Aflac 2008 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2008 Aflac annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

72 Aflac Incorporated Annual Report for 2008

our investment in BES would not be settled at a price less than

the amortized cost of the investment and we have the intent

and ability to hold this investment until recovery of fair value,

which may be maturity, we do not consider this investment to

be other-than-temporarily impaired at December 31, 2008.

Another component of the unrealized losses in the banks and

financial institutions sector as of December 31, 2008, was an

unrealized loss totaling $153 million related to Aflac’s $558

million investment in UniCredit S.p.A.’s German subsidiary

Bayerische Hypo-und Vereinsbank AG (HVB). Aflac’s HVB

investments include both yen-and dollar-denominated Tier

I and Tier II hybrid instruments that are subordinated fixed

maturity securities. The yen-denominated portion of these

subordinated fixed maturity securities totaled $494 million (¥45

billion) with an unrealized loss of $119 million while the dollar-

denominated portion of these securities totaled $53 million

with an unrealized loss of $38 million at year end. The increase

in the unrealized loss on our investment in HVB totaled $124

million during 2008. UniCredit, the parent company of HVB

is a financial services holding company based in Italy where it

enjoys a strong franchise with a significant presence in Germany,

Austria, Poland and Central Eastern Europe. HVB is a key part

of UniCredit with well-positioned retail and corporate banking

franchises in the South and North of Germany. HVB also houses

the Markets and Investment Banking Division of UniCredit.

The portion of the unrealized losses on our investment in HVB

related to foreign currency translation was $24 million. We

believe that the fair value of our investment in HVB is negatively

impacted by the downturn in the economic environment in

the European economies, particularly Germany, HVB’s key

market. Also negatively impacting HVB’s fair value is its parent

company’s marginal capital levels in 2008. In contrast however,

HVB reported much stronger capital levels than its parent

company at the end of September 30, 2008. Additionally,

during 2008 HVB has improved the quality of its loan portfolio

by reducing its exposure to real estate. Although HVB incurred

fairly significant asset write-downs related to structured credit

losses in 2008, its strong capital levels allowed HVB to absorb

these losses without any rating downgrades. As of December

31, 2008, all of our investments in our HVB investments carried

ratings in the A categories by Moody’s, S&P and Fitch.

As a class of securities, hybrid securities, and particularly

perpetual securities, have also suffered price erosion in the

fourth quarter of 2008 due to the financial crisis and perceived

higher deferral and extension risk. We have considered risks

common to perpetual securities, including deferral, extension

and loss absorption, in light of HVB’s strong competitive

position within the UniCredit franchise, HVB’s well-positioned

retail and corporate banking franchises in the South and North

of Germany, and HVB’s high capital ratios.

Based on our credit analysis, we believe that HVB’s ability

to service its obligation to Aflac is currently not impaired.

Accordingly, we believe it is probable that we will collect

all amounts due according to the contractual terms of the

investment. Since it is expected that our investment would

not be settled at a price less than the amortized cost of

the investment and we have the intent and ability to hold

this investment until recovery of fair value, which may be

maturity, we do not consider this investment to be other-than-

temporarily impaired at December 31, 2008.

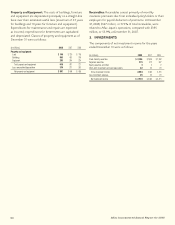

The following table shows the composition of our investments

in an unrealized loss position in the banks and financial

institutions sectors by fixed maturity securities and perpetual

securities. The table reflects those securities in that sector that

are in an unrealized loss position as a percentage of our total

investment portfolio in an unrealized loss position and their

respective unrealized losses as a percentage of total unrealized

losses as of December 31.

2008 2007

Percentage of Percentage of Percentage of Percentage of

Total Investments in Total Total Investments in Total

an Unrealized Loss Unrealized an Unrealized Loss Unrealized

Position Losses Position Losses

Fixed maturities 41% 40% 40% 41%

Perpetual securities:

Upper Tier II 9 8 6 3

Tier I 6 12 8 19

Total perpetual securities 15 20 14 22

Total 56% 60% 54% 63%

The valuation and pricing pressures from certain structured

investment securities throughout 2008, more notably the

banks and financial institutions sector’s exposure to the well

publicized structured investment vehicles (SIVs), coupled

with their exposure to the continued weakness in the housing

sector, in the UK, Europe and the United States, has led to

significant write-downs of asset values and capital pressure at

banks and financial institutions globally. National governments

in these regions have provided support in various forms,

ranging from guarantees on new and existing debt to

significant injections of capital. As the market continues to

deteriorate, more of these banks and financial institutions may

need various forms of government support before the current

economic downturn begins to ease. While it does not appear

to be a preferred solution, some troubled banks and financial

institutions may be nationalized. Very few nationalizations

have occurred to date, and in each instance, the governments

are standing behind the classes of investments that we own.

All of the investments in the government and guaranteed

sector in an unrealized loss position were investment grade

at December 31, 2008 and 2007. The unrealized losses on