Asus 2009 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2009 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

|

|

39

YU

CHI-LUNG

and administrative measures

LO JUI-LAN

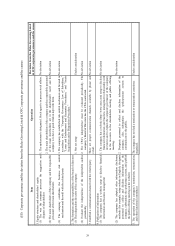

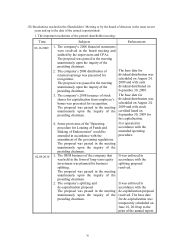

Note 1: If the company has retained the service of another CPA Firm or CPAs, the auditing period must

be detailed and with the reason for the change of CPA service detailed in the note. The

infomraiton of auditing fees, the auditing amount and non-auditing amount; also, the

non-auditing service must be disclose.

Note 2: The information of non-auditing service must be disclosed in details. If the “others” of the

non-auditing service amounts over 25% of the non-auditing amount, the content of service

must be detailed in the note.

(II) If the auditing fee paid in the year retaining service from another CPA Firm is less than the

auditing fee paid in the year before, the amount of auditing fee before and after the change of

CPA Firm and the reasons for the said change must be disclosed: None

(III) If the auditing fee paid in the year retaining service from another CPA Firm is over 15% less

than the auditing fee paid in the year before, the amount and ratio of auditing fee reduced and

the reasons for the said change must be disclosed: Not applicable since the company’ s auditing

fee paid in 2009 was not over 15% less than the auditing fee paid in 2008.

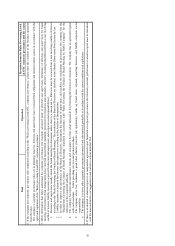

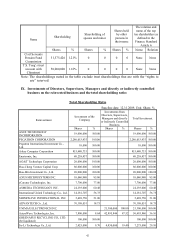

V. CPA’s information:

(I) Former CPAs

Date of change Aug 26, 2009

Reasons and explanation

of changes

In response to the company’ s integrated business management and

development

State whether the

appointment is

terminated or rejected by

the consignor or CPAs

Client

Status

CPA Consignor

Appointment terminated

automatically V

Appointment rejected

(discontinued)

The opinions other than

unqualified opinion

issued in the last two

years and the reasons for

the said opinions

None

Is there any difference in

opinion with the issuer

Yes

Accounting principle or practice

Disclosure of financial statements

Auditing scope or procedures

Others

No V

Explanation

Supplementary disclosure

(disclosures specified in Article 10.5.1.4 of the standards) None