BMW 2014 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2014 BMW annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

|

|

108

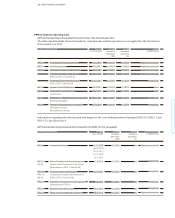

90 GROUP FINANCIAL STATEMENTS

90 Income Statements

90 Statement of

Comprehensive Income

92 Balance Sheets

94 Cash Flow Statements

96 Group Statement of Changes in

Equity

98 Notes

98 Accounting Principles and

Policies

116 Notes to the Income Statement

123 Notes to the Statement

of Comprehensive Income

124

Notes to the Balance Sheet

149 Other Disclosures

165 Segment Information

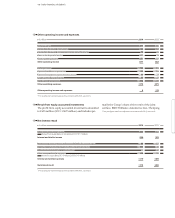

The calculation of deferred tax assets requires assump-

tions

to be made with regard to the level of future tax-

able

income and the timing of recovery of deferred tax

assets. These assumptions take account of forecast oper-

ating results and the impact on earnings of the reversal

of taxable temporary differences. Since future business

developments cannot be predicted with certainty and to

some extent cannot be influenced by the BMW Group,

the measurement of deferred tax assets is subject to un-

certainty. Further information is provided in note 17.

Current income taxes are computed throughout the

BMW Group in accordance with tax legislation appli-

cable

in each relevant country. In situations where a

permissible element of discretion has been applied in

determining the amount of a tax exposure to be recog-

nised in the financial statements, there is always a pos-

sibility that local tax authorities may reach a different

conclusion.

The calculation of pension provisions requires assump-

tions to be made with regard to discount factors, salary

trends, employee fluctuation and the life expectancy

of

employees. As in previous years, discount factors are

determined by reference to market yields at the end of

the reporting period on high quality corporate bonds.

The salary level trend refers to the expected rate of

salary

increase which is estimated annually depending

on inflation and the career development of employees

within the Group. Further information is provided in

note 36.

Estimations are required for the purposes of recognis-

ing and measuring provisions for warranty obligations

(statutory, contractual and voluntary). In addition to

statutorily prescribed manufacturer warranties, the

BMW Group also offers various categories of warranty

depending on the product and sales market concerned.

Warranty provisions are recognised when the risks

and

rewards of ownership of the goods are transferred

to the dealer or retail customer or when a new category

of warranty is introduced. In order to determine the

level of the provision, various factors are taken into

consideration, including estimations based on past ex-

perience with the nature and amount of claims. These

estimations also involve assessing the future level of

potential repair costs and price increases per product

and market. Provisions for warranties are adjusted

regularly to take account of new circumstances and the

impact of any changes recognised in the income

state-

ment. Further information is provided in note 37.

Similar estimates are also made in conjunction with the

measurement of expected reimbursement claims.

In the event of involvement in legal proceedings or

when claims are brought against a Group entity, provi-

sions for litigation and liability risks are recognised

when an outflow of resources is probable and a reliable

estimate can be made of the amount of the obligation.

Management is required to make assumptions with re-

spect to the probability of occurrence, the amount in-

volved and the duration of the legal dispute. For these

reasons, the recognition and measurement of provi-

sions for litigation and liability risks are subject to un-

certainty. Further information is provided in note 37.

In addition, judgement is required in particular when

assessing whether the risks and rewards incidental to

ownership of a leased asset have been transferred for

the purposes of determining the classification of leasing

arrangements.

Determining the scope of consolidated companies to

be

included in the Group Financial Statements may

involve the use of judgement. In particular when the

BMW Group holds 50 % or less of the voting rights, a

detailed assessment must be made as to whether sole

control, joint control or significant influence applies.

For instance, other contractual rights and / or other mat-

ters and circumstances could result in the conclusion

that the BMW entity concerned controls or jointly

con-

trols an entity in which it has a participation. In the

latter case, it must then be decided whether the joint

arrangement is a joint operation or a joint venture. In

making its judgement, the BMW Group must take all

contractual arrangements and other circumstances into

account, and not just the structure and legal form of

the entity. A new assessment is made in the event of

any indication of changes in the previous assessment of

(joint) control. Further information is provided in note 2.