rate of 0.81 to the euro. These exchange rates were af-

fected by the expectation of reference interest rate in-

creases in these two currency blocks in 2015, a develop-

ment

exacerbated by the European Central Bank’s

decision to reduce interest rates again in 2014 and its

announcement to loosen its monetary policies further.

With its value coupled to that of the US dollar, the an-

nual average exchange rate of the Chinese renminbi

(8.19 to the euro) remained at a similar level to the pre-

vious year. With fluctuations in exchange rates following

the same pattern as the US dollar, the Chinese renminbi

also gained noticeably in value towards the end of the

year. In sharp contrast, the Japanese yen fell to an annual

average rate of 140 yen to the euro in the wake of

Japan’s

monetary policy. Despite showing some signs of stabilising

Report on Economic Position

General and Sector-specific Environment