Asus 2009 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2009 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

|

|

100

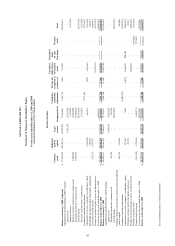

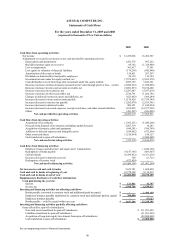

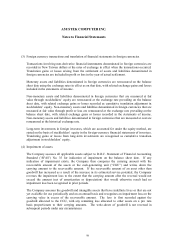

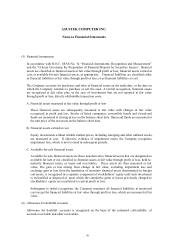

ASUSTEK COMPUTER INC.

Notes to Financial Statements

(7) Inventories

The costs of inventories include those necessary expenditures incurred in bringing each item of

inventory to its usable condition and location. Cost is calculated on a weighted-average basis.

Up to December 31, 2008, inventories were valued at the lower of cost or market value using the

gross method. The market values of raw materials and supplies were based on the replacement

cost, while those of work in process and finished goods were based on net realizable value.

Effective January 1, 2009, inventories are valued at the lower of cost or net realizable value. Net

realizable value by item is determined based on the estimated selling price in the ordinary course

of business, less estimated costs of completion and costs incurred in order to make the sale.

(8) Long-term equity investments

Long-term investments are accounted for under the equity method when the percentage of

ownership held by the Company and its subsidiaries exceeds 20% or if the Company and its

subsidiaries own less than 20% of the investee’ s common stock but have significant influence on

the investee’ s operations. If an investee company accounted for under the equity method issues

new shares and the Company does not purchase new shares proportionately, then the investment

percentage, and therefore the equity in net assets of the investee, will be changed. The effect of

such change is adjusted against the additional paid-in capital resulting from long-term equity

investments or retained earnings.

The difference between the cost of the investment and the amount of underlying equity in net

assets of an investee attributed to depreciable, depletable, or amortizable assets is amortized over

the estimated remaining economic years. The difference attributed to the carrying amount in

excess of or lower than the fair value of assets is written off entirely when the difference

disappears. The cost of investment in excess of the fair value of identifiable net assets is

recognized as goodwill and is no longer amortized. The difference attributed to the fair value of

identifiable net assets in excess of the cost of investment causes a proportional decrease in the

carrying amount of non-current assets. When the carrying amount of non-current assets is

decreased to zero, the remaining difference is recorded as extraordinary gain or loss.

The difference between the disposal price and carrying amount of long-term equity investment

under the equity method on the disposal date is recognized as gain or loss from disposal of long-

term equity investment. The associated additional paid-in capital resulting from long-term equity

investment is reclassified into current gain or loss in proportion to disposal of long-term equity

investment.