Aflac 2008 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2008 Aflac annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

3

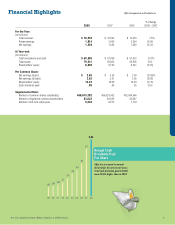

It’s no mystery how Aflac makes a difference.

program in 1994, we have bought more than

232 million shares. We also increased cash

dividends. Paid cash dividends in 2008 were

20.0% higher than in 2007. In October 2008,

the board of directors approved a 16.7%

increase in the cash dividend effective with

the first quarter of 2009, which will mark our

27th consecutive year of dividend increases.

While we still believe our capital position

to be strong, we will be closely monitoring

global financial markets and Aflac’s capital

position as 2009 progresses. As we have

previously announced, we do not anticipate

buying shares during the first half of the

year. Beyond the first six months, we will

evaluate that market and our capital position.

Obviously if conditions do not improve,

or if they deteriorate further, it is unlikely

we will buy shares back this year. Although

a significantly stronger yen to the dollar at

the end of the year and realized investment

losses in 2008 suppressed our risk-based

capital ratio, that important measure of

capital adequacy was still 476.5% at the end

of 2008. We believe our ratio compares

favorably to the industry.

Investing Prudently in a Volatile Market

I’m sure every individual and institutional

investor revisited their investment approach

in 2008 to make sure it was still appropriate.

We certainly did. However, we’re convinced

our global investment approach, which has

been consistently guided by Aflac’s board

of directors for many years, proved to

be prudent and effective in an extremely

distressed environment. Our investment

policy prohibits us from purchasing assets

that are deemed “speculative in nature.” As

such, we do not purchase junk bonds, nor do

we have any direct investment exposure to

the subprime mortgage market. At the end

of 2008, more than 98% of our holdings

were investment grade.

We purchase investments that best support

the liabilities of our insurance operations.

Our products in Japan, for instance,

produce long-duration, yen-denominated

policy liabilities. As such, we purchase

long-duration, yen-denominated assets to

support those liabilities. With the widening

of credit spreads in 2008, the long-duration

nature of our investments and the stronger

yen in relation to the dollar led to a large

unrealized loss in our portfolio. However,

because of our very strong cash flows, we

do not anticipate liquidating securities at a

loss to make claims payments. Instead, we

have both the intent and ability to hold our

investments until the market prices recover,

or when they mature.

Aflac Japan

We were pleased to see Aflac Japan’s new

annualized premium sales increase slightly

for the year, even though they fell below our

annual target for 2008. At the same time, we

remain encouraged about the opportunities

in the Japanese market, especially in light of

two new distribution opportunities that have

started gaining traction.

Daniel P. Amos

Chairman and CEO